15 Feb What’s the Difference Between Form 990, 990-EZ, and 990-N (High Level)?

Short Answer

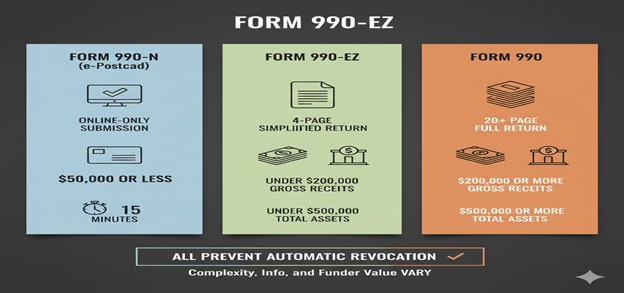

Form 990-N (e-Postcard) is a simple online-only submission for organizations with gross receipts normally $50,000 or less requiring only basic identifying information and taking 15 minutes to complete, Form 990-EZ is a 4-page simplified return for organizations with gross receipts under $200,000 AND total assets under $500,000 providing moderate financial detail with fewer schedules, and Form 990 is the comprehensive full return required for organizations with gross receipts of $200,000 or more OR total assets of $500,000 or more spanning 20+ pages with extensive financial reporting and multiple required schedules. All three satisfy annual filing requirements and prevent automatic revocation, but they differ dramatically in complexity, information disclosed, and value to funders evaluating organizational capacity—sophisticated funders prefer fuller returns showing financial health and governance practices that the e-Postcard doesn’t provide.

How do filing thresholds determine which form to use?

Gross receipts thresholds create the primary filing distinctions. Organizations with gross receipts normally $50,000 or less qualify for Form 990-N. Organizations with receipts under $200,000 AND assets under $500,000 qualify for Form 990-EZ. Organizations exceeding either the $200,000 receipts OR $500,000 assets threshold must file full Form 990. “Normally” is calculated using a three-year rolling average smoothing year-to-year fluctuations.

Both revenue and assets matter for 990-EZ eligibility. Meeting the receipts threshold alone isn’t sufficient—organizations must satisfy both tests. A small organization with $150,000 annual revenue but $600,000 in assets (perhaps owning property or having an endowment) must file Form 990, not 990-EZ. The dual thresholds recognize that organizational size isn’t purely revenue-based.

Organizations can voluntarily file more comprehensive forms. Riverside nonprofits qualifying for 990-N can choose to file 990-EZ or full Form 990 instead. Organizations qualifying for 990-EZ can choose full Form 990. Filing more comprehensive returns provides transparency and information valuable to funders. However, organizations cannot file simpler forms when thresholds require more comprehensive versions—filing 990-EZ when Form 990 is required violates filing obligations.

Threshold determination requires accurate calculations. Organizations miscalculating receipts or undervaluing assets and filing wrong forms face potential penalties and IRS inquiries. Conservative threshold application is advisable when close to boundaries—if genuinely uncertain whether you exceed thresholds, file the more comprehensive form rather than risking incorrect filing.

What information does each form require and disclose?

Form 990-N (e-Postcard) requires minimal information submitted through online system. Organizations provide tax year, legal name, any DBA names, mailing address, website if one exists, confirmation that gross receipts normally don’t exceed $50,000, name and address of principal officer, and EIN. No financial details, no program descriptions, no governance information beyond principal officer identification. The entire submission takes approximately 15 minutes.

Form 990-EZ provides moderate financial and program information. The 4-page return includes revenue summary by categories (contributions, program service revenue, other income), expense summary showing program services, management/general, and fundraising expenses, balance sheet showing assets and liabilities, and program service accomplishments describing major programs. Part V asks basic governance questions about conflict of interest policies, board meetings, and document retention. Required schedules add pages based on specific activities.

Form 990 requires comprehensive disclosure across 20+ pages. Beyond financial statements and program descriptions, the full return discloses detailed compensation information for officers, directors, key employees, and highly compensated staff, related party transactions and relationships, fundraising activities and professional fundraiser contracts, grant-making activities if applicable, foreign activities and operations, governance policies and practices in extensive detail, and compliance with specific requirements like hospital community benefit or school non-discrimination policies. Multiple schedules address specialized activities.

Public disclosure implications differ significantly. Form 990-N isn’t publicly available—only summary information confirming filing exists. Forms 990-EZ and 990 are public documents posted on GuideStar, Charity Navigator, and organizational websites. Full Form 990 discloses substantially more information about compensation, governance, and operations than 990-EZ, affecting public perception and funder evaluation.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

Launch includes understanding which form you’ll likely file as the organization grows. Riverside nonprofits starting small with 990-N eligibility should anticipate transitioning to 990-EZ and eventually full Form 990 as revenue and assets grow, planning recordkeeping systems supporting more comprehensive reporting.

Fix addresses situations where organizations filed wrong forms requiring amendment, underreported revenue or assets causing threshold miscalculations, or failed to transition to more comprehensive forms as they grew exceeding thresholds for simpler versions.

Fund success correlates with form comprehensiveness because funders gain more insight from fuller returns. Organizations voluntarily filing 990-EZ when they qualify for 990-N, or voluntarily filing Form 990 when they qualify for 990-EZ, often improve grant competitiveness by demonstrating transparency and providing information funders want.

Federal Recognition requires meeting annual filing obligations with appropriate form versions. Filing any of the three forms satisfies legal requirements preventing automatic revocation, but filing inappropriate versions (too simple when thresholds require comprehensive) may trigger IRS questions.

CA Compliance Triangle filing obligations exist independently of Form 990 version. Organizations filing 990-N, 990-EZ, or Form 990 federally still must file California Form 199 with Franchise Tax Board and RRF-1 with Attorney General Registry—federal form selection doesn’t affect California requirements.

Step-by-step: How NPLO helps organizations select and complete appropriate forms

Step 1: Threshold Calculation We accurately calculate 3-year average gross receipts and assess total assets determining which form is required.

Step 2: Strategic Form Selection For organizations qualifying for simpler forms, we discuss whether voluntary filing of fuller returns benefits grant competitiveness.

Step 3: Information Gathering We collect financial records, program documentation, and governance information appropriate to the form being filed.

Step 4: Accurate Completion We prepare complete returns answering all questions accurately with all required schedules.

Step 5: Governance Optimization For 990-EZ and Form 990 filers, we ensure governance question responses reflect strong practices.

Step 6: Funder Review Preparation We review returns from funder perspective identifying potential concerns before filing.

Step 7: Timely Filing We file electronically by deadlines preventing late penalties or countdown toward revocation.

Step 8: Transition Planning We help organizations anticipate when growth will require transitioning to more comprehensive forms.

Checklist: Comparing Form 990-N, 990-EZ, and Form 990

Form 990-N (e-Postcard):

- Who: Receipts normally ≤ $50K

- Length: Online submission, ~15 minutes

- Financial detail: None

- Program descriptions: None

- Governance questions: None

- Compensation disclosure: Principal officer only

- Public availability: Not posted publicly

- Funder value: Minimal information

Form 990-EZ:

- Who: Receipts < $200K AND assets < $500K

- Length: 4 pages + required schedules

- Financial detail: Revenue/expense summary, balance sheet

- Program descriptions: Program service accomplishments

- Governance questions: Basic (conflict policy, board meetings, retention)

- Compensation disclosure: Officers and directors

- Public availability: Posted on GuideStar, etc.

- Funder value: Moderate transparency

Form 990:

- Who: Receipts ≥ $200K OR assets ≥ $500K

- Length: 20+ pages + multiple schedules

- Financial detail: Comprehensive financial statements

- Program descriptions: Detailed program accomplishments

- Governance questions: Extensive governance section

- Compensation disclosure: Officers, directors, key employees, highly compensated

- Public availability: Widely posted and reviewed

- Funder value: Comprehensive transparency

Quick Answers (PPA)

We qualify for Form 990-N but funders keep asking for financial information—should we file 990-EZ instead? If you’re serious about pursuing grants, strongly consider voluntarily filing Form 990-EZ even though 990-N would satisfy legal requirements. The e-Postcard provides virtually no information funders need to evaluate financial health, program effectiveness, or governance quality. Filing 990-EZ demonstrates transparency and provides the financial and program information funders expect. The additional preparation time investment typically strengthens grant applications significantly enough to justify the effort. Many small organizations have adopted policies of filing 990-EZ regardless of 990-N eligibility specifically to support funding development.

What happens when we grow and exceed thresholds—do we automatically know, or does IRS notify us? You’re responsible for monitoring your own thresholds and transitioning to appropriate forms without IRS notification. Calculate your 3-year average gross receipts annually and assess total assets at year-end. When you exceed thresholds requiring a more comprehensive form, file that form starting with that tax year. IRS doesn’t send notices saying “you now need to file Form 990 instead of 990-EZ.” Organizations filing forms that are too simple when they’ve exceeded thresholds may face IRS inquiries requiring corrected returns and potential penalties.

If we filed Form 990-N last year but exceeded $50K this year, can we still file 990-N using the 3-year average? The 3-year rolling average smooths fluctuations allowing you to stay with 990-N longer than if each year stood alone. However, once your 3-year average exceeds $50,000, you must transition to 990-EZ or Form 990 (depending on whether you also exceed the $200K/$500K thresholds). Calculate precisely: (Year 1 + Year 2 + Year 3) ÷ 3. If the result exceeds $50,000, you no longer qualify for 990-N regardless of any single year being under $50,000. New organizations use different calculations: year one uses actual receipts, year two averages years one and two.

Do funders view Form 990-N filers as less credible or capable than organizations filing fuller returns? Sophisticated funders understand that 990-N is appropriate for very small organizations and don’t automatically penalize organizations for filing it when they qualify. However, funders need financial and program information to evaluate applications. Organizations filing 990-N must be prepared to provide financial statements, program descriptions, and governance documentation through other means when funders request it. Organizations repeatedly unable to provide information funders need may appear less organized or transparent than organizations whose Form 990-EZ or 990 already contains that information. Size-appropriate transparency is key.

Can we file amended returns changing from one form version to another if we realize we calculated thresholds wrong? If you filed 990-N but should have filed 990-EZ or Form 990 due to threshold miscalculations, you should file the correct comprehensive form as an amendment. However, if you filed Form 990 when you qualified for 990-EZ, or 990-EZ when you qualified for 990-N, the more comprehensive filing satisfied requirements—no amendment needed since you provided more information than required. Amendments are necessary when you filed too simple a form, not when you voluntarily filed a more comprehensive version.

What to do next (DIY vs Done-With-You)

DIY approach: Calculate your 3-year average gross receipts: add receipts from current year plus prior two years, divide by three. If you’re a new organization, year one uses actual receipts, year two averages years one and two. Assess total assets at fair market value from your year-end balance sheet including cash, investments, receivables, equipment, property. Determine which form you must file: 990-N if receipts normally ≤ $50K; 990-EZ if receipts < $200K AND assets < $500K; Form 990 if you exceed either threshold. Consider whether voluntary filing of fuller returns would strengthen grant competitiveness even if you qualify for simpler versions. Download appropriate form and instructions from IRS website. For 990-N, use IRS online e-Postcard system entering basic identifying information—takes about 15 minutes. For 990-EZ or Form 990, gather comprehensive financial records, program documentation, and governance information. Complete returns accurately answering all questions and completing required schedules. Have board treasurer or finance committee review draft before filing. File electronically by deadline (15th day of 5th month after fiscal year end) or file Form 8868 for automatic 6-month extension. Save filed return for records and prepare copies for funder requests.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive Form 990 preparation for Riverside and Inland Empire nonprofits filing any version. We accurately calculate 3-year average receipts and assess total assets determining which form is required, discuss strategic form selection including whether voluntary filing of fuller returns benefits grant development, collect all required financial records, program documentation, and governance information appropriate to the form being filed, prepare complete accurate returns answering all questions with all required schedules, optimize governance question responses demonstrating strong organizational practices, review returns from funder perspective identifying potential concerns before filing, file electronically by deadlines preventing late penalties, help organizations anticipate when growth will require transitioning to more comprehensive forms, and provide funder-ready copies for grant applications. This ensures you file appropriate forms satisfying legal requirements while maximizing the transparency and credibility that strengthen funding opportunities.

What happens immediately after missing a filing deadline?

Late filing penalties begin accruing based on organization size. Organizations with gross receipts over $1 million face penalties of $105 per day up to maximum $52,500. Smaller organizations face penalties of $20 per day up to lesser of $10,500 or 5% of gross receipts. Penalties accrue from the filing deadline until the return is filed, making prompt filing of delinquent returns financially important beyond just compliance concerns.

The three-year countdown toward automatic revocation starts. IRS tracks consecutive years without required filings. Missing one year doesn’t immediately revoke status but begins the countdown. If the organization files the second year’s return (even if late), the countdown resets. However, missing year two after missing year one creates serious urgency—you’re now one year away from automatic revocation requiring immediate corrective action.

TEOS database status remains active initially. After missing one filing deadline, the organization still appears in TEOS showing active status eligible to receive deductible contributions. Funders checking TEOS won’t immediately detect the filing failure. However, sophisticated funders requesting copies of recent Form 990 returns will discover the missing filing when organizations cannot provide the most recent year’s return.

IRS notices may or may not arrive. While IRS sometimes sends reminder notices about unfiled returns, don’t rely on receiving warnings. The IRS is not required to notify organizations before automatic revocation occurs. Many organizations only discover they’ve been revoked when checking TEOS database for other reasons or when funders inform them of revoked status during grant application due diligence.

What are the consequences of automatic revocation after three years?

Tax-exempt status terminates completely. After three consecutive years without required filings, IRS automatically revokes 501(c)(3) recognition effective the filing due date of the third missed year. The organization is no longer tax-exempt—any income generated after the effective date of revocation is potentially taxable as if the organization were a for-profit corporation. The determination letter becomes invalid and TEOS listing changes to “revoked” status.

Donor tax deductions become unavailable. Contributions made after the effective revocation date are not tax-deductible regardless of what the organization tells donors. Organizations continuing to solicit donations while claiming tax-deductibility after revocation commit fraud. Donors discovering their contributions weren’t actually deductible may demand refunds and can report organizations to IRS and state regulators for fraudulent solicitation.

Grant eligibility disappears immediately. Foundation and corporate grant programs verify tax-exempt status through TEOS searches before processing awards. Organizations showing “revoked” status fail basic eligibility requirements triggering automatic application rejection. Existing multi-year grants may be terminated when funders discover grantees lost tax-exempt status, potentially requiring return of already-disbursed funds depending on grant agreements.

Banking and vendor relationships face complications. Many banks, payment processors, donors management platforms, and vendors offer nonprofit pricing or services contingent on verified tax-exempt status. Loss of exemption may trigger account holds, service terminations, or repricing to for-profit rates. Organizations may be unable to process online donations through platforms like PayPal Giving Fund that verify tax-exempt status.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

Launch includes establishing filing systems preventing missed deadlines. Temecula nonprofits should create filing calendars with multiple advance reminders, assign clear responsibility for Form 990 preparation, and implement backup systems ensuring filings occur even when personnel changes happen.

Fix is precisely where organizations land after missing IRS filings. The Fix work involves filing all delinquent returns immediately, paying applicable penalties, applying for reinstatement if automatic revocation occurred, and establishing systems preventing future filing failures. Fix work is expensive and time-consuming—far better to prevent than remediate.

Fund access completely stops during revocation. Organizations cannot pursue grants while showing revoked TEOS status. Even after filing reinstatement applications, the processing period (often 3-6 months) prevents grant pursuit until TEOS updates showing restored active status. Every month in Fix mode is a month losing potential funding opportunities.

Federal Recognition was granted contingent on meeting ongoing filing requirements. Determination letters aren’t permanent guarantees—they represent recognition valid only while organizations maintain compliance including annual filing obligations. Missing filings voids the recognition determination originally granted.

CA Compliance Triangle operates independently of federal filing compliance. Organizations can miss IRS Form 990 filings while remaining current with California Secretary of State, Franchise Tax Board, and Attorney General—or vice versa. However, most Temecula nonprofits missing federal filings also miss California filings creating multiple concurrent compliance failures requiring simultaneous remediation.

Step-by-step: How NPLO helps organizations correct missed IRS filings

Step 1: Status Assessment We determine exactly which years have unfiled returns and whether revocation has occurred.

Step 2: TEOS Verification We check current TEOS listing confirming whether status shows active or revoked.

Step 3: Delinquent Return Preparation We prepare all missing Form 990/990-EZ/990-N returns for unfiled years.

Step 4: Penalty Calculation We calculate applicable late filing penalties and advise on reasonable cause abatement requests if circumstances warrant.

Step 5: Simultaneous Filing We file all delinquent returns together demonstrating commitment to compliance restoration.

Step 6: Reinstatement Application If revocation occurred, we prepare Form 1023 or 1024 applications requesting retroactive reinstatement.

Step 7: Status Monitoring We track reinstatement processing and TEOS updates confirming restored active status.

Step 8: Prevention Systems We establish filing calendars, responsibility assignments, and backup procedures preventing future missed filings.

Checklist: Correcting missed IRS filings

Immediate Actions:

- Check TEOS database determining current status

- Count consecutive years without filings

- Gather financial records for all unfiled years

- Determine which Form 990 version was required each year

- Calculate late filing penalties

Filing Delinquent Returns:

- Prepare accurate returns for each missed year

- Complete all required schedules

- Answer governance questions honestly

- Include explanatory statements about late filing

- File all delinquent returns promptly

If Revoked (3+ consecutive years):

- File all delinquent Form 990 returns

- Prepare Form 1023 or 1024 reinstatement application

- Request retroactive reinstatement to effective revocation date

- Pay user fees ($275 or $600)

- Include explanations of filing failure causes

- Demonstrate corrective measures preventing recurrence

After Reinstatement:

- Verify TEOS shows active status restored

- Update donor communications confirming deductibility restored

- Notify funders of restored status

- Resume grant applications

- Establish prevention systems

Prevention Going Forward:

- Create filing calendar with 90/60/30-day reminders

- Assign clear responsibility for preparation

- Establish backup person awareness

- Consider professional preparation assistance

- Review compliance quarterly

Quick Answers (PPA)

We just discovered we missed last year’s Form 990—should we file it immediately or wait until this year’s is due to file both together? File the missed return immediately—don’t wait. Filing late is far better than missing a second consecutive year which accelerates toward automatic revocation. You started the three-year countdown by missing one year; filing the delinquent return promptly stops that countdown and demonstrates good faith compliance effort potentially supporting penalty abatement. After filing the late return, ensure you file the current year’s return on time preventing any future gaps.

Can we request penalty abatement for late filing, or do we automatically have to pay? You can request reasonable cause abatement by submitting written explanation of circumstances preventing timely filing with your delinquent return. IRS may waive penalties if you demonstrate reasonable cause (serious illness, natural disaster, death of key personnel, unavoidable circumstance beyond organizational control) and that you acted responsibly by filing as soon as circumstances permitted. However, simply being disorganized, forgetting the deadline, or lacking funds to hire preparers typically don’t qualify as reasonable cause. Don’t assume automatic abatement—include detailed reasonable cause statement if requesting penalty waiver.

If we’re automatically revoked, can we just start a new nonprofit instead of going through reinstatement? Starting new organizations to avoid reinstatement creates significant problems. The new organization wouldn’t have your operating history, established reputation, existing contracts, donor relationships, or community recognition. Assets and liabilities from the old organization don’t automatically transfer to new entities—complex transactions would be required. Some funders track organizations that dissolved and reformed viewing it as attempt to escape accountability. Furthermore, the underlying causes of filing failure likely exist in the new organization too without corrective measures. Reinstatement is usually faster, simpler, and more appropriate than starting over.

How long does reinstatement take after filing the application? Reinstatement applications typically process in 3-6 months similar to original determination applications, though complex cases can take longer. Organizations cannot legitimately operate as tax-exempt or tell donors contributions are deductible during the processing period—you must wait for IRS approval and TEOS database update showing restored status. This processing delay is why prevention is so critical—every month without valid exemption is a month you can’t fundraise or pursue grants effectively.

Will funders hold the missed filings against us even after we’re reinstated? Many funders will ask about the circumstances of revocation and what measures you’ve implemented preventing recurrence. Honest acknowledgment of the failure, clear explanation of corrective actions, and demonstration of improved systems can rebuild funder confidence. However, some funders may view revocation as indicator of poor management regardless of subsequent correction. The best approach is transparency about what happened, accountability for the failure, and concrete evidence of improved compliance systems—don’t hide or minimize the revocation, but do demonstrate you’ve learned and improved.

What to do next (DIY vs Done-With-You)

DIY approach: Immediately check IRS TEOS database at apps.irs.gov/app/eos searching for your organization by name and EIN. Note whether status shows “Active” or “Revoked.” Count how many consecutive years you’ve missed filings—one year means urgency but not yet revoked, two consecutive years means extreme urgency and immediate action required, three or more means automatic revocation requiring reinstatement application. Gather financial records, bank statements, receipts, and program documentation for all unfiled years. Determine which Form 990 version was required each year based on revenue and asset thresholds at that time. Download appropriate forms and instructions from IRS website. Complete accurate returns for each missed year answering all questions honestly including governance questions. Consider including brief explanatory statement about why filing was late and what measures you’ve implemented preventing future failures. File all delinquent returns electronically through IRS-authorized e-file provider. If you’ve been revoked (three consecutive years missed), file all delinquent Form 990s first, then prepare Form 1023 or 1024 requesting retroactive reinstatement including detailed explanation of filing failure causes and corrective measures. After filing, monitor TEOS database weekly checking for status updates. Establish comprehensive filing calendar with multiple advance reminders preventing future missed filings. Assign clear responsibility for Form 990 preparation and establish backup procedures.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive missed filing correction for Temecula and Inland Empire nonprofits. We determine exactly which years have unfiled returns and current TEOS status, prepare all delinquent Form 990/990-EZ/990-N returns with accurate financial information and governance responses, calculate late filing penalties and advise on reasonable cause abatement requests if circumstances warrant, file all delinquent returns promptly demonstrating compliance restoration commitment, prepare reinstatement applications (Form 1023/1024) if automatic revocation occurred including persuasive explanations and corrective measures, track reinstatement processing and TEOS updates confirming restored active status, communicate with funders about restored status when appropriate, and establish prevention systems including filing calendars, responsibility assignments, and backup procedures preventing future filing failures. This ensures you correct filing failures as efficiently as possible, minimize penalties where reasonable cause exists, restore tax-exempt status through successful reinstatement, and prevent future compliance failures through improved systems.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Find Us Locally

Service Area: Moreno Valley, CA and surrounding areas

Coordinates: 33.9535, -117.2081

Address: 23945 Sunnymead Blvd. #4, Moreno Valley, CA 92553

Sources

- https://www.irs.gov/charities-non-profits/charitable-organizations

- https://www.irs.gov/forms-pubs/about-form-1023

- https://calnonprofits.org/

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.