14 Jan Can a New Nonprofit Realistically Win Grants in Its First Year?

Short Answer

New nonprofits can realistically win grants in their first year if they complete federal 501(c)(3) recognition early in that year, maintain current compliance with California’s three-agency requirements (Secretary of State, Franchise Tax Board, Attorney General Registry), target funders who specifically support emerging organizations or capacity building, demonstrate strong leadership and governance despite limited operational history, and pursue modest initial awards from local or regional sources rather than attempting large national grants requiring extensive track records. Eligibility varies by grant, but first-year success depends more on targeting appropriate funders who value organizational potential and community need over established performance history, while maintaining the compliance profile and documentation organization that allows credible applications despite newness.

What types of grants are actually accessible to first-year nonprofits?

Community foundation grants from regional funders like the Inland Empire Community Foundation often include programs specifically designed for emerging organizations. These funders understand that new nonprofits address emerging community needs or bring fresh approaches to persistent problems, and they’ve built funding programs that value potential and innovation alongside established performance. Community foundation grants to first-year organizations typically range from $5,000-$25,000, providing meaningful seed funding while limiting funder risk through modest award amounts.

Corporate giving programs from businesses with local operations in Riverside and the Inland Empire frequently support new nonprofits, particularly when the nonprofit’s mission aligns with corporate community investment priorities. Corporate funders making decisions locally (rather than through national headquarters) often exercise flexibility in supporting promising new organizations led by trusted community members. Small business sponsorships, employee volunteer grants, and corporate matching gift programs may be accessible even to very new nonprofits with strong community connections.

Individual donor campaigns represent the most accessible funding for first-year nonprofits because individuals don’t typically impose the institutional eligibility requirements that foundations and government funders enforce. Crowdfunding platforms, direct solicitation from personal networks, fundraising events, and major donor cultivation all remain open to new organizations regardless of operational history. Many successful first-year nonprofits build individual donor bases that provide operating support while they develop the track record needed for institutional grants.

Small grassroots grants from service clubs, religious institutions, neighborhood associations, and informal community groups often support first-year nonprofits addressing hyperlocal needs. These funders make modest awards ($500-$5,000) based on relationships, community knowledge, and direct observation of need rather than through formal application processes requiring extensive documentation. While grassroots grants don’t typically provide large amounts individually, they accumulate into meaningful support and build credibility for subsequent institutional applications.

Government grants and large national foundation programs generally remain inaccessible to first-year nonprofits because they require demonstrated capacity, extensive performance history, audited financials, and proven program models. New organizations should generally avoid investing time in applications for these highly competitive funding sources until they’ve accumulated 2-3 years of operations, successful program delivery, and documented outcomes that competitive review processes reward.

What obstacles do first-year nonprofits face that affect grant competitiveness?

Limited operational history creates the primary barrier because funders evaluate applications based partly on past performance predicting future success. When reviewers ask “Has this organization delivered similar programs successfully before?” the honest answer for first-year nonprofits is “No, not under our current structure, though individual leaders may have relevant experience.” This lack of organizational track record doesn’t automatically disqualify applications, but it shifts evaluation focus entirely onto leadership credentials, community partnerships, needs documentation, and program design quality rather than proven effectiveness.

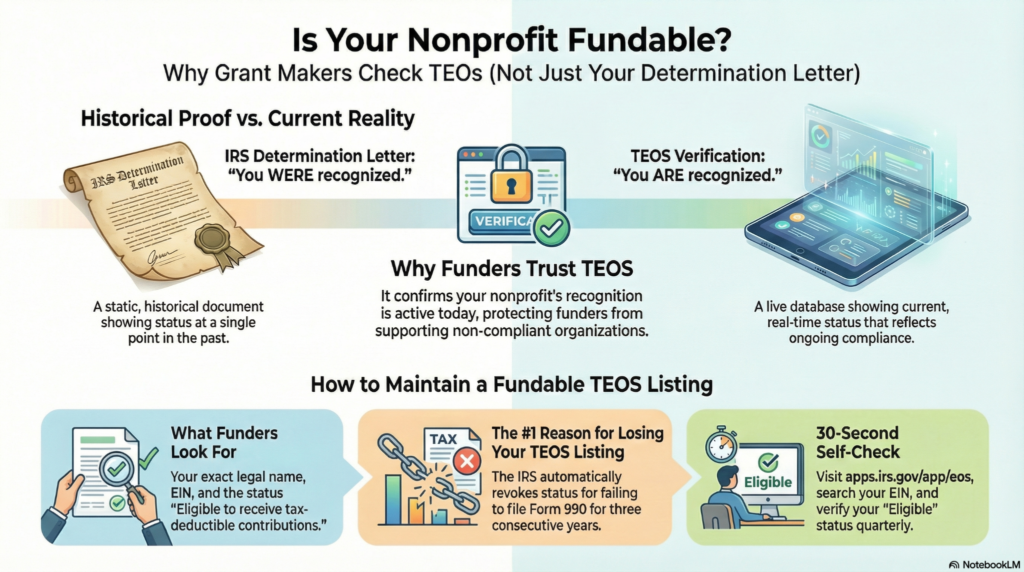

Missing financial history affects competitiveness because many grant applications request multiple years of audited financials, Form 990 filings, or financial statements demonstrating fiscal management capacity. First-year Riverside nonprofits often haven’t filed their first Form 990 yet because it’s not due until the 15th day of the 5th month after their first fiscal year ends. Explaining limited financial history in cover letters helps, but some funders use years of financial data as a screening criterion that automatically eliminates very new applicants regardless of program quality.

Incomplete compliance documentation emerges when first-year nonprofits received IRS determination late in their first year or haven’t yet completed all California registrations. Applications submitted while you’re waiting for IRS determination face rejection from most institutional funders. Applications submitted before registering with the Attorney General Registry of Charities raise legal compliance questions. The timeline to achieve full grant-ready status—completing incorporation, securing IRS recognition, registering with all California agencies, adopting governance policies, filing initial compliance renewals—typically spans 6-12 months minimum, limiting how early in your first year grants become feasible.

Lack of established relationships with funders means program officers don’t know your organization, haven’t conducted site visits, and can’t draw on informal knowledge about your work when evaluating applications. Established nonprofits benefit from years of relationship cultivation—attending funder events, meeting with program officers, participating in grantee convenings, demonstrating consistent performance. First-year organizations start with none of these relationship advantages, requiring applications to stand entirely on documented merit rather than supplemented by relational confidence.

Limited program outcomes and impact data reflect the reality that you haven’t operated long enough to demonstrate results. Applications asking “What outcomes did you achieve in the past three years?” cannot be answered substantively by six-month-old organizations. First-year applicants must present logic models, outcome frameworks, and anticipated results rather than actual measurements, which reviewers inherently trust less than proven track records of effectiveness.

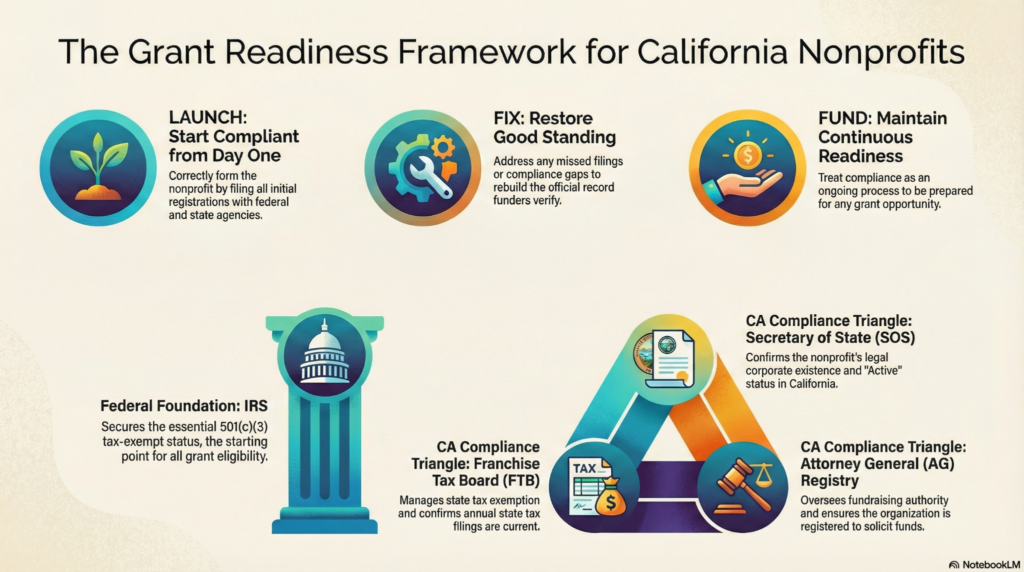

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

The Nonprofit Launch Office operates within a strategic framework designed to help California nonprofits move from formation to fundability:

Launch determines whether first-year grant success is realistic by establishing the timeline for achieving grant-ready status. Organizations that complete incorporation, IRS application, and California registrations efficiently may achieve full compliance by month 6-8 of their first year, leaving 4-6 months for grant pursuit. Organizations that delay formation steps or encounter IRS processing delays may not achieve grant-ready status until year two. Launch planning should include realistic timeline assessment for when grants become strategically worth pursuing versus when focusing on individual donors makes more sense.

Fix becomes relevant even in the first year when formation steps were completed incorrectly or compliance gaps emerge. First-year organizations that incorporated without proper bylaws, missed Attorney General registration requirements, or submitted incomplete IRS applications may need Fix interventions that further delay grant-readiness. Preventing Fix needs through careful Launch execution allows earlier grant pursuit within the first year.

Fund represents the operational state first-year nonprofits are trying to reach—where grant applications become routine rather than extraordinary efforts, where compliance remains current without crisis management, and where the organization can credibly compete for funding. Some first-year organizations achieve Fund status by late in their first year if they launch well. Others don’t reach Fund status until year two or three if launch was messy or resources were limited.

Federal Recognition through IRS 501(c)(3) determination timing critically affects first-year grant feasibility. Organizations that incorporate in January and receive IRS determination by July have five months for grant pursuit in year one. Organizations that incorporate in September and receive determination in March of year two have essentially no first-year grant window. Accelerating federal recognition timelines—through complete, accurate initial applications that avoid IRS delays—expands first-year grant opportunities.

CA Compliance Triangle requires that first-year Riverside nonprofits achieve simultaneous good standing with all three California agencies (Secretary of State, Franchise Tax Board, Attorney General Registry) plus federal IRS recognition before most institutional grants become accessible. The multi-step nature of California compliance—incorporation, then IRS application, then FTB exemption, then AG Registry registration—creates sequential dependencies that extend the timeline to full grant-ready status and affect how much of year one remains available for grant pursuit after compliance is achieved.

Step-by-step: How NPLO helps first-year nonprofits pursue realistic grant opportunities

Step 1: Timeline Reality Assessment We evaluate where you are in your first year and when you’ll realistically achieve full grant-ready status. If you’re month three post-incorporation with IRS application pending, we can project when determination might arrive and how much of year one remains for grant pursuit. This assessment helps set realistic expectations—pursuing grants may not be strategic if you’ll only have 2-3 months of eligible time in year one.

Step 2: Funder Research and Targeting We identify funders who specifically support emerging organizations, capacity building, or new approaches to community problems. Rather than encouraging applications to funders requiring three years of operational history, we focus on the subset of accessible funders whose eligibility criteria align with first-year realities. This targeted approach prevents wasted effort on inappropriate opportunities.

Step 3: Compliance Acceleration We guide rapid completion of any remaining compliance steps—rushing IRS application if not yet filed, completing California registrations immediately upon IRS determination, adopting essential governance policies quickly. Accelerating compliance completion maximizes the portion of year one available for grant pursuit rather than losing months to delayed paperwork.

Step 4: Strengths Documentation Despite Newness We help articulate organizational strengths that compensate for limited history—leadership team credentials and relevant prior experience, community partnerships and stakeholder support letters, needs assessment data justifying program focus, and program design quality showing thoughtful planning. These elements allow applications to compete on potential rather than proven performance.

Step 5: Modest Goal Setting We help set first-year grant targets that reflect emerging organization realities—pursuing 5-10 small grants totaling $25,000-$50,000 rather than attempting one large $100,000 grant requiring extensive track record. Multiple small wins build momentum, provide program funding, and create success stories strengthening year two applications.

Step 6: Individual Donor Integration We develop parallel individual fundraising strategies that don’t depend on institutional grant eligibility, ensuring operating support flows regardless of grant success. First-year organizations shouldn’t depend entirely on grants that may not materialize—individual donors provide more reliable seed funding while you build grant competitiveness.

Step 7: Strategic Timing Planning We coordinate grant application timing with your organizational development timeline. Rather than applying the moment you receive IRS determination, we may recommend waiting 2-3 months to accumulate program data, complete initial board meetings generating governance documentation, and finalize first-quarter financial statements that strengthen applications. Strategic delay sometimes produces better outcomes than rushing premature submissions.

Step 8: Learning and Relationship Building We help view first-year grant pursuit as much about learning funder expectations and building relationships as about winning immediate awards. Some first-year applications result in funding, others result in feedback and invitations to reapply next cycle with stronger applications. Both outcomes advance toward sustainable funding if approached strategically rather than desperately.

Checklist: What first-year nonprofits need to maximize grant competitiveness

First-year Riverside nonprofits pursuing grants should ensure they have:

- Complete federal and state compliance with IRS determination, California SOS Active status, FTB exemption, and AG Registry registration all current

- Governance infrastructure including adopted bylaws, complete board roster, conflict of interest policy, and documented board meetings showing active oversight

- Program documentation with clear descriptions, logic models showing how activities produce outcomes, and preliminary data even if limited

- Financial foundation including operating budget, financial policies, bank account with responsible management, and whatever financial statements your stage allows

- Leadership credentials documented through bios, resumes, or narratives showing relevant expertise and community trust

- Community support evidence through letters from partners, beneficiary testimonials, or needs assessments validating program focus

- Realistic outcome expectations that acknowledge limited history while presenting credible frameworks for measuring future success

- Appropriate funder targets selected for emerging organization focus rather than established performer requirements

- Modest funding requests matching first-year organizational capacity rather than overreaching beyond credible scale

- Clear organizational narrative explaining why you formed, what gap you address, and why community needs justify supporting new approaches

- Professional application materials despite newness—organized, well-written, complete submissions demonstrating competence

- Patience and persistence recognizing that first-year grant success is possible but not guaranteed, and that building momentum takes time

- Parallel funding strategies including individual donors who don’t require institutional eligibility criteria

- Learning orientation that extracts value from application feedback regardless of immediate funding outcomes

- Relationship cultivation with funders you target for year two or three even if year one applications don’t succeed

Quick Answers (PPA)

What’s a realistic grant fundraising goal for a nonprofit’s first year? Realistic first-year grant targets vary widely based on when you achieve compliance, how much time remains for applications, and your specific funding landscape. Conservative planning might target $10,000-$25,000 in first-year grants from multiple small awards, while aggressive strategies in favorable conditions might pursue $50,000-$75,000. However, many successful nonprofits raise little to no grant funding in year one because they spend most of the year completing formation and building foundations, achieving grant-ready status too late for substantial pursuit. Setting expectations around building grant capacity in year one rather than depending on grants for survival prevents crisis when grants don’t materialize as quickly as hoped.

Should I wait until year two to pursue grants so I have more history, or start immediately when eligible? This depends on your specific timeline and capacity. If you achieve full compliance in month 6-7 of your first year, pursuing grants in months 8-12 makes strategic sense—you’re building experience, developing applications, establishing funder relationships, and possibly winning modest awards. If you don’t achieve compliance until month 10-11, investing time in grant applications with only 1-2 months remaining may not be strategic—focusing on individual donors and preparing for aggressive year two grant pursuit might produce better results. The key is assessing whether you have sufficient time and organizational readiness to make first-year grant pursuit worthwhile rather than defaulting to “apply immediately” regardless of circumstances.

Do funders explicitly say they accept first-year nonprofits, or do I need to read between the lines? Some funders explicitly state eligibility for “emerging organizations,” “capacity building,” or “organizations in their first three years,” making first-year eligibility clear. Other funders have eligibility criteria that don’t explicitly exclude new organizations but also don’t encourage them—requiring “demonstrated track record” or “evidence of programmatic success” suggests preference for established organizations but doesn’t absolutely bar first-year applicants with strong cases. When eligibility is ambiguous, contacting program officers directly to ask about first-year applicant viability prevents wasting time on inappropriate opportunities. Many program officers appreciate the outreach and provide honest guidance about whether application makes sense.

What if I have relevant experience from previous organizations—does that count as organizational history? Individual team member experience absolutely strengthens first-year applications even though the organization itself lacks history. Applications should prominently feature leadership bios highlighting relevant credentials, prior program management experience, subject matter expertise, and community trust built through previous work. However, be clear about the distinction—”Our Executive Director has ten years of youth development experience, though our organization formed six months ago” presents leadership strength honestly without misrepresenting organizational age. Some funders value experienced leadership enough that it compensates for organizational newness. Others maintain organizational history requirements regardless of individual credentials.

Are there advantages to being a new nonprofit when seeking grants? Yes, strategically positioned. Some funders specifically seek innovative approaches and emerging solutions rather than established programs, viewing new organizations as sources of fresh thinking and adaptive programming. New organizations can sometimes move faster and experiment more readily than established nonprofits with bureaucratic constraints. First-year status can also generate community excitement and volunteer engagement that demonstrates grassroots support to funders. Finally, some funders set aside resources specifically for capacity building and organizational development available only to emerging organizations, creating funding opportunities established nonprofits can’t access. The key is targeting funders who value these newness advantages rather than viewing all funders through the same lens.

What to do next (DIY vs Done-With-You)

DIY approach: Conduct honest assessment of where you are in year one—have you completed IRS determination, California registrations, governance adoption, and initial program operations? Calculate how many months remain in year one after achieving full compliance, recognizing you need at least 3-4 months of eligible time to make grant pursuit worthwhile. Research funders explicitly supporting emerging organizations by searching “grants for new nonprofits California,” “capacity building grants Inland Empire,” and reviewing community foundation websites for programs targeting first-year organizations. Review eligibility criteria carefully rather than applying broadly—does “demonstrated track record” mean you’re excluded, or can strong leadership credentials substitute? Develop modest first-year grant targets focused on multiple small awards rather than few large ones. Create parallel individual donor strategies ensuring operating support regardless of grant outcomes. View first-year grant pursuit as learning and relationship building as much as immediate fundraising—feedback and invitations to reapply create year two advantages even when year one applications don’t yield awards.

Done-With-You approach: The Nonprofit Launch Office provides realistic first-year grant strategy for Riverside and Inland Empire nonprofits balancing optimism with honest assessment. We evaluate your specific timeline and readiness to determine whether grant pursuit makes strategic sense in year one or whether building foundations for year two produces better outcomes, research and identify funders whose eligibility criteria and mission focus align with first-year organizational realities, accelerate any remaining compliance steps to maximize time available for grant pursuit within year one, help document organizational strengths that compensate for limited history—leadership credentials, community partnerships, needs justification, program design quality, develop appropriately modest grant targets matching first-year capacity and funder accessibility, create integrated fundraising strategies combining realistic grant goals with individual donor cultivation, provide application development support emphasizing potential and planning over proven performance, and position first-year efforts as foundation building for sustained grant success in years two and beyond. This guidance prevents unrealistic expectations that create financial crisis when grants don’t materialize while maximizing whatever first-year grant opportunities genuinely exist.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Sources

- IRS – Charitable Organizations Overview

- IRS Tax Exempt Organization Search (EO Finder)

- California Secretary of State – Business & Nonprofit Entities

- California Franchise Tax Board – Nonprofit Tax Information

- California Attorney General – Registry of Charitable Trusts

- CalNonprofits – Resources for California Nonprofits

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.