16 Jan What’s the Difference Between Restricted and Unrestricted Grant Funds?

Short Answer

Restricted grant funds come with funder-imposed limitations specifying how the money must be used—typically for particular programs, specific expenses, designated time periods, or defined populations—and cannot be redirected to other purposes without funder permission, requiring careful tracking and separate accounting to demonstrate compliance. Unrestricted grant funds (also called general operating support) come with no usage limitations beyond supporting the organization’s overall charitable mission, giving nonprofits complete discretion to allocate funds where needed most—whether for programs, administration, staff salaries, infrastructure, reserves, or emerging priorities. Eligibility varies by grant, but the distinction fundamentally affects organizational flexibility, financial sustainability, administrative burden, and strategic capacity, with most Temecula and Inland Empire nonprofits finding that balanced portfolios combining both restricted program grants and unrestricted operating support provide optimal sustainability and adaptability.

What do restricted grant funds actually restrict and how does this affect operations?

Restricted grant funds typically specify one or more types of limitations that govern how recipients can use the money. Program restrictions limit funds to supporting specific activities—a grant for youth mentoring programs cannot be redirected to senior services even if both serve the organization’s mission. Expense category restrictions designate funds for particular costs like equipment purchases, staff salaries, facility improvements, or program supplies rather than allowing allocation across various expense types. Time restrictions require that funds be spent within defined periods—a one-year grant cannot extend spending into year two without funder approval. Population restrictions target funds toward serving specific communities like veterans, homeless families, or students in particular school districts.

These restrictions create operational complexity because Temecula nonprofits must track restricted funds separately from other revenue through fund accounting practices that demonstrate compliance with funder requirements. When a nonprofit receives three different restricted grants each supporting different programs with different allowable expenses and different time periods, financial management becomes significantly more complicated than if all revenue were unrestricted. Organizations need accounting systems that allocate expenses correctly to restricted fund sources, track spending against grant budgets, prevent inadvertent use of restricted funds for non-permitted purposes, and generate reports showing funder-specific financial activity.

The administrative burden of managing restricted funds increases with the number of different restricted grants an organization holds simultaneously. Each restricted grant requires separate budget tracking, periodic financial reports to the funder showing how their specific money was spent, documentation proving expenses charged to the grant align with approved budgets and allowable costs, and careful attention to spending deadlines ensuring funds are fully utilized before grant periods expire. Organizations heavily dependent on restricted program grants often employ significant staff time on grant compliance and reporting rather than direct program delivery.

Restricted funds limit strategic flexibility because they cannot be redirected when organizational priorities shift or unexpected needs emerge. If a nonprofit experiences facility emergency repairs requiring immediate funding, restricted program grants cannot be used for this purpose even if the organization desperately needs the money. If one program is oversubscribed while another struggles with low participation, restricted funding cannot shift between programs to align with actual community demand. Restrictions mean saying “we have money, but we cannot use it for this purpose” even when the purpose clearly serves the mission.

What makes unrestricted grants valuable despite being harder to obtain?

Unrestricted grants provide maximum organizational flexibility because funders impose no limitations on how recipients allocate the money beyond supporting the charitable mission generally. Organizations can use unrestricted funds for any legitimate purpose—direct program expenses, staff salaries regardless of which programs they support, administrative costs like accounting and legal services, facility rent and utilities, technology and equipment, professional development, financial reserves, or strategic initiatives not yet funded by specific program grants. This flexibility allows nonprofits to function as integrated organizations rather than collections of separately funded programs.

General operating support fills critical funding gaps that restricted program grants inherently create. While restricted grants might fund program staff salaries and direct participant costs, they rarely cover the executive director’s time spent on fundraising and organizational management, the bookkeeper processing grant reimbursements and financial reports, the rent and utilities for space where programs operate, or the technology infrastructure enabling program delivery. Unrestricted funds cover these essential but often “unexciting” costs that make programmatic work possible but struggle to attract dedicated restricted funding.

Unrestricted grants enable organizational innovation and adaptation by supporting work that hasn’t been pre-approved in specific grant applications. If community needs shift and a new program approach emerges as critical, unrestricted funds allow piloting the innovation before securing dedicated restricted funding. If evaluation data suggests program adjustments would improve outcomes, unrestricted funds enable adaptation without lengthy funder approval processes. Unrestricted support says “we trust your judgment about how to advance your mission” rather than “we’ll support specific pre-approved activities only.”

Financial sustainability and organizational health depend heavily on adequate unrestricted revenue. Organizations operating entirely on restricted program grants face chronic financial stress because they cannot cover indirect costs, build reserves, invest in infrastructure improvements, or weather temporary revenue shortfalls. Unrestricted funds provide the working capital and financial cushion that allow nonprofits to manage cash flow fluctuations, bridge gaps between restricted grant payments, and maintain operations during funding transitions. Most financially healthy Temecula nonprofits maintain unrestricted revenue representing 30-50% of total budgets alongside restricted program grants.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

The Nonprofit Launch Office operates within a strategic framework designed to help California nonprofits move from formation to fundability:

Launch includes understanding restricted versus unrestricted funding distinctions from the beginning so new organizations can develop balanced fundraising strategies. Launch-phase Temecula nonprofits often focus heavily on restricted program grants because they seem more accessible—funders feel comfortable supporting specific programs they can track and measure. However, Launch planning should include unrestricted revenue development through individual donor cultivation, board giving, earned income strategies, or capacity-building grants that provide general operating support. Early habits around funding mix significantly affect long-term financial sustainability.

Fix addresses situations where nonprofits became over-dependent on restricted program grants and now face financial stress from inability to cover administrative costs, invest in organizational infrastructure, or adapt to changing circumstances. Fix work involves diversifying revenue sources to include more unrestricted funding, developing compelling cases for general operating support that resonate with funders skeptical of “overhead,” implementing fund accounting systems that properly track restricted and unrestricted funds, and sometimes renegotiating restrictions with existing funders when original limitations prove operationally problematic.

Fund represents the operational state where organizations maintain healthy balances between restricted program grants funding specific work and unrestricted revenue providing flexibility, covering indirect costs, and enabling strategic adaptation. Fund-phase organizations understand how to articulate the value of general operating support to funders, maintain accounting systems that manage multiple restricted grants efficiently, and budget realistically about what restricted program grants can and cannot support. They pursue restricted grants strategically while continuously building unrestricted revenue streams.

Federal Recognition through IRS 501(c)(3) determination allows nonprofits to receive both restricted and unrestricted grants, but doesn’t eliminate the strategic challenge of building balanced funding portfolios. Federal tax exemption makes contributions tax-deductible regardless of whether they’re restricted or unrestricted, but funders make independent decisions about what types of support to provide based on their own philanthropic philosophies and risk tolerance.

CA Compliance Triangle (Secretary of State, Franchise Tax Board, Attorney General Registry) must be maintained with current standing regardless of whether an organization’s revenue is predominantly restricted or unrestricted. Compliance costs—filing fees, staff time for reporting, professional services—typically come from unrestricted funds since most restricted program grants won’t pay for compliance activities. This reality illustrates why unrestricted revenue is essential—compliance obligations exist regardless of funding mix, and someone must pay for them.

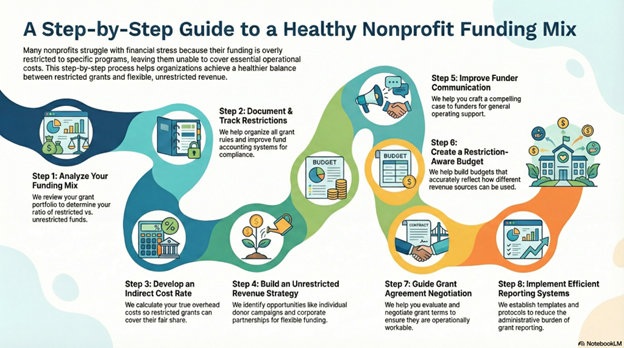

Step-by-step: How NPLO helps organizations understand and manage funding restrictions

Step 1: Current Funding Mix Analysis We review your existing grant portfolio to determine what percentage of revenue is restricted versus unrestricted, identify what restrictions currently apply to various funding sources, assess whether current restrictions create operational challenges or limit flexibility, and evaluate whether your funding balance supports financial sustainability. Many Temecula organizations discover they’re far more dependent on restricted program grants than optimal, with unrestricted revenue representing only 10-20% of budgets rather than healthier 30-50% targets.

Step 2: Restriction Documentation and Tracking We help organize clear documentation of every restriction on current grants—what each funder’s money can and cannot be used for, what time periods apply, what reporting requirements exist, and when restrictions expire. This comprehensive tracking prevents inadvertent misuse of restricted funds and ensures compliance with all funder requirements. We also help implement or improve fund accounting systems that maintain separate tracking for each restricted fund source.

Step 3: Indirect Cost Rate Development We help calculate legitimate indirect cost rates showing what percentage of program expenses represents shared organizational costs like facilities, administration, and overhead. Many restricted program grants allow charging indirect costs at negotiated or federally approved rates, but nonprofits must calculate and justify these rates. Proper indirect cost recovery helps restricted program grants cover their fair share of organizational overhead rather than leaving all administrative costs to unrestricted funds.

Step 4: Unrestricted Revenue Strategy Development We help identify and prioritize opportunities for building unrestricted revenue—individual donor campaigns emphasizing general operating support, corporate partnerships providing flexible funding, board giving focused on unrestricted contributions, earned income from fee-for-service programs, endowment or reserve fund development, and capacity-building grants specifically for organizational infrastructure. The strategy creates intentional plans for reducing over-dependence on restricted program grants.

Step 5: Funder Communication About Flexibility We help craft compelling cases for unrestricted support when approaching funders, explaining why general operating grants provide greater impact than restricted program support, articulating how administrative capacity enables program quality, and demonstrating organizational health and financial responsibility that justify funder confidence in unrestricted giving. Many funders will provide unrestricted support when asked thoughtfully, but nonprofits must make the case.

Step 6: Budget Development Reflecting Restrictions We help create organizational budgets that accurately reflect restricted and unrestricted revenue sources, show how restricted grants support specific programs, demonstrate how unrestricted funds cover shared organizational costs, identify funding gaps where additional unrestricted revenue is needed, and present realistic rather than optimistic financial pictures. Honest budgeting prevents the scenario where organizations commit to expenses they cannot cover once restrictions are properly accounted for.

Step 7: Grant Agreement Negotiation Guidance When restricted grant opportunities emerge, we help evaluate whether proposed restrictions are operationally workable, identify potentially problematic limitation language that should be negotiated, suggest alternative restriction frameworks that achieve funder accountability goals while providing recipient flexibility, and advise when restrictions are so onerous that declining the grant serves the organization better than accepting overly burdensome limitations.

Step 8: Reporting Systems Implementation We help establish efficient reporting systems that track restricted grant compliance and satisfy funder requirements without consuming excessive staff time—templates for common report types, documentation protocols for restricted expenses, financial tracking mechanisms linking expenses to specific grants, and calendars ensuring timely submission of required reports. Efficient systems reduce the administrative burden that makes restricted grants costly to manage.

Checklist: What you should understand before accepting restricted grants

Before accepting restricted grant funding, Temecula nonprofits should evaluate these considerations:

- Precise restriction language understanding exactly what the funder’s money can and cannot pay for based on grant agreement terms

- Allowable expense categories clarifying whether funds can cover salaries, benefits, equipment, supplies, subcontractors, travel, or other specific costs

- Indirect cost provisions determining whether the grant allows charging indirect/overhead costs and at what rate or amount

- Time period limitations knowing when spending must occur and whether unspent funds must be returned or can be extended with approval

- Geographic or population restrictions understanding if funds must serve specific communities, regions, or demographic groups

- Reporting requirements knowing what financial and programmatic reports funders expect, how often, and in what format

- Documentation standards understanding what records must be maintained proving restricted funds were used appropriately

- Amendment processes knowing how to request permission if circumstances change and you need to modify how funds are used

- Matching or cost-share requirements determining if you must provide specific amounts of other funding to access the restricted grant

- Budget line-item restrictions understanding if you must spend exact amounts on specific budget categories or have flexibility within the total

- Equipment and property provisions knowing if assets purchased with restricted funds become your property or have funder ownership interests

- End-of-grant requirements understanding what happens to unused funds, whether spending can extend past the grant period, or if unexpended amounts must be returned

- Modification and transfer limitations knowing if funds can be reallocated between budget categories with or without funder approval

- Audit and monitoring rights understanding if funders can conduct site visits, financial audits, or program monitoring to verify compliance

- True cost of compliance calculating staff time and systems needed to track, report, and comply with restrictions to determine if the grant amount justifies the administrative burden

Quick Answers (PPA)

Can we move money from a restricted grant to unrestricted use if we have urgent needs the restricted grant won’t cover? No, not without explicit funder permission, which is rarely granted. Restricted grant funds must be used according to the specific limitations the funder imposed, and redirecting restricted money to other purposes violates grant agreements and potentially violates charitable solicitation laws if restrictions were communicated to donors. If you have urgent unrestricted needs and only restricted funds available, you must either seek funder approval to modify restrictions (usually difficult), find other unrestricted revenue sources, or explain to stakeholders why the restricted funds cannot address the need despite being available. This frustrating scenario illustrates exactly why building unrestricted revenue is critical—it provides the flexibility to respond to unexpected needs that restricted grants cannot address.

Why don’t all funders just give unrestricted grants if they’re so much more valuable to nonprofits? Funders restrict grants for several reasons: accountability concerns (they want to ensure money supports specific work they care about), outcome measurement (easier to evaluate impact when funding specific programs versus general operations), donor expectations (individual donors or board members who provided the money expect it to fund particular work), strategic focus (foundation missions target specific issue areas or populations, not broad organizational support), and risk management (restricted grants feel safer to funders uncertain about an organization’s overall management). Additionally, many funders believe restricted program support is more valuable because they fundamentally misunderstand the importance of organizational infrastructure, adequate staffing, and administrative capacity. Shifting funder behavior toward more unrestricted giving requires persistent sector-wide advocacy about the true costs of program delivery and the value of organizational health.

What’s a reasonable split between restricted and unrestricted revenue for a healthy nonprofit? While ideal ratios vary by organizational size, complexity, and program models, most financial sustainability experts suggest that 30-50% unrestricted revenue provides healthy balance for mid-sized nonprofits. Organizations with 20% or less unrestricted funding often struggle chronically with covering administrative costs, building reserves, and adapting to changing circumstances. Organizations with 60%+ unrestricted revenue enjoy significant flexibility but may struggle to attract the restricted program grants that demonstrate programmatic focus and impact to funders. Very small grassroots organizations might operate successfully with higher percentages of unrestricted revenue from individual donors, while large organizations managing complex multi-year government contracts might maintain lower unrestricted percentages if indirect cost recovery is strong. The key is having sufficient unrestricted funds to cover shared organizational costs, maintain working capital, and provide strategic flexibility.

Can we count the same expense toward multiple restricted grants if it benefits multiple programs? Generally no—this is considered “double-dipping” or improper cost allocation and violates grant compliance requirements. If an expense legitimately benefits multiple programs supported by different restricted grants, you must allocate the cost proportionally across those grants based on reasonable allocation methodologies (percentage of time, percentage of program participants served, square footage used, etc.). For example, if your executive director spends 25% of time on Program A (Grant 1) and 25% on Program B (Grant 2), you can charge 25% of their salary to each restricted grant, but you cannot charge 100% to both grants. Proper cost allocation requires time tracking, space usage documentation, or other allocation basis evidence. This is one reason why fund accounting systems and good financial management are essential when managing multiple restricted grants.

What happens if we don’t spend all the restricted grant money by the deadline—do we have to give it back? This depends entirely on the specific grant agreement language. Some funders require that unspent funds be returned at the end of the grant period, treating the grant as “use it or lose it.” Other funders allow requesting no-cost extensions that provide additional time to spend funds without additional money. Some agreements include provisions allowing unspent funds to roll into subsequent grant periods if the funder makes multi-year commitments. Review your grant agreement carefully to understand what provisions apply. If the deadline is approaching and spending won’t be complete, contact the funder immediately rather than waiting—proactive communication about legitimate reasons for underspending and requesting modifications shows professionalism and often results in workable solutions, while silent non-compliance or last-minute requests create funder distrust.

What to do next (DIY vs Done-With-You)

DIY approach: Conduct funding mix analysis by reviewing your current revenue sources and categorizing each as restricted or unrestricted based on grant agreements, donation letters, or funder communications. Calculate what percentage of total revenue is unrestricted—if it’s below 30%, you’re likely experiencing financial stress from inability to cover administrative costs or respond to unexpected needs. Review your accounting practices to ensure restricted and unrestricted funds are tracked separately through fund accounting rather than lumped together in single accounts. Examine each restricted grant agreement to document specific limitations—what the money can/cannot be used for, time periods, reporting requirements, and compliance obligations. Assess whether current restrictions create operational problems—are you unable to cover legitimate organizational costs because everything is restricted? Develop a strategic plan for increasing unrestricted revenue over the next 2-3 years through individual donor cultivation, general operating support grant applications, earned income, or other flexible funding sources. When considering new grant opportunities, evaluate the total cost of compliance including staff time for tracking and reporting against the grant amount to determine if restricted grants justify the administrative burden.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive funding restriction strategy for Temecula and Inland Empire nonprofits struggling with imbalanced funding portfolios or poor understanding of how restrictions affect operations. We analyze your current funding mix identifying the percentage restricted versus unrestricted and whether the balance supports sustainability, document all current restrictions and assess whether they create operational challenges, implement or improve fund accounting systems that properly track restricted and unrestricted funds separately, calculate legitimate indirect cost rates enabling better cost recovery from restricted program grants, develop strategic plans for building unrestricted revenue through diversified sources, create compelling cases for general operating support that persuade funders to provide flexible funding, provide grant agreement review and negotiation guidance when restricted funding opportunities emerge, and implement efficient reporting systems that satisfy funder compliance requirements without consuming excessive administrative resources. This comprehensive approach helps organizations understand the true impact of funding restrictions and develop sustainable funding portfolios balancing the accountability restricted grants provide with the flexibility unrestricted revenue enables.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Sources

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.