23 Jan What Are Bylaws and Why Do They Matter for a New Nonprofit?

Short Answer

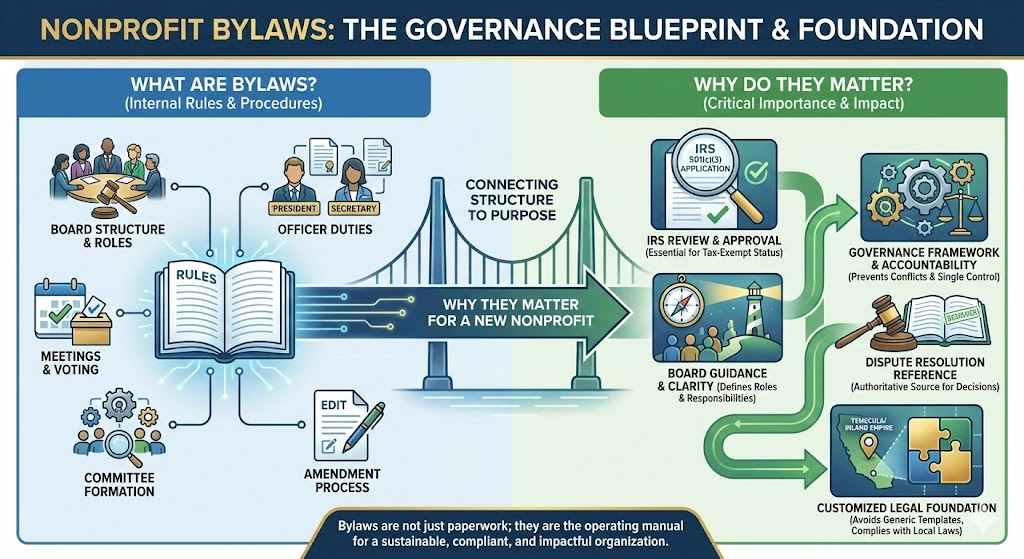

Bylaws are the internal governance rules and operational procedures that define how a nonprofit organization functions on a day-to-day basis, covering board structure and responsibilities, officer positions and duties, meeting requirements and voting procedures, committee formation and authority, membership provisions if applicable, amendment processes, and other operational protocols. These bylaws matter for new nonprofits because they establish the governance framework the IRS examines when evaluating 501(c)(3) applications, provide legal documentation of how the organization makes decisions and exercises oversight, create accountability mechanisms preventing single-person control or conflicts of interest, guide board members in understanding their roles and responsibilities, and serve as the authoritative reference for resolving governance questions or disputes throughout the organization’s existence. Eligibility varies by organization, but properly drafted and formally adopted bylaws represent one of the most critical governance documents new Temecula and Inland Empire nonprofits create during formation, requiring careful attention rather than casual adoption of generic templates that may not fit organizational needs or comply with California requirements.

What do bylaws actually contain and what decisions do they govern?

Board structure provisions form the core of nonprofit bylaws, specifying the number of directors (California requires minimum three), whether that number is fixed or within a range allowing flexibility, director term lengths and whether terms are staggered to ensure continuity, and whether term limits exist preventing perpetual board service. These provisions affect organizational stability and governance quality—boards that are too small lack diverse perspectives and skills, boards that are too large struggle with coordination and decision-making, and boards without term structures risk stagnation through directors serving decades without fresh perspectives or accountability through reelection.

Meeting requirements establish how often boards must convene (monthly, quarterly, annually), what constitutes quorum for conducting official business (typically majority of sitting directors), what advance notice directors must receive before meetings, whether meetings can occur virtually or must be in-person, and what voting procedures apply for different decision types. Meeting provisions balance ensuring adequate governance oversight through regular board engagement against respecting volunteer board members’ time constraints. Riverside nonprofits with all-volunteer boards might specify quarterly meetings as adequate for their operational complexity, while organizations with staff, facilities, and complex programs might require monthly board meetings for effective oversight.

Officer positions and duties sections identify required officers (California typically requires at minimum president/CEO, secretary, and treasurer though one person may hold multiple offices with limitations), describe the responsibilities and authority of each officer position, specify how officers are elected and for what terms, and establish procedures for officer removal or resignation. Officer provisions prevent governance confusion about who has authority to sign contracts, manage finances, maintain records, or represent the organization publicly. Clarity about officer roles also strengthens IRS applications by demonstrating functional governance rather than founder-dominated structures lacking genuine oversight.

Committee structures and authority provisions address whether standing committees will exist (finance, governance, program, fundraising, etc.), how committee members are appointed, what authority committees have to make decisions versus recommendations requiring full board approval, and what reporting requirements committees have to the full board. Committee provisions allow boards to distribute work efficiently and leverage specialized expertise without requiring every board member to be expert in finance, programs, and fundraising simultaneously. However, bylaws must clarify that ultimate authority remains with the full board rather than being delegated away to committees operating independently.

Why do bylaws matter specifically during nonprofit formation and IRS review?

IRS Form 1023 and 1023-EZ applications require submitting organizational bylaws as part of the 501(c)(3) determination process, with IRS reviewers examining bylaws to verify that governance structures meet federal requirements for tax-exempt charitable organizations. The IRS specifically looks for provisions demonstrating genuine board oversight rather than founder control, conflict of interest policies or procedures preventing self-dealing and private benefit, prohibition on distributing organizational assets or profits to individuals, and decision-making processes suggesting democratic governance rather than autocratic management.

Conflict of interest compliance represents a critical IRS focus area where bylaws often provide essential documentation. While separate conflict of interest policies are ideal, many organizations incorporate conflict provisions directly into bylaws—requiring annual disclosure of conflicts by all board members and officers, establishing procedures for handling conflicts when they arise in board decisions, prohibiting interested directors from voting on matters where conflicts exist, and ensuring that compensation or contract decisions involving board members receive independent review. Bylaws demonstrating robust conflict management strengthen IRS applications significantly because they address the agency’s fundamental concern about private individuals benefiting from charitable organization assets.

Private inurement prohibition language in bylaws reinforces similar requirements in Articles of Incorporation, clarifying that no part of organizational net earnings can benefit private individuals, that the organization operates exclusively for charitable purposes rather than private interests, and that any compensation paid to officers, employees, or contractors must be reasonable for services rendered. IRS reviewers want consistency between Articles of Incorporation (which contain legally required private inurement language) and bylaws (which operationalize those prohibitions through governance procedures), viewing discrepancies or contradictions as evidence of poor organizational planning or potential compliance risks.

Board independence from founder control emerges through bylaw provisions that IRS reviewers scrutinize carefully. Bylaws should demonstrate that boards exercise genuine oversight—not that founders appointed family members and friends who rubber-stamp founder decisions without independent judgment. Key indicators of independence include: boards with majority of unrelated, uncompensated directors; voting procedures requiring majority or supermajority approval rather than allowing single-person authority; term limits or regular reelection requirements ensuring directors remain accountable; and clear separation between board governance roles and staff operational roles preventing individuals from controlling both governance and operations.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

The Nonprofit Launch Office operates within a strategic framework designed to help California nonprofits move from formation to fundability:

Launch includes developing and formally adopting bylaws during the organizational meeting after California incorporation but before IRS Form 1023 submission. Launch-phase bylaw development determines whether you start with governance structures appropriate for your organizational size and complexity, whether you establish meeting requirements realistic for volunteer board members’ availability, whether you create officer positions matching your actual leadership structure, and whether you build in flexibility allowing growth and evolution without requiring frequent bylaw amendments. Proper Launch means bylaws strengthen rather than complicate IRS determination applications.

Fix addresses situations where original bylaws were problematic—generic templates adopted without customization creating provisions that don’t fit organizational reality, California-noncompliant language requiring revision to meet state nonprofit corporation law, missing provisions that IRS or funders expect to see in governance documents, or contradictions between bylaws and Articles of Incorporation raising questions about organizational coherence. Fix work involving bylaws typically requires board amendment votes, documentation of amendment approval in meeting minutes, and sometimes IRS notification if changes affect governance structures that were part of original determination basis.

Fund depends partly on bylaws because grant applications often request organizational bylaws as part of governance documentation proving functional oversight. Funders review bylaws to assess whether boards meet regularly (suggesting active engagement versus inactive rubber-stamping), whether conflict of interest procedures exist (reducing risk of grant fund misuse), whether decision-making processes are democratic (preventing single-person control of grant money), and whether the organization demonstrates professional governance practices. Well-drafted bylaws strengthen grant applications; missing or chaotic bylaws raise red flags about organizational management quality.

Federal Recognition through IRS 501(c)(3) determination depends directly on bylaw quality because bylaws are required application documents and because IRS reviewers examine governance structures carefully. Organizations with missing bylaws face application rejection or extensive IRS questions. Organizations with poorly drafted bylaws containing California-noncompliant provisions, private benefit language, or governance structures suggesting founder control face determination delays or denials requiring supplemental explanations and revisions.

CA Compliance Triangle (Secretary of State, Franchise Tax Board, Attorney General Registry) references governance structures established in bylaws even though bylaws themselves aren’t filed with state agencies. California Nonprofit Corporation Code establishes certain mandatory governance requirements—minimum three directors, certain fiduciary duties, specific meeting notice requirements—that bylaws must comply with. Bylaws that contradict California law create potential liability for board members and compliance concerns during state agency reviews or audits.

Step-by-step: How NPLO helps new nonprofits develop effective bylaws

Step 1: Organizational Needs Assessment We evaluate your specific governance needs based on organizational size, complexity, program scope, funding sources, and volunteer versus staff structure. A small all-volunteer organization with one program operates differently than an organization planning staff hires, multiple programs, and complex partnerships—bylaws should reflect actual operational reality rather than imposing unnecessary governance burden or providing insufficient oversight for organizational complexity.

Step 2: Board Structure Design We help determine appropriate board size for your organization (starting small with room to grow, or establishing larger boards from inception), whether fixed numbers or ranges provide better flexibility, what term lengths balance continuity with fresh perspectives (typically 2-3 year terms), and whether term limits or unlimited reelection better serves your governance goals. These decisions should consider your capacity to recruit quality board members—better to have seven engaged directors than fifteen disconnected ones.

Step 3: Meeting Requirements Development We establish meeting frequency realistic for your board members while ensuring adequate oversight (monthly may be excessive for small organizations, quarterly may be insufficient for complex operations), determine quorum requirements that allow business to proceed without requiring perfect attendance, specify notice periods giving members adequate preparation time, and address virtual meeting provisions particularly important post-pandemic when geographic barriers can be reduced through technology.

Step 4: Officer Position Specification We define which officer positions your organization needs (president, secretary, treasurer are standard; vice president, assistant secretary, or other positions are optional), clarify duties and authority for each position preventing role confusion, establish reasonable term lengths and succession procedures, and address whether officers must be board members or whether non-board staff can serve in certain officer capacities (particularly executive director relationships with board president).

Step 5: Conflict of Interest Integration We ensure bylaws include robust conflict of interest provisions—either incorporating full conflict policies directly into bylaws or referencing separate adopted conflict policies, establishing annual disclosure requirements for all board members, specifying procedures for handling conflicts when they arise in board decisions, and prohibiting interested parties from voting on matters where personal conflicts exist. Strong conflict provisions significantly strengthen IRS applications.

Step 6: Amendment Procedures Establishment We specify how bylaws can be amended in the future—typically requiring notice to board members of proposed amendments, supermajority votes (two-thirds or three-quarters) rather than simple majority to prevent casual changes, and documentation in meeting minutes. Amendment provisions balance allowing necessary evolution as organizations mature against preventing impulsive changes to fundamental governance structures.

Step 7: California Compliance Verification We review draft bylaws against California Nonprofit Corporation Code requirements ensuring compliance with mandatory state law provisions, verify that bylaw language doesn’t contradict Articles of Incorporation, confirm that governance structures meet both state and federal legal requirements, and eliminate provisions that might be unenforceable under California law even if they appear in generic national templates.

Step 8: Formal Adoption and Documentation We guide the organizational meeting where initial board formally adopts bylaws through recorded vote, ensure adoption is properly documented in meeting minutes with dates and vote tallies, verify that adopted bylaws are maintained in organizational records where board members and regulators can access them, and establish protocols for keeping bylaws current as amendments occur.

Checklist: What your bylaws should address

Well-drafted bylaws for Riverside nonprofits should include provisions covering:

- Organizational identification stating the nonprofit’s legal name and confirming it’s organized under California Nonprofit Public Benefit Corporation Law

- Board size and composition specifying number of directors (minimum three for California), whether fixed or range, and any diversity or qualification requirements

- Director terms and elections establishing term lengths (typically 2-3 years), whether terms are staggered, term limits if any, and election or reelection procedures

- Board meeting requirements specifying regular meeting frequency (monthly, quarterly, etc.), annual meeting requirements, special meeting procedures, and notice periods

- Quorum and voting defining what constitutes quorum (typically majority), what vote threshold is required for decisions (simple majority, supermajority for certain actions), and proxy or absentee voting provisions if allowed

- Officer positions and duties identifying required officers (president, secretary, treasurer minimum), describing responsibilities, specifying election procedures and terms, and addressing officer removal or resignation

- Committee structures establishing which standing committees exist (finance, governance, etc.), describing committee authority and limitations, specifying appointment procedures, and requiring committee reports to full board

- Conflict of interest provisions requiring annual disclosure of potential conflicts, establishing procedures for handling conflicts in board decisions, prohibiting interested directors from voting on conflicted matters, and ensuring independent review of compensation or contracts with board members

- Executive Director relationship (if applicable) clarifying that ED reports to board, ED attends board meetings in non-voting capacity, ED implements board policies but doesn’t set them, and clear separation between governance and operations exists

- Financial management addressing fiscal year designation, financial report requirements to board, audit or financial review requirements based on organization size, and approval authorities for budgets and expenditures

- Amendment procedures specifying how bylaws can be changed, what vote threshold is required (typically two-thirds or three-quarters), what notice of proposed amendments is required, and documentation requirements

- Dissolution provisions (optional but recommended) describing what happens to assets if organization dissolves, typically referencing the Articles of Incorporation dissolution clause directing assets to other 501(c)(3) organizations

- Indemnification (optional) providing that organization will defend and indemnify directors and officers against claims arising from their service, subject to legal limitations

- Document retention (optional but increasingly expected) establishing policies for maintaining organizational records including meeting minutes, financial documents, and legal filings

Quick Answers (PPA)

Can we just use a generic bylaws template from the internet, or do we need something customized? Generic templates provide useful starting points showing what sections bylaws typically include, but using templates without customization creates several problems. National templates may not comply with California Nonprofit Corporation Code requirements that differ from other states. Generic templates often include provisions inappropriate for your organization’s size, structure, or operational model—like complex committee structures that small all-volunteer organizations won’t actually use, or governance processes too informal for organizations planning to hire staff and pursue significant grants. Most importantly, bylaws should reflect actual governance decisions your founding board makes—how often will you realistically meet, what size board can you sustain, what officer structure fits your leadership—rather than imposing generic structures that don’t match organizational reality. The best approach involves starting with quality templates, then carefully customizing every provision to fit your specific needs and ensuring California compliance.

Do bylaws need to be filed anywhere like Articles of Incorporation, or are they just internal documents? Bylaws are internal governance documents not filed with California Secretary of State, IRS, or other government agencies during routine operations. However, bylaws are required attachments to IRS Form 1023/1023-EZ applications for 501(c)(3) determination, and funders commonly request bylaws as part of grant application documentation. Additionally, regulatory agencies can request bylaws during audits or investigations. While not publicly filed, bylaws are not secret documents—they should be maintained in organizational records accessible to board members, provided to IRS during determination process, shared with funders when requested, and potentially disclosed to Attorney General or other regulators conducting oversight. The practical reality is that bylaws function as semi-public governance documentation that should be professionally drafted and well-maintained rather than treated as casual internal paperwork.

How often should bylaws be updated or revised? Bylaws don’t require routine annual updates like some organizational policies. Well-drafted initial bylaws often serve organizations effectively for 5-10 years or longer without amendments. However, bylaws should be amended when organizational reality changes significantly—board size needs to expand or contract from original provisions, meeting frequency proves unrealistic requiring adjustment, officer positions need addition or restructuring, or legal requirements change necessitating compliance updates. Many organizations review bylaws every 3-5 years as part of governance self-assessment, identifying provisions that no longer fit operational reality or areas where amendments would improve governance effectiveness. The key is balancing stability (bylaws shouldn’t change constantly) with responsiveness (bylaws should reflect actual governance practices rather than becoming obsolete documents no one follows).

What’s the difference between what goes in Articles of Incorporation versus what goes in bylaws? Articles of Incorporation are the external legal document filed with California Secretary of State creating the corporate entity and containing legally required provisions: corporate name and address, statement of charitable purpose, dissolution clause, prohibition on private inurement, initial registered agent, and incorporator signature. Articles are public documents, difficult to amend (requiring state filing and fees), and legally establish the organization’s existence and tax-exempt eligibility basis. Bylaws are internal governance documents containing operational details: board size and structure, meeting requirements, officer positions and duties, committee structures, voting procedures, and amendment processes. Bylaws are not publicly filed (though shared when requested), easier to amend (requiring board vote without state filing), and govern day-to-day operations rather than establishing legal existence. Some provisions appear in both—particularly charitable purpose and private inurement language—with Articles providing legally required minimal statements and bylaws providing operational detail about how those legal requirements are implemented.

What happens if our board violates the bylaws—like holding fewer meetings than required or not following voting procedures? Bylaw violations create several potential problems depending on severity and context. Minor technical violations that don’t affect substantive decisions (like holding a meeting five days after the scheduled date rather than exactly on the calendar date) typically don’t create serious consequences if corrected. Significant violations affecting decision validity (like making major decisions without required quorum or supermajority votes) can render those decisions voidable, potentially requiring re-votes under proper procedures. Persistent bylaw violations suggest governance dysfunction that raises IRS concerns during audits, creates funder skepticism about organizational management, and potentially exposes board members to liability for breaching fiduciary duties. The best approach involves treating bylaws as binding governance requirements rather than suggestions, documenting when circumstances require waiving or modifying bylaw provisions (which boards can typically do through proper vote), and amending bylaws when provisions prove consistently unrealistic rather than simply ignoring inconvenient requirements.

What to do next (DIY vs Done-With-You)

DIY approach: Begin by reviewing several nonprofit bylaw templates from reputable sources like CalNonprofits.org, National Council of Nonprofits, or state association resources—compare templates to identify common sections and understand typical provisions. Research California Nonprofit Corporation Code basic requirements for directors (minimum three), meeting notice periods, and other mandatory provisions your bylaws must comply with. Make organizational decisions about governance structure: How many board members can you realistically recruit and sustain? How often can volunteer directors commit to meeting? What officer positions match your leadership structure? What committee structure (if any) fits your organizational complexity? Use template language as starting point, but customize every section to reflect your actual governance decisions rather than just accepting generic provisions. Ensure your bylaws include robust conflict of interest provisions either as separate articles or by reference to adopted conflict policies. Review draft bylaws against California legal requirements and IRS expectations before formal adoption. Hold proper organizational meeting where founding board reviews, discusses, and formally adopts bylaws through recorded vote, documenting adoption in meeting minutes. Maintain adopted bylaws in organizational records accessible to all board members and available for IRS submission and funder requests.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive bylaw development for Riverside and Inland Empire nonprofits, ensuring governance documents fit organizational needs while satisfying California law and IRS requirements. We assess your specific governance needs based on organizational size, complexity, and operational model, design appropriate board structures balancing oversight quality with volunteer capacity constraints, establish meeting requirements realistic for your board while ensuring adequate governance, define officer positions and duties matching your leadership structure, integrate robust conflict of interest provisions strengthening IRS applications, develop committee structures appropriate to organizational scale, verify California Nonprofit Corporation Code compliance throughout bylaw language, ensure consistency between bylaws and Articles of Incorporation, guide formal adoption at organizational meeting with proper documentation, and establish amendment procedures allowing future evolution as organizations mature. This comprehensive approach delivers professionally drafted, legally compliant, operationally appropriate bylaws that strengthen rather than complicate formation while establishing governance foundations supporting long-term organizational effectiveness and funder confidence.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Sources

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.