09 Feb What Is “Public Charity Status” and Why Do Funders Care?

Short Answer

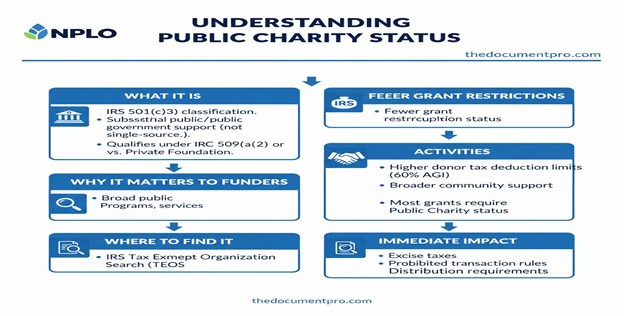

Public charity status is an IRS classification within 501(c)(3) designating organizations that receive substantial support from the general public or government rather than from a single source, qualifying under Section 509(a)(1), 509(a)(2), or 509(a)(3) rather than being classified as private foundations. Funders care because public charities face fewer restrictions on activities and grant-making, donors receive higher tax deduction limits for contributions to public charities versus private foundations, public charities demonstrate broader community support and engagement rather than single-source control, and most foundation and corporate grant programs explicitly restrict funding to public charities excluding private foundations from eligibility. The classification appears in IRS determination letters and matters immediately—organizations classified as private foundations face additional excise taxes, prohibited transaction rules, and mandatory distribution requirements that public charities avoid.

What distinguishes public charities from private foundations?

Public support requirements define the primary distinction. Public charities receive substantial portions of their funding from diverse sources—individual donations from many people, government grants, fees for charitable services, or support from other public charities. Private foundations typically receive funding from single sources—one wealthy individual, family, or corporation—and primarily make grants to other organizations rather than conducting direct programs. The public support test demonstrates that the organization serves broad public interests rather than private donor preferences.

Section 509(a) classifications specify different public charity types. Most operating nonprofits qualify as 509(a)(1) public charities receiving broad public support or 509(a)(2) public charities receiving substantial revenue from program service fees. Supporting organizations classified as 509(a)(3) support other public charities. Organizations not meeting any 509(a) public charity test automatically classify as private foundations under Section 509(a)—it’s the default classification when public charity status can’t be proven.

Operating versus grant-making focuses distinguish most public charities from most private foundations. Public charities typically conduct direct charitable programs—running schools, operating clinics, providing social services, conducting research. Private foundations primarily make grants to other organizations that conduct direct programs. While public charities can make grants and private foundations can operate programs, the predominant activity pattern differs between classifications.

Tax treatment differences create significant operational impacts. Private foundations pay 1-2% excise tax on net investment income. Private foundations face strict rules prohibiting self-dealing, excess business holdings, jeopardy investments, and taxable expenditures. Private foundations must distribute approximately 5% of assets annually. Public charities avoid these additional taxes and restrictions, operating under the same basic 501(c)(3) rules without foundation-specific complications.

Why do funders restrict grants to public charities?

Donor deduction limits favor public charity recipients. Individual donors can deduct contributions up to 60% of adjusted gross income for cash donations to public charities, but only 30% for contributions to private foundations. For appreciated property, limits are 30% for public charities versus 20% for private foundations. These higher deduction limits make public charities more attractive to major donors seeking maximum tax benefits, creating fundraising advantages.

Foundation grant-making rules complicate giving to private foundations. Private foundations making grants to other private foundations face “expenditure responsibility” requirements involving extensive documentation, monitoring, and reporting that don’t apply to grants to public charities. Many foundations avoid this administrative burden by restricting grants to public charities. Additionally, some foundation charters or policies explicitly limit giving to public charities as matter of preference or mission focus.

Public accountability expectations drive funder preferences. Public charities’ broader support base suggests community validation and engagement that private foundations’ single-source funding doesn’t demonstrate. Funders assume public charities responsive to diverse stakeholders operate more transparently and accountably than private foundations potentially dominated by single donor interests. Whether fair or not, this perception influences funding decisions.

Regulatory complexity avoidance motivates restrictions. Funders familiar with private foundation rules’ complexity may simply prefer supporting public charities to avoid dealing with foundation-specific regulations, even for legitimate foundation grantees. Grant administrators find public charity grants simpler to process and monitor than foundation grants requiring special considerations.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

Launch includes understanding public charity classification and structuring organizations to qualify. Most Temecula nonprofits conducting direct programs and seeking diverse funding sources will qualify as public charities automatically. Organizations considering private foundation structure should understand the implications.

Fix addresses rare situations where organizations expected public charity classification but received private foundation determination, requiring supplemental information demonstrating public support or appealing IRS classification. Most organizations receive expected classifications without problems.

Fund access depends heavily on public charity status because most institutional funders restrict grants to public charities. Organizations classified as private foundations face severely limited foundation and corporate grant opportunities, though they can still receive individual donations and pursue the smaller pool of funders willing to support foundations.

Federal Recognition determination letters specify classification. The IRS determination states whether the organization qualifies as a public charity under Section 509(a)(1), 509(a)(2), or 509(a)(3), or whether it’s classified as a private foundation. This classification profoundly affects operational requirements and funding access.

CA Compliance Triangle operates identically for public charities and private foundations—both need California Secretary of State, Franchise Tax Board, and Attorney General compliance. Classification difference is federal, not California-specific.

Step-by-step: How NPLO helps organizations achieve public charity classification

Step 1: Classification Assessment We evaluate whether planned funding models and activities will qualify for public charity status.

Step 2: Structure Optimization We help design funding strategies demonstrating broad public support for public charity qualification.

Step 3: Application Preparation We prepare IRS applications presenting organizational models clearly qualifying as public charities.

Step 4: Public Support Documentation We document diverse funding sources and public engagement demonstrating public charity qualification.

Step 5: Determination Verification We verify determination letters specify public charity classification under appropriate Section 509(a) subsection.

Step 6: Annual Maintenance We help organizations maintain public support percentages satisfying public charity tests ongoing.

Step 7: Reclassification Prevention We establish monitoring ensuring organizations don’t inadvertently lose public charity status.

Step 8: Funder Communication We help organizations communicate public charity status to funders when requested.

Checklist: Public charity vs private foundation comparison

Public Charities:

- Receive broad public support or program revenue

- Classified under Section 509(a)(1), (2), or (3)

- No excise tax on investment income

- No mandatory 5% distribution

- Fewer prohibited transaction restrictions

- Higher donor deduction limits (60% vs 30%)

- Qualify for most foundation grants

- Less complex regulatory requirements

Private Foundations:

- Funded primarily by single source

- Default classification if public charity tests not met

- 1-2% excise tax on investment income

- Must distribute ~5% of assets annually

- Strict self-dealing prohibitions

- Excess business holdings limits

- Lower donor deduction limits

- Limited foundation grant eligibility

- Complex expenditure responsibility rules

Why Most New Nonprofits Are Public Charities:

- Conducting direct programs (not just grant-making)

- Seeking diverse funding (not single-source)

- Want foundation grant eligibility

- Prefer simpler regulatory environment

Quick Answers (PPA)

How do we know if we’re classified as a public charity or private foundation? Your IRS determination letter explicitly states the classification. The letter will say you’re recognized as a 501(c)(3) organization and specify that you’re a “public charity” qualifying under Section 509(a)(1), 509(a)(2), or 509(a)(3). If the letter doesn’t specify public charity status or explicitly states private foundation classification, you’re a private foundation. The IRS TEOS database also shows classification. Most organizations conducting direct charitable programs with diverse funding are classified as public charities automatically unless something unusual about their funding model triggers foundation classification.

Can we change from private foundation to public charity classification, or vice versa? Yes, organizations can change classification in either direction though the process varies. Private foundations seeking public charity reclassification must demonstrate meeting public support tests for a statutory period (typically four years) then file Form 8734 requesting reclassification. Public charities that lose public support over time may automatically reclassify as private foundations unless they take corrective action. Most organizations don’t need to change—they receive appropriate classification initially and maintain it through consistent operations. Changes usually result from significant funding model shifts like receiving single large gift that overwhelms other support.

What happens if we’re classified as private foundation but wanted public charity status? If you believe the classification is incorrect, you can appeal through IRS administrative processes providing additional information demonstrating you meet public charity tests. However, if you’re genuinely funded primarily by a single source and don’t conduct substantial direct programs, private foundation may be the correct classification regardless of preference. Some organizations initially classified as private foundations due to startup funding from one source transition to public charity status as they develop broader support. If you’re operating as a true private foundation (single-source funded grant-maker), accept that classification and operate within foundation rules rather than fighting appropriate classification.

Do donors know or care whether we’re public charity or private foundation when making gifts? Sophisticated major donors absolutely care because of deduction limit differences. A donor in high tax bracket making $100,000 gift wants to know whether they can deduct 60% (public charity) or only 30% (private foundation) of their adjusted gross income. Smaller donors making contributions under deduction limits may not notice differences. When soliciting major gifts, be prepared to confirm your public charity status if asked—uncertainty about classification creates hesitation from donors whose advisors tell them to verify before making large gifts.

Can public charities make grants to other organizations like foundations do? Yes, public charities can make grants to other charities though most focus on direct programs. Unlike private foundations making grants to other organizations, public charities making grants don’t face expenditure responsibility requirements for grants to other public charities and don’t have mandatory 5% distribution requirements. Many community foundations, federated campaigns, and other public charities make grants as primary activity while maintaining public charity classification through their own diverse support. The operating-versus-grant-making distinction is typical but not absolute—classification depends on public support sources, not whether grants are made.

What to do next (DIY vs Done-With-You)

DIY approach: Locate your IRS determination letter and read the classification section. It will explicitly state whether you’re a public charity under Section 509(a)(1), 509(a)(2), or 509(a)(3), or whether you’re classified as a private foundation. If you’re a public charity (the most common classification), note which subsection you qualified under. Verify your TEOS listing also shows public charity classification. If you’re a private foundation but didn’t intend to be, evaluate whether the classification is actually correct based on your funding model—if you’re funded primarily by one source and make grants rather than operating direct programs, foundation classification may be appropriate. If you’re a public charity conducting direct programs with diverse funding but somehow received foundation classification, gather documentation of your actual operations and public support sources and consider requesting IRS reconsideration. For ongoing operations, monitor your funding sources ensuring you maintain public support percentages satisfying public charity tests—Form 990 Schedule A provides public support calculations you should review annually. When applying for grants, be prepared to confirm your public charity status if funders ask.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive public charity classification support for Temecula and Inland Empire nonprofits. We evaluate whether planned funding models and activities will qualify for public charity status, help design organizational structures and funding strategies demonstrating broad public support, prepare IRS applications presenting clear public charity qualification, document diverse funding and public engagement supporting classification, verify determination letters specify appropriate public charity classification, establish annual monitoring maintaining public support percentages, prevent inadvertent loss of public charity status through funding shifts, and help communicate classification to funders when requested. This ensures you achieve and maintain the public charity classification that opens funding doors and avoids private foundation regulatory complexity.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Find Us Locally

Service Area: Moreno Valley, CA and surrounding areas

Coordinates: 33.9535, -117.2081

Address: 23945 Sunnymead Blvd. #4, Moreno Valley, CA 92553

Sources

- https://www.irs.gov/charities-non-profits/charitable-organizations

- https://www.irs.gov/forms-pubs/about-form-1023

- https://calnonprofits.org/

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.