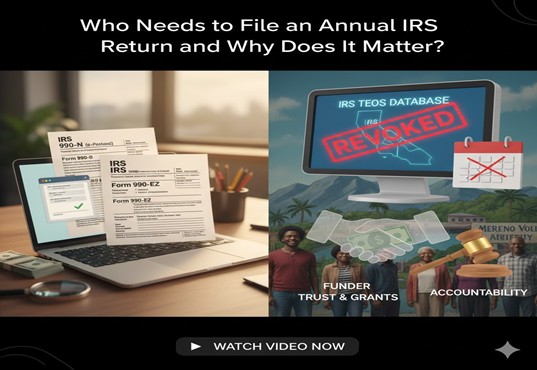

12 Feb Who Needs to File an Annual IRS Return and Why Does It Matter?

Short Answer

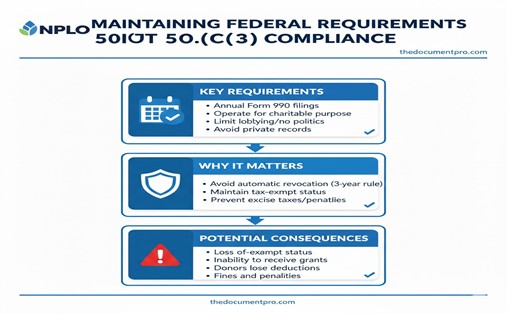

All 501(c)(3) organizations with IRS recognition must file annual information returns unless specifically exempted—organizations with gross receipts normally $50,000 or less file Form 990-N (e-Postcard), organizations with receipts under $200,000 and assets under $500,000 file Form 990-EZ, and organizations exceeding those thresholds file full Form 990. Annual filing matters because missing returns for three consecutive years triggers automatic revocation of tax-exempt status without further IRS notice, Form 990 is a public document that funders review when evaluating grant applications and organizational credibility, the return provides IRS oversight ensuring organizations operate for approved charitable purposes, and filing demonstrates organizational transparency and accountability to donors, regulators, and the communities served.

What determines which Form 990 version organizations must file?

Gross receipts and total assets determine form requirements. Organizations with gross receipts normally $50,000 or less file Form 990-N (e-Postcard), a simple online submission requiring basic information like organization name, EIN, principal officer, and confirmation that gross receipts remain under the threshold. Organizations with gross receipts under $200,000 AND total assets under $500,000 file Form 990-EZ, a simplified 4-page return with fewer schedules. Organizations exceeding either the $200,000 receipts or $500,000 assets threshold file full Form 990, a comprehensive return potentially spanning 20+ pages with multiple schedules.

Threshold calculations require understanding “gross receipts normally.” IRS uses a three-year average to determine normal gross receipts. A new organization’s first year uses actual receipts from that year. The second year averages years one and two. The third year and beyond average the current year plus prior two years. This smoothing prevents organizations from bouncing between forms yearly due to one-time large gifts or revenue fluctuations.

Total assets include all organizational property, investments, and resources at fair market value. Organizations must consider cash, accounts receivable, investments, equipment, buildings, land, and other assets when determining whether the $500,000 threshold is exceeded. Organizations with modest revenue but significant endowments or real estate holdings may need to file Form 990 rather than 990-EZ due to asset thresholds.

Certain organizations cannot use simplified forms regardless of size. Churches and church-affiliated organizations filing Form 990 cannot use Form 990-EZ. Organizations filing as supporting organizations or private foundations have specific form requirements. When uncertain which form to file, consult IRS instructions or tax professionals—filing wrong forms creates complications.

Why do funders review Form 990 returns during grant evaluation?

Financial health assessment occurs through Form 990 review. Funders examine revenue sources, expense categories, changes in net assets, and ending fund balances evaluating whether organizations are financially stable or struggling. Large deficits, declining revenue, minimal reserves, or concerning expense patterns raise questions about sustainability and capacity to manage grant funds effectively.

Governance quality indicators appear throughout Form 990. Organizations answer questions about conflict of interest policies, document retention policies, whistleblower policies, board meeting frequency, board independence, and compensation review processes. Funders interpret answers as signals about organizational maturity and management quality. Organizations answering “no” to governance questions look poorly managed regardless of program effectiveness.

Program spending ratios influence funder perceptions. Funders calculate what percentage of expenses support program activities versus administrative overhead and fundraising costs. While ratios vary by organization type and maturity stage, funders generally expect at least 60-75% of expenses supporting programs. Organizations showing high administrative percentages or excessive fundraising costs face scrutiny about efficiency and mission focus.

Compensation information reveals leadership structure and potential concerns. Form 990 requires disclosing compensation for officers, directors, key employees, and highest-compensated employees. Funders review this information evaluating whether compensation is reasonable for organizational size and region, whether multiple family members receive compensation suggesting nepotism, and whether compensation increases appear appropriate given organizational performance.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

Launch includes understanding filing obligations from inception. Moreno Valley nonprofits should establish Form 990 preparation systems, filing calendars, and recordkeeping practices supporting accurate annual returns before first deadline arrives—not scrambling at the last minute.

Fix becomes necessary when organizations missed Form 990 filings triggering automatic revocation, filed incorrect forms requiring amendment, or submitted returns with errors or omissions causing IRS questions. Correcting filing failures requires filing delinquent returns potentially with penalties and applying for reinstatement if revocation occurred.

Fund depends significantly on Form 990 quality because funders request recent returns as standard due diligence documents. Well-prepared returns demonstrating financial health, strong governance, and appropriate program spending strengthen applications. Problematic returns raising red flags weaken applications regardless of program proposals’ quality.

Federal Recognition requires maintaining filing compliance. IRS grants 501(c)(3) status expecting organizations will meet annual filing obligations demonstrating ongoing charitable operations. Recognition continues only while organizations maintain filing compliance and operational standards.

CA Compliance Triangle includes separate California filing requirements beyond Form 990. Organizations must file both IRS Form 990 AND California Form 199 with Franchise Tax Board, plus annual RRF-1 with Attorney General Registry. Filing federal Form 990 doesn’t satisfy California obligations.

Step-by-step: How NPLO helps organizations with Form 990 compliance

Step 1: Form Determination We evaluate which Form 990 version organizations must file based on receipts and assets thresholds.

Step 2: Information Gathering We collect financial records, program descriptions, governance documentation, and other information required for returns.

Step 3: Return Preparation We prepare complete accurate returns answering all questions and completing all required schedules.

Step 4: Governance Review We ensure governance question responses reflect actual practices and that supporting documentation exists.

Step 5: Board Review We prepare returns for board examination before filing ensuring accuracy and board awareness of reported information.

Step 6: Filing Management We file returns electronically through IRS-authorized providers ensuring timely submission.

Step 7: Record Retention We help establish systems preserving filed returns and supporting documentation for required periods.

Step 8: Funder Preparation We prepare Form 990 copies in formats funders commonly request for grant applications.

Checklist: Form 990 filing essentials

Determine Correct Form:

- Calculate 3-year average gross receipts

- Assess total assets at fair market value

- Identify: 990-N (<$50K), 990-EZ (<$200K receipts AND <$500K assets), or Form 990 (above thresholds)

Filing Deadline:

- 15th day of 5th month after fiscal year end

- May 15 for calendar-year organizations

- File Form 8868 for automatic 6-month extension if needed

Required Information:

- Complete financial statements

- Program service accomplishments

- Governance policies and practices

- Compensation information

- Related party transactions

- Required schedules based on activities

Governance Questions:

- Conflict of interest policy adopted

- Whistleblower policy adopted

- Document retention policy adopted

- Board meeting frequency

- Board independence (uncompensated/unrelated)

- Compensation review procedures

Public Disclosure:

- Make Form 990 available on request

- Post on organizational website (recommended)

- Understand information is public record

Quick Answers (PPA)

What if our revenue fluctuates significantly year to year—how do we know which form to file? Use the three-year rolling average for “normally” calculations smoothing fluctuations. If you had receipts of $30K, $75K, and $45K in the past three years, your average is $50K—right at the threshold where you could file 990-N or might need 990-EZ depending on how IRS interprets “normally.” When close to thresholds with fluctuating revenue, consider filing the more comprehensive form voluntarily to avoid risk of filing the wrong form. Organizations can always file Form 990 even if they qualify for simplified versions, though not vice versa.

Can we file Form 990-N (e-Postcard) if we’re well under $50K to save time, or should we file fuller returns? If you qualify for 990-N based on gross receipts normally under $50K, you can file it satisfying legal requirements. However, sophisticated funders prefer seeing fuller Form 990-EZ or 990 returns providing financial and program information that e-Postcard doesn’t contain. Organizations serious about pursuing grants often voluntarily file Form 990-EZ even when 990-N would suffice, providing transparency and information funders want. The additional preparation time investment often pays off through stronger grant applications.

What happens if we file the wrong Form 990 version—do we need to amend? Filing a more comprehensive form than required (Form 990 when you could have filed 990-EZ) isn’t a problem—you satisfied requirements. Filing a simpler form when you should have filed a more comprehensive version (990-EZ when you exceeded thresholds requiring full Form 990) may require amendment. IRS might accept the simpler filing if information is substantially complete, or might request that you file the correct form. When you discover you filed the wrong version, consult tax professionals about whether amendment is necessary or whether the filing adequately satisfied requirements given the circumstances.

Do we need to file Form 990 for the year we incorporated even if we had minimal activity? Yes, filing requirements begin the fiscal year you receive IRS determination or, for organizations operating before determination, the year activities commenced. Even with minimal activity, file the appropriate form showing limited revenue and expenses. Don’t assume you don’t need to file—starting the three-year countdown toward automatic revocation by not filing your first year is poor beginning. Filing shows IRS and future funders that you understand compliance obligations from inception.

What if we disagree with something in our filed Form 990—can we correct it after submission? Yes, file Form 990-X (Amended Return) correcting errors or omissions. However, consider whether corrections are necessary versus preferable. Material errors affecting financial information, program descriptions, or governance responses should be corrected. Minor typos or immaterial errors might not warrant amendment. Don’t file amended returns simply because you wish you had phrased something differently—amendments should correct actual errors or add required information that was omitted. Frequent amendments raise questions about recordkeeping quality.

What to do next (DIY vs Done-With-You)

DIY approach: Determine which Form 990 version you must file by calculating your three-year average gross receipts and assessing total assets. Mark your filing deadline (15th day of 5th month after fiscal year end) on calendar with 90-day, 60-day, and 30-day advance reminders. Gather complete financial records including revenue sources, expense categories, and year-end financial statements. Document all program activities with participant numbers, services provided, and outcomes achieved. Compile governance documentation showing board meetings, policy adoptions, and decision-making processes. Download appropriate Form 990 version and instructions from IRS website. Review instructions carefully—don’t guess at questions. Complete return accurately answering all questions and completing all required schedules. Have board treasurer or finance committee review draft return before filing. Consider having board vote approving final return creating documentation that board reviewed financial reporting. File electronically through IRS-authorized e-file provider. Save filed return and all supporting documentation for minimum seven years. Provide copy to accountant or tax preparer preparing next year’s return. Post Form 990 on organizational website or maintain system for providing copies when requested.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive Form 990 preparation and filing support for Moreno Valley and Inland Empire nonprofits. We determine which form version organizations must file based on accurate threshold calculations, gather all required financial and programmatic information through systematic collection processes, prepare complete accurate returns reflecting organizational activities and governance, ensure governance question responses match actual practices with supporting documentation, prepare returns for board review with explanations of reported information, file returns electronically through IRS-authorized providers ensuring timely submission, establish record retention systems preserving returns and documentation, prepare funder-ready copies for grant applications, and guide amendment processes when corrections are needed. This ensures your Form 990 satisfies IRS requirements while presenting your organization favorably to funders evaluating financial health, governance quality, and program effectiveness.

What happens immediately after missing a filing deadline?

Late filing penalties begin accruing based on organization size. Organizations with gross receipts over $1 million face penalties of $105 per day up to maximum $52,500. Smaller organizations face penalties of $20 per day up to lesser of $10,500 or 5% of gross receipts. Penalties accrue from the filing deadline until the return is filed, making prompt filing of delinquent returns financially important beyond just compliance concerns.

The three-year countdown toward automatic revocation starts. IRS tracks consecutive years without required filings. Missing one year doesn’t immediately revoke status but begins the countdown. If the organization files the second year’s return (even if late), the countdown resets. However, missing year two after missing year one creates serious urgency—you’re now one year away from automatic revocation requiring immediate corrective action.

TEOS database status remains active initially. After missing one filing deadline, the organization still appears in TEOS showing active status eligible to receive deductible contributions. Funders checking TEOS won’t immediately detect the filing failure. However, sophisticated funders requesting copies of recent Form 990 returns will discover the missing filing when organizations cannot provide the most recent year’s return.

IRS notices may or may not arrive. While IRS sometimes sends reminder notices about unfiled returns, don’t rely on receiving warnings. The IRS is not required to notify organizations before automatic revocation occurs. Many organizations only discover they’ve been revoked when checking TEOS database for other reasons or when funders inform them of revoked status during grant application due diligence.

What are the consequences of automatic revocation after three years?

Tax-exempt status terminates completely. After three consecutive years without required filings, IRS automatically revokes 501(c)(3) recognition effective the filing due date of the third missed year. The organization is no longer tax-exempt—any income generated after the effective date of revocation is potentially taxable as if the organization were a for-profit corporation. The determination letter becomes invalid and TEOS listing changes to “revoked” status.

Donor tax deductions become unavailable. Contributions made after the effective revocation date are not tax-deductible regardless of what the organization tells donors. Organizations continuing to solicit donations while claiming tax-deductibility after revocation commit fraud. Donors discovering their contributions weren’t actually deductible may demand refunds and can report organizations to IRS and state regulators for fraudulent solicitation.

Grant eligibility disappears immediately. Foundation and corporate grant programs verify tax-exempt status through TEOS searches before processing awards. Organizations showing “revoked” status fail basic eligibility requirements triggering automatic application rejection. Existing multi-year grants may be terminated when funders discover grantees lost tax-exempt status, potentially requiring return of already-disbursed funds depending on grant agreements.

Banking and vendor relationships face complications. Many banks, payment processors, donors management platforms, and vendors offer nonprofit pricing or services contingent on verified tax-exempt status. Loss of exemption may trigger account holds, service terminations, or repricing to for-profit rates. Organizations may be unable to process online donations through platforms like PayPal Giving Fund that verify tax-exempt status.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

Launch includes establishing filing systems preventing missed deadlines. Temecula nonprofits should create filing calendars with multiple advance reminders, assign clear responsibility for Form 990 preparation, and implement backup systems ensuring filings occur even when personnel changes happen.

Fix is precisely where organizations land after missing IRS filings. The Fix work involves filing all delinquent returns immediately, paying applicable penalties, applying for reinstatement if automatic revocation occurred, and establishing systems preventing future filing failures. Fix work is expensive and time-consuming—far better to prevent than remediate.

Fund access completely stops during revocation. Organizations cannot pursue grants while showing revoked TEOS status. Even after filing reinstatement applications, the processing period (often 3-6 months) prevents grant pursuit until TEOS updates showing restored active status. Every month in Fix mode is a month losing potential funding opportunities.

Federal Recognition was granted contingent on meeting ongoing filing requirements. Determination letters aren’t permanent guarantees—they represent recognition valid only while organizations maintain compliance including annual filing obligations. Missing filings voids the recognition determination originally granted.

CA Compliance Triangle operates independently of federal filing compliance. Organizations can miss IRS Form 990 filings while remaining current with California Secretary of State, Franchise Tax Board, and Attorney General—or vice versa. However, most Temecula nonprofits missing federal filings also miss California filings creating multiple concurrent compliance failures requiring simultaneous remediation.

Step-by-step: How NPLO helps organizations correct missed IRS filings

Step 1: Status Assessment We determine exactly which years have unfiled returns and whether revocation has occurred.

Step 2: TEOS Verification We check current TEOS listing confirming whether status shows active or revoked.

Step 3: Delinquent Return Preparation We prepare all missing Form 990/990-EZ/990-N returns for unfiled years.

Step 4: Penalty Calculation We calculate applicable late filing penalties and advise on reasonable cause abatement requests if circumstances warrant.

Step 5: Simultaneous Filing We file all delinquent returns together demonstrating commitment to compliance restoration.

Step 6: Reinstatement Application If revocation occurred, we prepare Form 1023 or 1024 applications requesting retroactive reinstatement.

Step 7: Status Monitoring We track reinstatement processing and TEOS updates confirming restored active status.

Step 8: Prevention Systems We establish filing calendars, responsibility assignments, and backup procedures preventing future missed filings.

Checklist: Correcting missed IRS filings

Immediate Actions:

- Check TEOS database determining current status

- Count consecutive years without filings

- Gather financial records for all unfiled years

- Determine which Form 990 version was required each year

- Calculate late filing penalties

Filing Delinquent Returns:

- Prepare accurate returns for each missed year

- Complete all required schedules

- Answer governance questions honestly

- Include explanatory statements about late filing

- File all delinquent returns promptly

If Revoked (3+ consecutive years):

- File all delinquent Form 990 returns

- Prepare Form 1023 or 1024 reinstatement application

- Request retroactive reinstatement to effective revocation date

- Pay user fees ($275 or $600)

- Include explanations of filing failure causes

- Demonstrate corrective measures preventing recurrence

After Reinstatement:

- Verify TEOS shows active status restored

- Update donor communications confirming deductibility restored

- Notify funders of restored status

- Resume grant applications

- Establish prevention systems

Prevention Going Forward:

- Create filing calendar with 90/60/30-day reminders

- Assign clear responsibility for preparation

- Establish backup person awareness

- Consider professional preparation assistance

- Review compliance quarterly

Quick Answers (PPA)

We just discovered we missed last year’s Form 990—should we file it immediately or wait until this year’s is due to file both together? File the missed return immediately—don’t wait. Filing late is far better than missing a second consecutive year which accelerates toward automatic revocation. You started the three-year countdown by missing one year; filing the delinquent return promptly stops that countdown and demonstrates good faith compliance effort potentially supporting penalty abatement. After filing the late return, ensure you file the current year’s return on time preventing any future gaps.

Can we request penalty abatement for late filing, or do we automatically have to pay? You can request reasonable cause abatement by submitting written explanation of circumstances preventing timely filing with your delinquent return. IRS may waive penalties if you demonstrate reasonable cause (serious illness, natural disaster, death of key personnel, unavoidable circumstance beyond organizational control) and that you acted responsibly by filing as soon as circumstances permitted. However, simply being disorganized, forgetting the deadline, or lacking funds to hire preparers typically don’t qualify as reasonable cause. Don’t assume automatic abatement—include detailed reasonable cause statement if requesting penalty waiver.

If we’re automatically revoked, can we just start a new nonprofit instead of going through reinstatement? Starting new organizations to avoid reinstatement creates significant problems. The new organization wouldn’t have your operating history, established reputation, existing contracts, donor relationships, or community recognition. Assets and liabilities from the old organization don’t automatically transfer to new entities—complex transactions would be required. Some funders track organizations that dissolved and reformed viewing it as attempt to escape accountability. Furthermore, the underlying causes of filing failure likely exist in the new organization too without corrective measures. Reinstatement is usually faster, simpler, and more appropriate than starting over.

How long does reinstatement take after filing the application? Reinstatement applications typically process in 3-6 months similar to original determination applications, though complex cases can take longer. Organizations cannot legitimately operate as tax-exempt or tell donors contributions are deductible during the processing period—you must wait for IRS approval and TEOS database update showing restored status. This processing delay is why prevention is so critical—every month without valid exemption is a month you can’t fundraise or pursue grants effectively.

Will funders hold the missed filings against us even after we’re reinstated? Many funders will ask about the circumstances of revocation and what measures you’ve implemented preventing recurrence. Honest acknowledgment of the failure, clear explanation of corrective actions, and demonstration of improved systems can rebuild funder confidence. However, some funders may view revocation as indicator of poor management regardless of subsequent correction. The best approach is transparency about what happened, accountability for the failure, and concrete evidence of improved compliance systems—don’t hide or minimize the revocation, but do demonstrate you’ve learned and improved.

What to do next (DIY vs Done-With-You)

DIY approach: Immediately check IRS TEOS database at apps.irs.gov/app/eos searching for your organization by name and EIN. Note whether status shows “Active” or “Revoked.” Count how many consecutive years you’ve missed filings—one year means urgency but not yet revoked, two consecutive years means extreme urgency and immediate action required, three or more means automatic revocation requiring reinstatement application. Gather financial records, bank statements, receipts, and program documentation for all unfiled years. Determine which Form 990 version was required each year based on revenue and asset thresholds at that time. Download appropriate forms and instructions from IRS website. Complete accurate returns for each missed year answering all questions honestly including governance questions. Consider including brief explanatory statement about why filing was late and what measures you’ve implemented preventing future failures. File all delinquent returns electronically through IRS-authorized e-file provider. If you’ve been revoked (three consecutive years missed), file all delinquent Form 990s first, then prepare Form 1023 or 1024 requesting retroactive reinstatement including detailed explanation of filing failure causes and corrective measures. After filing, monitor TEOS database weekly checking for status updates. Establish comprehensive filing calendar with multiple advance reminders preventing future missed filings. Assign clear responsibility for Form 990 preparation and establish backup procedures.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive missed filing correction for Temecula and Inland Empire nonprofits. We determine exactly which years have unfiled returns and current TEOS status, prepare all delinquent Form 990/990-EZ/990-N returns with accurate financial information and governance responses, calculate late filing penalties and advise on reasonable cause abatement requests if circumstances warrant, file all delinquent returns promptly demonstrating compliance restoration commitment, prepare reinstatement applications (Form 1023/1024) if automatic revocation occurred including persuasive explanations and corrective measures, track reinstatement processing and TEOS updates confirming restored active status, communicate with funders about restored status when appropriate, and establish prevention systems including filing calendars, responsibility assignments, and backup procedures preventing future filing failures. This ensures you correct filing failures as efficiently as possible, minimize penalties where reasonable cause exists, restore tax-exempt status through successful reinstatement, and prevent future compliance failures through improved systems.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Find Us Locally

Service Area: Moreno Valley, CA and surrounding areas

Coordinates: 33.9535, -117.2081

Address: 23945 Sunnymead Blvd. #4, Moreno Valley, CA 92553

Sources

- https://www.irs.gov/charities-non-profits/charitable-organizations

- https://www.irs.gov/forms-pubs/about-form-1023

- https://calnonprofits.org/

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.