16 Jan What Are Common Compliance Red Flags That Scare Funders Away?

Short Answer

Common compliance red flags that scare funders away include suspended or revoked IRS tax-exempt status discovered through TEOS database verification, suspension by California Franchise Tax Board for delinquent filings, missing or expired Attorney General Registry of Charities registration, Secretary of State status showing anything other than “Active,” missed Form 990 annual filings creating automatic IRS revocation risk, governance red flags like no board meetings documented or conflict of interest policies absent, financial warning signs such as excessive administrative expenses or negative net assets, inconsistencies between different documents suggesting poor record-keeping or misrepresentation, and unresponsive or defensive communication when funders ask clarifying questions about compliance status. Eligibility varies by grant, but these red flags trigger immediate concern during due diligence because they indicate organizational dysfunction, legal exposure, or misuse risk that most funders cannot accept regardless of how compelling the program narrative appears.

What federal compliance red flags immediately concern grant reviewers?

IRS tax-exempt status problems represent the most serious federal red flag because they question whether the organization legally qualifies as a charitable nonprofit entitled to receive tax-deductible contributions. When funders verify applicants through the IRS TEOS database at apps.irs.gov/app/eos and discover the organization doesn’t appear, shows revoked status, or displays warnings about lost recognition, applications typically stop immediately regardless of program quality. Most funders cannot legally distribute charitable dollars to organizations lacking current federal tax exemption, making IRS status problems absolute dealbreakers rather than concerns that can be explained or excused.

Automatic IRS revocation for failure to file Form 990 for three consecutive years catches many Temecula nonprofits by surprise. Organizations assume that because they received determination letters years ago, their tax-exempt status is permanent. In reality, status is conditional on ongoing compliance with annual filing requirements—even very small organizations with gross receipts under $50,000 must file Form 990-N (e-postcard). When organizations miss three consecutive years of required filings, the IRS automatically revokes recognition without advance warning. Funders discovering this revocation during due diligence view it as evidence of fundamental governance failure and organizational incompetence.

Missing or incomplete Form 990 filings even short of automatic revocation raise serious concerns. Organizations current with IRS but with spotty filing histories—filing some years but not others, filing extremely late consistently, or submitting incomplete returns with errors or missing schedules—signal poor financial management and compliance awareness. Funders reviewing multi-year Form 990 histories on GuideStar or ProPublica Nonprofit Explorer notice these patterns and question whether grant funds will be managed responsibly by organizations that struggle with basic federal reporting obligations.

Determination letter problems create red flags when the letter presented is outdated, doesn’t match the organization’s current legal name, shows a different EIN than provided elsewhere in application materials, or appears altered or fraudulent. Some organizations present determination letters from parent organizations or former affiliations rather than their own current recognition. Others present letters that are decades old without understanding that while determination doesn’t typically expire, it can be revoked for noncompliance. Funders cross-reference determination letters against TEOS verification to catch discrepancies suggesting misrepresentation or confusion about organizational status.

What California-specific compliance red flags trigger immediate funder concern?

California Franchise Tax Board suspension status discovered during verification represents a serious red flag because it indicates the organization failed to file required annual Form 199 or Form 199N returns or didn’t pay associated fees. FTB suspension can occur even when organizations maintain current federal IRS recognition, creating the confusing scenario where a nonprofit is recognized by the IRS but suspended by California. Funders—particularly California-based foundations, corporate givers, and government agencies—view FTB suspension as evidence of poor state compliance management and often pause or reject applications until suspension is lifted.

Attorney General Registry of Charities problems raise red flags around legal authority to solicit charitable contributions in California. Organizations that never registered with the AG Registry despite being required to (most nonprofits must register within 30 days of first receiving assets), let their registration lapse by failing to file annual RRF-1 renewals, or show “delinquent” status in the AG Registry search at oag.ca.gov/charities are technically violating California charitable solicitation law. Funders discovering these problems face legal concerns—by giving money to an organization operating without proper fundraising authorization, are they facilitating illegal activity? Most funders won’t risk this exposure.

Secretary of State status showing anything other than “Active” creates immediate questions about the organization’s legal corporate existence and ability to conduct business in California. Status descriptors like “Suspended,” “Forfeited,” “Dissolved,” or “Surrendered” indicate serious problems with corporate compliance—typically missed Statement of Information filings or failure to maintain a current registered agent. Organizations showing these statuses cannot legally enter contracts, meaning grant agreements would be unenforceable. Most funders verify SOS status as part of basic due diligence and halt applications immediately when non-Active status appears.

Inconsistent information across California’s three agencies creates red flags even when each individual agency shows acceptable status. For example, an organization might show Active with Secretary of State but use a different address or slightly different legal name with Franchise Tax Board or Attorney General Registry. These inconsistencies suggest poor record-keeping, lack of coordination in filing requirements, or potential identity confusion between similarly named organizations. Funders notice discrepancies during multi-agency verification and question organizational competence and attention to detail.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

The Nonprofit Launch Office operates within a strategic framework designed to help California nonprofits move from formation to fundability:

Launch includes understanding common compliance red flags from day one so you avoid creating them through ignorance or neglect. Launch-phase organizations should establish systems ensuring all filings happen before deadlines, maintain consistent organizational information across all agencies, document governance practices that demonstrate functional oversight, and implement regular status verification preventing the surprise discovery of compliance problems when pursuing grants. Proper Launch prevents most red flags from ever emerging.

Fix is precisely what organizations showing red flags need—urgent remediation addressing specific compliance failures that block funding access. Fix work for Temecula nonprofits might include filing delinquent Form 990 returns and requesting IRS reinstatement after automatic revocation, submitting overdue Form 199 filings and paying penalties to lift Franchise Tax Board suspension, filing late RRF-1 renewals with Attorney General Registry to restore fundraising authorization, correcting Secretary of State status by filing overdue Statement of Information and paying restoration fees, and implementing governance improvements preventing recurrence. Fix is always more expensive and time-consuming than Launch would have been, but it’s essential for organizations already showing red flags.

Fund represents the compliance state where no red flags exist—all agencies show current status, all filings are timely, all governance documentation demonstrates functional oversight, and all financial records signal responsible management. Fund-phase organizations can pursue grants confidently knowing that due diligence verification will reveal clean compliance profiles rather than problems requiring explanation or correction. Maintaining Fund status requires ongoing vigilance and systems rather than assuming compliance maintains itself automatically.

Federal Recognition through IRS 501(c)(3) determination creates the foundation that must remain clean—any problems at the federal level (revocation, missed filings, determination letter issues) create the most serious red flags because they question fundamental charitable status. Organizations must view federal compliance as non-negotiable baseline rather than optional burden because federal problems block nearly all institutional funding regardless of state-level compliance quality.

CA Compliance Triangle represents California’s three-agency oversight system where problems with any single agency create red flags even when the other two show clean status. Funders verify all three agencies independently (Secretary of State, Franchise Tax Board, Attorney General Registry), so Temecula nonprofits cannot compensate for problems in one area with excellent status in another. The triangle structure requires simultaneous good standing across all three vertices plus the federal IRS foundation—weakness anywhere compromises the entire compliance profile.

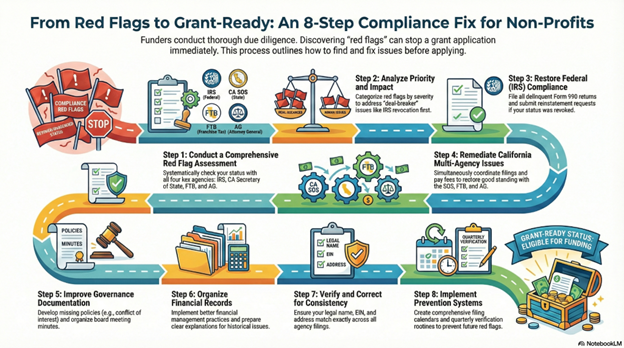

Step-by-step: How NPLO helps organizations address and eliminate red flags

Step 1: Comprehensive Red Flag Assessment We conduct systematic verification across all four agencies—IRS TEOS status, California Secretary of State entity status, Franchise Tax Board exemption status, and Attorney General Registry registration—to identify every red flag that funders would discover during due diligence. This complete assessment reveals the full scope of compliance problems rather than addressing issues piecemeal as they’re discovered. Many Temecula organizations are shocked to learn they have multiple simultaneous red flags they weren’t aware existed.

Step 2: Priority and Impact Analysis We categorize identified red flags by severity and urgency—which problems block all funding immediately (like IRS revocation or FTB suspension) versus which create concerns but don’t absolutely prevent applications (like slightly outdated board rosters or minor governance documentation gaps). This prioritization guides remediation strategy, ensuring you address dealbreaker problems before investing time in lower-priority improvements.

Step 3: Federal Compliance Restoration When IRS problems exist, we coordinate urgent remediation—filing all delinquent Form 990 returns for missed years, submitting Form 1023 reinstatement requests if automatic revocation occurred, obtaining replacement determination letters if originals are lost or problematic, and establishing filing calendar systems preventing future IRS problems. Federal restoration often takes months, during which grant pursuit typically must pause until status is clean.

Step 4: California Multi-Agency Remediation We coordinate simultaneous restoration across California’s three agencies—filing overdue Statement of Information and paying reinstatement fees to achieve Secretary of State Active status, submitting delinquent Form 199 returns and paying penalties to lift Franchise Tax Board suspension, and filing overdue RRF-1 renewals with Attorney General Registry to restore current registration. Multi-agency coordination is critical because remediation timelines differ and you need all three showing clean status simultaneously for full grant-readiness.

Step 5: Governance Documentation Improvement We address governance red flags by helping develop or update missing policies (conflict of interest, whistleblower, document retention), organize board meeting minutes demonstrating regular oversight, create comprehensive board rosters with current information, and implement governance practices that signal functional organizational management. These improvements show funders that past problems resulted from fixable gaps rather than fundamental dysfunction.

Step 6: Financial Record Organization When financial red flags exist—concerning Form 990 patterns, negative net assets, excessive administrative costs, or messy financial documentation—we help implement better financial management practices, prepare clear financial narratives explaining historical patterns, develop sustainability plans addressing structural financial problems, and organize financial documentation that demonstrates current fiscal responsibility despite past challenges.

Step 7: Consistency Verification and Correction We identify and correct inconsistencies across different documents and agencies—ensuring legal name matches exactly across IRS, California SOS, FTB, and AG Registry filings, confirming EIN appears identically in all materials, verifying addresses are current and consistent, and eliminating discrepancies that raise questions about organizational identity or record-keeping quality.

Step 8: Prevention System Implementation Once red flags are eliminated, we implement systems preventing recurrence—comprehensive filing calendars covering all federal and state obligations, quarterly compliance verification routines checking status across all agencies, governance practices ensuring board awareness of compliance obligations, and documentation protocols maintaining organized records that facilitate timely filings and accurate reporting.

Checklist: What you should verify to catch red flags before funders do

Temecula nonprofits should regularly check these areas where red flags commonly emerge:

- IRS TEOS database listing at apps.irs.gov/app/eos showing “Eligible to receive tax-deductible contributions” without revocation warnings

- Form 990 filing history on GuideStar/Candid showing complete, timely filings for every required year without gaps or patterns of extreme lateness

- IRS determination letter validity confirming it matches current legal name, shows correct EIN, and isn’t outdated or from a different organization

- California Secretary of State entity status showing “Active” rather than Suspended, Forfeited, Dissolved, or any problematic status

- Statement of Information currency with most recent filing within past two years during your designated filing month

- Registered agent current with valid California street address (not PO Box) and agent who actually receives and forwards legal notices

- Franchise Tax Board exemption status showing state tax exemption maintained without suspension flags

- Form 199 filing history showing annual California returns filed timely without major gaps or delinquencies

- Attorney General Registry registration showing current active status with valid CT number

- RRF-1 renewal currency with most recent filing within past 13 months of registration anniversary date

- Consistency across agencies with identical legal name, matching addresses (or documented reasons for differences), and coherent organizational identity

- Board meeting documentation with minutes from recent meetings showing active governance rather than rubber-stamping or inactivity

- Conflict of interest policy adopted by board with annual signed disclosures from all board members and key staff

- Financial policy documentation addressing approval authorities, internal controls, expense management, and oversight procedures

- Form 990 accuracy with program expense percentages reasonable (typically 65%+), administrative costs not excessive, compensation appropriate, and narrative descriptions matching grant applications

- Net asset trends showing financial sustainability rather than declining reserves, chronic deficits, or concerning financial trajectory

- Audit issues (if audited) with clean opinions rather than qualified opinions, material weaknesses, or going concern warnings

- Legal name consistency with identical organizational name across all documents, websites, marketing materials, and public communications

- EIN consistency with same nine-digit number used across all federal and state filings, bank accounts, and grant applications

- Responsive communication with funders when questions arise, providing complete answers rather than evasive or defensive responses

Quick Answers (PPA)

If we discover red flags during grant application preparation, should we still submit or wait until problems are fixed? Generally, wait until major red flags are corrected before submitting applications. Submitting applications with known IRS revocation, FTB suspension, or other serious compliance problems wastes time and often creates negative impressions with funders who may remember the problematic application when you reapply later with restored compliance. Minor red flags—slightly outdated documentation or small governance gaps—might be acceptable to explain if application deadlines are imminent and the program opportunity is time-sensitive. But major compliance failures should be fixed before applying. Contact funders directly to ask whether addressing red flags before submission or submitting with explanation of remediation in progress serves applications better.

How long does it typically take to resolve major red flags like IRS revocation or FTB suspension? Federal IRS reinstatement after automatic revocation typically requires 3-6 months minimum—you must file all delinquent Form 990 returns, submit reinstatement request, wait for IRS processing, and receive new determination letter. California Franchise Tax Board suspension lifts more quickly once delinquent returns are filed and penalties paid—often within 4-8 weeks. Attorney General Registry reinstatement from delinquent status usually processes within 2-4 weeks after filing overdue RRF-1. Secretary of State reinstatement to Active status can happen within days after filing overdue Statement of Information and paying fees. Total timeline for comprehensive compliance restoration across all agencies typically spans 4-8 months when multiple serious problems exist simultaneously.

Can we still apply for grants if we’re in the process of fixing red flags but not yet fully compliant? This depends heavily on the specific funder and the nature of the red flags. Some funders will conditionally approve grants contingent on compliance restoration by specific dates, particularly for organizations with strong programs and fixable administrative problems. Other funders maintain strict eligibility requirements and won’t consider applications until full compliance is documented. If pursuing grants during remediation, be completely transparent—”Our organization is currently addressing compliance gaps that resulted from [honest explanation]. We have filed delinquent returns, paid penalties, and expect full restoration by [date]. We are providing documentation of remediation progress.” Honesty sometimes preserves opportunities; hiding problems always creates worse outcomes when discovered.

What if only one agency shows problems but the other three are clean—will funders overlook it? Unfortunately, no. Funders conducting thorough due diligence verify all four agencies (IRS, CA SOS, CA FTB, CA AG Registry) independently, and problems with any single agency typically pause or reject applications. Being 3-for-4 on compliance doesn’t create 75% eligibility—it creates ineligibility until the fourth agency problem is resolved. This reflects the reality that each agency serves different legal purposes, and funders need confidence that organizations maintain all required registrations and filings. The multi-agency structure means you cannot compensate for weakness in one area with strength in another.

How do we prevent red flags from emerging in the first place? Prevention requires systematic compliance management rather than reactive problem-solving. Establish comprehensive filing calendars showing every deadline for IRS Form 990, California Form 199, Statement of Information, and RRF-1 renewals with advance reminders 90, 60, and 30 days before deadlines. Conduct quarterly status verification across all four agencies to catch problems early before they escalate. Assign clear board or staff responsibility for compliance tracking with backup coverage if primary responsible person changes roles. Document all governance practices—board meetings, policy adoptions, conflict disclosures—as they happen rather than retroactively creating documentation when grants require it. Treat compliance as continuous operational function rather than annual crisis when filing deadlines arrive.

What to do next (DIY vs Done-With-You)

DIY approach: Conduct honest self-assessment by verifying your organization’s status across all four verification points—search IRS TEOS database for your organization and confirm “Eligible” status without warnings, check California Secretary of State business entity search and verify “Active” status, look up Franchise Tax Board exemption status and confirm you’re not suspended, and search Attorney General Registry of Charities and verify current registration. Save dated screenshots documenting what you find. Review your Form 990 filing history on GuideStar or ProPublica Nonprofit Explorer and identify any missed years or concerning patterns. Compare information across different sources—does your legal name match exactly across all agencies, is your EIN consistent, are addresses current? List every red flag discovered with honest assessment of severity. Prioritize which problems absolutely block grant applications (IRS revocation, FTB suspension) versus which create concerns but might be explainable (minor governance gaps). Research how to address each red flag—which agencies to contact, what forms to file, what fees to pay. Create remediation plan with realistic timelines. Consider whether to pause grant applications until major red flags are resolved.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive red flag identification and remediation for Temecula and Inland Empire nonprofits facing compliance problems that block funding access. We conduct thorough verification across all four agencies identifying every red flag funders would discover, categorize problems by severity and urgency to guide efficient remediation, coordinate federal IRS compliance restoration including delinquent filing and reinstatement when necessary, manage California multi-agency remediation addressing Secretary of State, Franchise Tax Board, and Attorney General problems simultaneously, develop or improve governance documentation eliminating governance-related red flags, organize financial records and narratives addressing financial concerns, ensure consistency across all documents and agencies, implement prevention systems maintaining clean compliance going forward, and provide honest guidance about whether pursuing grants during remediation makes strategic sense or whether waiting for full restoration produces better outcomes. This comprehensive approach addresses red flags systemically rather than piecemeal, preventing the scenario where you fix one problem only to discover three others blocking grant access.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Sources

- IRS – Charitable Organizations

- IRS – Annual Exempt Organization Return: Who Must File

- IRS – Tax Exempt Organization Search (TEOS)

- California Secretary of State – Business Entities

- California Franchise Tax Board – Nonprofit Organizations

- California Attorney General – Charities

- CalNonprofits – California Nonprofit Resources & Advocacy

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.