26 Jan What Policies Should a New Nonprofit Have from Day One?

Short Answer

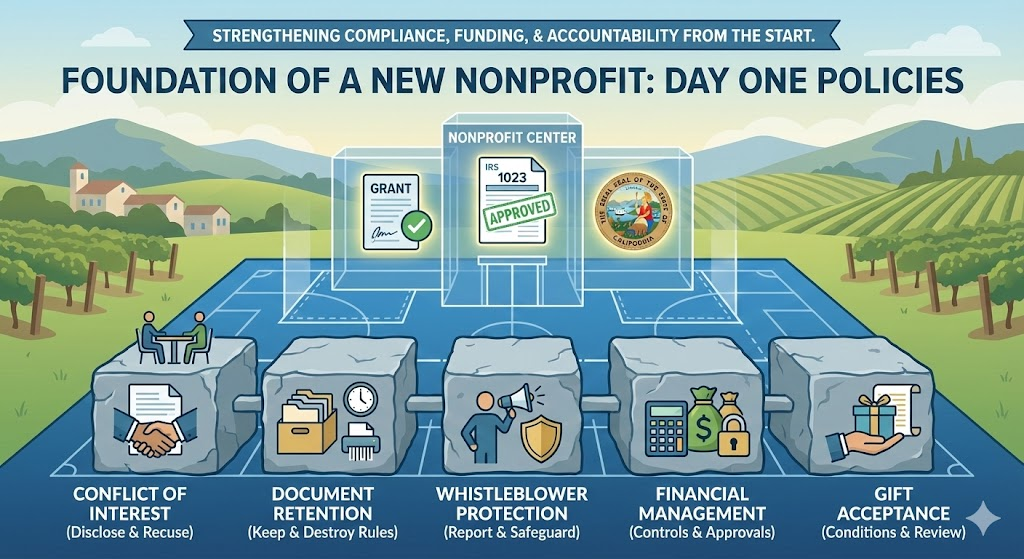

New nonprofits should establish from day one a conflict of interest policy requiring annual disclosure and recusal procedures, a document retention and destruction policy specifying what records to keep and for how long, a whistleblower policy protecting individuals who report suspected violations or misconduct, financial management policies addressing approval authorities and internal controls, and a gift acceptance policy clarifying what donations the organization will accept and under what conditions. Eligibility varies by organization, but these core policies matter because the IRS Form 1023 application specifically asks about conflict of interest and whistleblower policies, funders commonly request governance policies when evaluating grant applications, proper policies prevent compliance problems and operational confusion, and California Attorney General monitors nonprofit governance practices including policy adoption. Temecula and Inland Empire nonprofits that establish these foundational policies during formation demonstrate organizational maturity and governance quality that strengthen IRS determination applications, improve grant competitiveness, and create accountability frameworks preventing the governance problems that plague nonprofits lacking clear operational guidelines.

What are the essential policies IRS and funders expect to see?

Conflict of interest policy represents the single most critical governance policy for new nonprofits because IRS Form 1023 applications specifically ask whether the organization has adopted a conflict of interest policy, and because conflict management demonstrates the board exercises genuine oversight rather than rubber-stamping founder decisions. Effective conflict policies require annual written disclosure statements from all board members, officers, and key employees identifying potential conflicts (business relationships, family connections, financial interests in vendors or partners), establish procedures for board members to identify conflicts as they arise in specific decisions, prohibit interested parties from voting on matters where they have conflicts, and require that a majority of board members and all committee members reviewing conflicted transactions be free from conflicts themselves. The policy should define what constitutes a conflict broadly—not just direct financial benefit but also indirect benefits through family members or business associates.

Whistleblower policy (sometimes called whistleblower protection policy) provides procedures for employees, volunteers, and board members to report suspected legal violations, financial improprieties, or policy breaches without fear of retaliation. The IRS Form 1023 asks about whistleblower policies, and the Sarbanes-Oxley Act requires certain protections even for nonprofits. Effective whistleblower policies establish multiple reporting channels (supervisor, board chair, legal counsel, outside hotline), prohibit retaliation against individuals who report concerns in good faith, outline investigation procedures when reports are received, and maintain confidentiality to the extent possible. Whistleblower policies matter because they create accountability mechanisms encouraging early problem identification and demonstrate commitment to ethical operations.

Document retention and destruction policy specifies what organizational records must be maintained, for how long, under what conditions, and when/how they can be destroyed. The Sarbanes-Oxley Act requires nonprofits to retain certain financial and governance documents, and various state and federal laws impose retention requirements. Effective policies identify document categories (incorporation documents, IRS determination letters, tax returns, financial records, board minutes, employee files, donor records, grant agreements, contracts) with specific retention periods for each category, establish secure storage procedures, and create destruction protocols ensuring documents are destroyed systematically when retention periods expire rather than selectively destroyed when convenient. Document retention policies prevent both accidental loss of critical records and intentional destruction of documents relevant to investigations.

Financial management policies establish internal controls preventing fraud, misappropriation, or financial mismanagement. While comprehensive financial policies evolve as organizations mature, day-one policies should address: who has authority to approve expenses and at what dollar thresholds, how many signatures are required on checks or electronic fund transfers, how cash receipts are handled and deposited, what documentation is required for expense reimbursement, how credit cards or debit cards are controlled, and how financial reports are reviewed by board or finance committee. Financial policies demonstrate fiscal responsibility to funders and provide accountability frameworks preventing the common nonprofit problem where founders have unchecked access to organizational funds.

What additional policies strengthen governance and operations?

Gift acceptance policy clarifies what types of donations the organization will accept, under what conditions, and what donations will be declined or require special board approval. Basic gift acceptance policies address: cash and check donations (almost always accepted), stock or securities (accepted if readily marketable), real estate (requires appraisal and board approval due to liability and maintenance concerns), vehicles or equipment (evaluated for usefulness versus disposal costs), in-kind goods or services (accepted if needed for programs, declined if storage/disposal is burdensome), and restricted gifts (accepted only if restrictions align with organizational mission and capacity). Gift acceptance policies prevent problems where well-meaning donors offer gifts that create financial burden, liability exposure, or mission drift through restrictive conditions the organization cannot reasonably satisfy.

Records access policy (sometimes called transparency policy) establishes what organizational documents are available to the public, board members, donors, or regulatory agencies, and through what procedures access is provided. California law and IRS regulations require certain documents be made available—Form 990 returns, IRS determination letter, and (for California nonprofits) Articles of Incorporation and bylaws to Attorney General upon request. Policies should specify: what documents are public versus confidential, how requests for documents are handled and by whom, whether fees are charged for copying, and what timeframes apply for providing requested documents. Clear access policies prevent confusion when stakeholders or journalists request organizational information.

Expense reimbursement and travel policy establishes what organizational expenses will be reimbursed to board members, employees, or volunteers, what documentation is required, and what approval is necessary. Policies typically address: mileage reimbursement rates (often tied to IRS standard rates), meal and lodging expense limits, what receipts are required for reimbursement, how quickly reimbursement requests must be submitted, and who approves reimbursements. Clear expense policies prevent disputes about what’s reimbursable and ensure consistent treatment of similar expenses rather than ad hoc decisions that may appear to favor certain individuals.

Volunteer management policy (particularly important for volunteer-dependent organizations) addresses volunteer recruitment, screening, training, supervision, and recognition procedures. Policies might cover: background check requirements for volunteers working with vulnerable populations, confidentiality obligations for volunteers accessing sensitive information, volunteer rights and responsibilities, grievance procedures if problems arise, and risk management procedures ensuring adequate insurance coverage for volunteer activities. Volunteer policies demonstrate professionalism in volunteer engagement and reduce liability exposure from inadequately supervised volunteers.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

The Nonprofit Launch Office operates within a strategic framework designed to help California nonprofits move from formation to fundability:

Launch includes adopting core governance policies during the organizational meeting when the board adopts bylaws and makes initial operational decisions. Launch-phase policy adoption demonstrates to IRS reviewers evaluating Form 1023 applications that governance structures are functional rather than theoretical, shows funders that organizational management follows professional standards, and creates accountability frameworks from inception rather than attempting to impose policies retroactively after problems emerge. Organizations that launch with strong policies avoid many Fix interventions later.

Fix addresses situations where policies were never adopted during Launch, creating problems when IRS or funders request policies the organization doesn’t have, when conflicts arise without clear procedures for managing them, or when financial irregularities occur because no internal controls existed. Fix work involves developing and adopting policies that should have existed from day one, potentially explaining to IRS or funders why policies are being adopted retroactively, and implementing practices that align with newly adopted policies rather than continuing previous informal operations.

Fund depends partly on policy quality because grant applications frequently request governance policies as part of due diligence documentation. Funders review conflict of interest policies to assess whether the board prevents self-dealing, examine financial policies to evaluate internal controls protecting grant funds, and consider whether whistleblower policies suggest commitment to accountability. Missing policies weaken grant applications by suggesting poor governance; strong policies strengthen applications by demonstrating organizational maturity.

Federal Recognition through IRS 501(c)(3) determination applications includes specific Form 1023 questions about conflict of interest policies and whistleblower policies. Organizations answer “no” to having these policies face IRS questions requiring explanation, while organizations with adopted policies can attach them to applications demonstrating governance quality. The IRS views policy adoption as evidence of functional board oversight rather than founder-dominated structures lacking genuine governance.

CA Compliance Triangle (Secretary of State, Franchise Tax Board, Attorney General Registry) includes Attorney General oversight of nonprofit governance practices. The Attorney General can request policies during investigations, reviews Form 990 Schedule O narratives describing governance policies, and monitors for governance failures suggesting policy gaps. California nonprofits should maintain policies accessible for Attorney General review if requested.

Step-by-step: How NPLO helps new nonprofits establish foundational policies

Step 1: Essential Policy Identification We assess which policies your organization needs immediately versus which can be developed as operations mature. All organizations need conflict of interest, whistleblower, and document retention policies from day one. Additional policies depend on organizational characteristics—gift acceptance matters more for fundraising-focused organizations, volunteer management matters more for volunteer-dependent operations, financial controls scale with budget size.

Step 2: Template Customization We provide model policy templates appropriate for California nonprofits and customize them to organizational needs. Generic national templates often don’t reflect California requirements or fit small nonprofit realities. We adapt templates to match actual governance structures, operational models, and organizational capacity rather than imposing complex policies designed for large organizations on small startups.

Step 3: Board Education We help boards understand what policies mean and why they matter, not just adopt boilerplate language they don’t comprehend. Board members should understand conflict of interest procedures so they recognize conflicts when they arise, understand whistleblower protections so they don’t inadvertently retaliate, and understand document retention so they don’t destroy critical records. Education transforms policies from paperwork into functional governance tools.

Step 4: Formal Adoption Process We guide proper policy adoption during board meetings with documented votes, ensuring adoption is recorded in meeting minutes with dates and approval votes, and that adopted policies are maintained in organizational records where board members can access them. Formal adoption creates the documentation trail proving policies exist and were deliberately approved rather than casually accepted.

Step 5: Annual Disclosure Implementation For conflict of interest policies, we help implement annual disclosure processes where all board members, officers, and key staff complete written disclosure forms identifying potential conflicts, forms are collected and reviewed by board or governance committee, and disclosures are updated when circumstances change. Annual disclosure operationalizes conflict policies beyond abstract adoption.

Step 6: Policy Communication We ensure policies are communicated to everyone they affect—board members receive governance policies, employees receive personnel and financial policies, volunteers receive volunteer management policies, donors receive gift acceptance policies. Communication ensures individuals understand expectations and procedures rather than discovering policy requirements during conflicts or problems.

Step 7: Form 1023 Integration We prepare policy documentation for IRS Form 1023 applications, ensuring conflict of interest and whistleblower policies are attached as required exhibits, policy adoption is documented in board minutes referenced in applications, and application narratives describe how policies are implemented in practice. Strong policy documentation strengthens IRS applications significantly.

Step 8: Ongoing Review and Updates We establish schedules for reviewing policies periodically (typically every 2-3 years), updating policies when legal requirements change or organizational growth makes existing policies insufficient, and documenting policy amendments in board minutes. Policies should evolve with organizational maturation rather than remaining static documents that become obsolete.

Checklist: What policies your new Riverside nonprofit should adopt

New nonprofits should establish these foundational policies from day one:

- Conflict of interest policy requiring annual written disclosures, recusal from conflicted decisions, prohibition on interested party voting, and independent review of conflicted transactions

- Whistleblower policy providing reporting channels, retaliation prohibitions, investigation procedures, and confidentiality protections

- Document retention and destruction policy specifying retention periods for different document types, storage procedures, and systematic destruction protocols

- Financial management policy addressing approval authorities, signature requirements, cash handling, expense documentation, and financial reporting

- Gift acceptance policy clarifying what donations are accepted, what requires special approval, and what is declined due to liability or mission concerns

Additional policies to consider based on organizational needs:

- Records access policy establishing what documents are public, confidential, or available to specific stakeholders

- Expense reimbursement policy specifying what’s reimbursable, documentation requirements, and approval procedures

- Volunteer management policy (if volunteer-dependent) addressing recruitment, screening, training, supervision, and recognition

- Social media policy (if using social platforms) clarifying who can post on behalf of organization and what content is appropriate

- Data privacy policy (if collecting personal information) explaining how data is collected, used, stored, and protected

- Code of ethics articulating values and behavioral expectations for board, staff, and volunteers

Quick Answers (PPA)

Can we adopt policies later as we grow, or do we really need them from day one? While comprehensive policy manuals evolve as organizations mature, certain core policies—conflict of interest, whistleblower, document retention, basic financial controls—should be adopted during the organizational meeting for several reasons. First, IRS Form 1023 asks specifically about conflict and whistleblower policies, so you need them for determination applications. Second, early policy adoption establishes governance expectations and accountability frameworks before problems occur—adopting conflict policies after a conflict emerges appears reactive rather than proactive. Third, funders reviewing grant applications within your first year expect to see basic governance policies. Fourth, operating without policies creates risks—financial mismanagement without controls, lost records without retention policies, or mishandled conflicts without procedures. Starting with foundational policies and expanding policy coverage as you grow is far better than operating policy-free during startup.

Do policies need to be long, complex documents, or can they be relatively simple for a small nonprofit? Policy complexity should match organizational size and complexity. A small all-volunteer organization with a $25,000 budget needs simpler, shorter policies than a $2 million organization with staff, multiple programs, and complex operations. Effective policies for small nonprofits might be 1-3 pages each covering essential elements clearly and concisely. Avoid adopting 30-page policy manuals designed for large nonprofits when your reality is five board members meeting quarterly. Simple, clear policies that your board actually understands and follows are far better than comprehensive complex policies that sit on shelves ignored. You can always expand and elaborate policies as organizational sophistication grows—start appropriately simple.

What happens if we adopt policies but don’t actually follow them—is that worse than not having policies? Yes, adopting policies you don’t follow creates worse problems than not having formal policies. When policies exist but aren’t followed, it demonstrates either board incompetence (adopted policies without understanding them) or deliberate disregard for governance (knew policies existed but chose to ignore them). IRS reviews, funder due diligence, or legal disputes will reveal the gap between stated policies and actual practices, seriously damaging organizational credibility. The solution is adopting realistic policies you can and will follow—if quarterly financial reporting to the board is unrealistic for your capacity, don’t adopt a policy requiring it. Better to have fewer, simpler policies that are actually implemented than comprehensive policies that exist only on paper.

Who is responsible for ensuring policies are followed—the board, executive director, or someone else? Responsibility varies by policy type. The board is responsible for ensuring governance policies (conflict of interest, whistleblower, document retention for governance records) are followed and for monitoring that management follows operational policies. The executive director or organizational leadership is responsible for implementing operational policies (financial controls, expense reimbursement, volunteer management) on a day-to-day basis and reporting to the board about policy compliance. For small nonprofits without staff, the board collectively manages both governance and operational policy implementation. Many organizations assign a compliance officer or designate specific board members (treasurer for financial policies, secretary for document retention) to monitor particular policy areas. Clear assignment of policy monitoring responsibility prevents the common problem where everyone assumes someone else is ensuring compliance.

Should policies be publicly available, or can we keep them internal and confidential? Some policies should be publicly available while others can remain internal. Conflict of interest policies, whistleblower policies, and gift acceptance policies are often published on websites demonstrating transparency and governance quality. Financial management policies and document retention policies are typically internal documents available to board and staff but not necessarily published. The key is that policies must be available when legitimately requested—IRS Form 1023 applications require submitting certain policies, funders commonly request governance policies during due diligence, and California Attorney General can request policies during investigations. Being prepared to share policies when appropriately requested is more important than deciding whether to proactively publish them. Organizations demonstrating nothing to hide often publish core governance policies voluntarily.

What to do next (DIY vs Done-With-You)

DIY approach: Start by downloading model policy templates from reputable sources like CalNonprofits.org, National Council of Nonprofits, or BoardSource for conflict of interest, whistleblower, and document retention policies. Review templates carefully, customizing language to match your organizational structure, size, and operations rather than adopting generic language unchanged. Ensure California-specific requirements are addressed. Schedule a board meeting specifically to review, discuss, and adopt policies—don’t just email policies asking for approval, have genuine board discussion about what policies mean and how they’ll be implemented. Document policy adoption in meeting minutes with vote tallies and dates. Create annual disclosure forms for conflict of interest policy and collect initial disclosures from all board members. Maintain adopted policies in organizational records where board members can access them and where they’re available for IRS applications and funder requests. Establish calendar reminders to review and collect annual conflict disclosures each year. Plan to expand policy coverage as the organization matures—add gift acceptance when you begin active fundraising, add volunteer management when volunteer engagement grows, add personnel policies when you hire staff.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive policy development for Riverside and Inland Empire nonprofits, ensuring foundational governance structures are established from day one. We assess which policies your organization needs immediately based on size, structure, and operational model, provide California-compliant model policies customized to your specific organizational characteristics, educate boards about policy meaning and implementation so policies become functional governance tools rather than ignored paperwork, guide formal adoption processes during board meetings with proper documentation in minutes, implement annual conflict disclosure procedures operationalizing conflict policies beyond abstract adoption, prepare policy documentation for IRS Form 1023 applications with appropriate exhibits and narratives, ensure policies are communicated to everyone they affect—board members, staff, volunteers, donors, and establish review schedules maintaining policy relevance as organizations evolve. This comprehensive approach delivers professionally drafted, legally compliant, operationally appropriate policies that strengthen IRS applications, improve grant competitiveness, create accountability frameworks, and demonstrate organizational maturity from inception.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Sources

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.