05 Feb What’s the Difference Between a Nonprofit’s Mission and Its Activities for IRS Purposes?

Short Answer

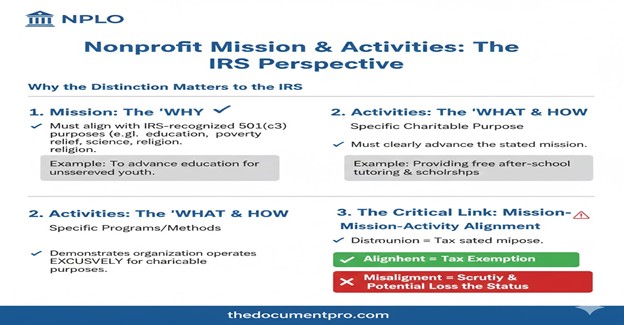

A nonprofit’s mission is the broad charitable purpose or goal the organization seeks to achieve—the “why” behind existence such as “advancing education” or “relieving poverty”—while activities are the specific methods, programs, and services the organization conducts to accomplish that mission—the “what” and “how” such as “providing tutoring” or “distributing food.” The IRS cares about this distinction because mission must fall within recognized 501(c)(3) charitable purposes qualifying for tax exemption, while activities must clearly advance the stated mission rather than serving unrelated purposes, and the relationship between mission and activities demonstrates whether the organization operates exclusively for charitable purposes or mixes charitable work with substantial non-charitable activities.

How does IRS distinguish mission statements from activity descriptions?

Mission represents organizational purpose at the highest level. Mission statements answer why the organization exists and what broad goal it pursues. “We advance education for underserved youth” is a mission. “We relieve poverty by promoting economic self-sufficiency” is a mission. These statements identify the charitable purpose category (education, poverty relief) and general target population without specifying exactly how the work will be accomplished.

Activities translate mission into concrete operational reality. Activities answer what the organization actually does on a day-to-day basis and how it accomplishes its mission. “We provide after-school tutoring three times weekly” is an activity. “We operate a job training program and food pantry” describes activities. These statements specify tangible programs, services, and operations that advance the mission.

Mission provides continuity while activities may evolve. An organization with the mission “advancing health through community wellness” could operate a fitness center, conduct health education workshops, or provide preventive screening clinics—all different activities serving the same mission. As community needs shift or funding changes, activities can be added, modified, or ended while mission remains constant. IRS expects mission stability but understands activity evolution.

The mission-activity relationship determines charitable qualification. IRS evaluates whether described activities logically advance the stated mission. An organization with education mission conducting tutoring programs shows clear alignment. An organization with education mission primarily running a restaurant shows questionable alignment—is the restaurant genuinely an educational program or an unrelated business generating income? The tighter the connection between mission and activities, the stronger the 501(c)(3) application.

What problems arise when mission and activities don’t align?

Activities unrelated to mission raise unrelated business income concerns. When substantial organizational activities don’t advance the charitable mission, IRS may determine that income from those activities is unrelated business income (UBI) subject to taxation. An organization with education mission operating a gift shop selling donated items might generate UBI if retail operations don’t have substantial relationship to educational purposes. Occasional UBI doesn’t jeopardize exemption, but substantial UBI suggests the organization isn’t operated exclusively for charitable purposes.

Mission creep occurs when activities expand beyond original charitable purposes. Organizations starting with focused missions sometimes add programs that don’t clearly connect. An organization with “youth education” mission that starts operating a senior center may be conducting charitable work, but the senior center activities don’t advance youth education mission. This doesn’t necessarily violate IRS rules if the organization properly described both youth and senior services in its purposes, but unexpected mission creep raises questions about whether the organization is operating as described in its determination application.

Vague mission statements create activity classification problems. If an organization’s mission is simply “helping the community,” IRS can’t evaluate whether specific activities advance that mission because the mission is too undefined. Specific missions like “providing health services to low-income families” allow clear assessment of whether activities (operating a free clinic, conducting health screenings, distributing medications) logically advance that purpose. Vague missions paired with diverse activities suggest lack of organizational focus.

Commercial activities disguised as mission work jeopardize exemption. Some organizations describe commercial enterprises as charitable activities when the connection is weak or non-existent. Operating a restaurant and claiming it advances education mission because employees learn job skills sounds charitable but may not satisfy IRS if the restaurant primarily functions as a commercial business competing with for-profit restaurants. The IRS looks for whether activities would be considered charitable independent of any educational or rehabilitative aspects attached to commercial operations.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

Launch includes articulating clear mission statements and developing activities obviously advancing that mission. San Bernardino nonprofits should ensure mission-activity alignment is apparent from formation documents and IRS applications preventing questions about whether operations serve genuine charitable purposes.

Fix addresses situations where organizational drift created misalignment between stated mission and actual activities, where mission statements are too vague to meaningfully guide operations, or where activities expanded beyond mission scope requiring either mission amendments or activity refocusing.

Fund depends on demonstrating mission-activity alignment because grant applications request both mission statements and program descriptions. Funders evaluate whether your activities logically accomplish your mission and whether mission aligns with their funding priorities. Misalignment between claimed mission and actual programs raises credibility concerns.

Federal Recognition requires proving to IRS that mission qualifies as charitable and that planned activities will advance that mission. Form 1023/1023-EZ applications ask separately about organizational purposes and specific activities because IRS evaluates both the charitable purpose itself and whether activities effectively pursue it.

CA Compliance Triangle includes Attorney General oversight ensuring charitable assets serve stated purposes. Significant deviation between stated mission in formation documents and actual organizational activities can trigger AG investigation about whether the organization is operating within its chartered purposes.

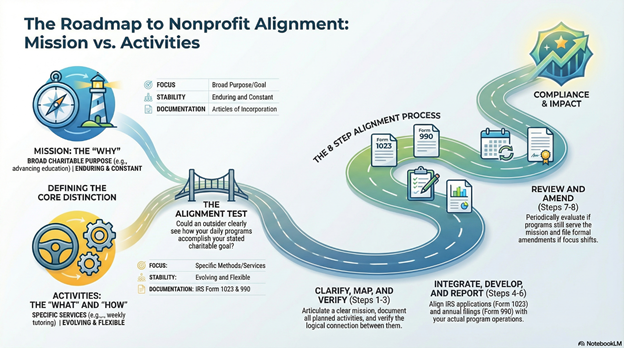

Step-by-step: How NPLO helps organizations maintain mission-activity alignment

Step 1: Mission Clarification We help articulate clear mission statements that are specific enough to guide operations but flexible enough to allow reasonable evolution.

Step 2: Activity Mapping We document all planned activities and verify each clearly advances the stated mission.

Step 3: Alignment Verification We assess whether the connection between mission and activities is obvious or requires explanation.

Step 4: IRS Application Integration We ensure Form 1023/1023-EZ applications present mission and activities showing clear logical connections.

Step 5: Program Development Guidance We help organizations considering new programs evaluate whether they align with existing mission or require mission amendments.

Step 6: Form 990 Consistency We ensure annual Form 990 program descriptions remain consistent with stated mission and IRS determination basis.

Step 7: Periodic Review We establish schedules for reviewing whether activities still align with mission as organizations evolve.

Step 8: Amendment Guidance When mission or activities change significantly, we guide proper IRS notification or amended application processes.

Checklist: Mission-activity alignment essentials

Mission Statement Should:

- Identify specific charitable purpose (education, poverty relief, health, etc.)

- Describe general goal or outcome pursued

- Indicate target population at high level

- Be stable and enduring

- Guide all organizational decisions

- Appear in Articles of Incorporation

- Be broad enough to encompass multiple programs

Activities Should:

- Clearly advance the stated mission

- Describe specific programs and services

- Explain methods and delivery approaches

- Specify who benefits directly

- Show logical connection to mission

- Be documented in IRS applications

- Evolve as needed to serve mission

Alignment Indicators:

- Someone unfamiliar with organization can see how activities accomplish mission

- Each major program connects to mission directly

- Activities wouldn’t make sense with different mission

- Mission explains why organization conducts its activities

Quick Answers (PPA)

Can we change our mission statement, or is it permanent once IRS approves it? Mission can change through formal amendment processes, but frequent mission changes raise questions about organizational stability and focus. Minor refinements to mission language don’t require IRS notification—clarifying “youth education” to “youth education and mentoring” when mentoring was always part of the work is reasonable evolution. Substantial mission changes adding new charitable purpose categories or fundamentally shifting focus may require filing amended determination applications. Before changing mission, consider whether the issue is actually mission needing change versus activities needing adjustment to better serve existing mission. Many organizations think they need new missions when they really need better activity alignment.

What if we want to add a program that doesn’t obviously connect to our mission—should we amend the mission or just not do the program? Evaluate whether the proposed program serves a charitable purpose that could reasonably be included in your organizational purposes. If it does and you genuinely want to pursue it, consider amending your Articles of Incorporation to broaden purposes appropriately and notifying IRS if the change is substantial. However, consider whether adding unfocused programs dilutes organizational effectiveness. Organizations known for excellence in specific areas often have greater impact than organizations pursuing scattered activities across multiple unrelated missions. Unless the new program genuinely fits your expertise and capacity, declining opportunities that don’t align with mission demonstrates good judgment rather than missed opportunity.

How specific should mission statements be—is “helping people” adequate? “Helping people” is far too vague to serve as organizational mission. Mission should identify which recognized charitable purpose you serve (education, poverty relief, health, community development, etc.) and generally who benefits. “Advancing education for underserved youth” is appropriately specific—it identifies charitable purpose category (education) and general beneficiary population (underserved youth) while allowing flexibility in specific programs and methods. Mission specificity helps IRS evaluate whether purposes qualify as charitable and helps funders understand whether your work aligns with their priorities.

Do activities have to match mission word-for-word, or can they serve the mission in creative ways? Activities don’t require literal word-matching but should have logical connections clear to outside observers. An organization with “environmental conservation” mission could conduct education programs teaching conservation practices, organize community cleanup events, advocate for environmental policies, or operate habitat restoration projects—all activities serving the mission through different approaches. The test is whether reasonable observers would agree activities advance the mission. Creative approaches are fine; tenuous connections that require elaborate explanations raise concerns.

What happens if we conduct activities that IRS determines don’t advance our mission? Activities not advancing exempt purposes generate unrelated business income taxable even for exempt organizations. Occasional UBI doesn’t jeopardize exemption, but substantial UBI or operations primarily focused on non-mission activities can result in IRS revoking 501(c)(3) status on grounds the organization isn’t operated exclusively for charitable purposes. If you discover activities have drifted from mission, either refocus activities to better serve mission, eliminate activities that don’t advance exempt purposes, or formally amend mission if activities serve different charitable purposes you genuinely want to pursue. Don’t continue substantial misalignment hoping IRS won’t notice.

What to do next (DIY vs Done-With-You)

DIY approach: Write your organization’s mission statement in one clear sentence identifying the charitable purpose and general goal. Then list all current or planned programs and activities. For each activity, write 1-2 sentences explaining how it advances the mission. If you struggle articulating the connection or if the explanation requires elaborate justification, the activity may not align well. Review your Articles of Incorporation verifying the stated purpose encompasses your current activities—if activities have drifted beyond chartered purposes, consider whether Articles need amendment. Review your most recent Form 990 comparing the program service accomplishments you reported with your stated mission ensuring consistency. If you’re planning new programs, evaluate them against mission asking “does this clearly advance our charitable purpose or does it pull us in new directions?” Consider whether mission needs broadening or whether proposed activities don’t fit organizational focus. Before changing mission substantially, consult with board about whether change serves organizational best interests or whether maintaining current focus with better-aligned activities would be stronger strategy.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive mission-activity alignment support for San Bernardino and Inland Empire nonprofits. We help articulate clear mission statements specific enough to guide decisions but flexible enough to allow reasonable program evolution, document and evaluate all planned or current activities verifying clear connections to mission, assess whether mission-activity alignment is obvious or requires improvement, ensure IRS applications and Form 990 filings present consistent mission and program relationships, guide organizations considering new programs through alignment analysis determining fit with existing mission, help organizations that have drifted from original mission decide whether refocusing activities or amending mission serves best interests, ensure ongoing alignment as organizations mature and programs evolve, and guide proper IRS notification when substantial mission or activity changes occur. This ensures your organization maintains the mission-activity coherence that IRS expects and that funders look for when evaluating whether your work aligns with their charitable priorities.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Find Us Locally

Service Area: Moreno Valley, CA and surrounding areas

Coordinates: 33.9535, -117.2081

Address: 23945 Sunnymead Blvd. #4, Moreno Valley, CA 92553

Sources

- https://www.irs.gov/charities-non-profits/charitable-organizations

- https://www.irs.gov/forms-pubs/about-form-1023

- https://calnonprofits.org/

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.