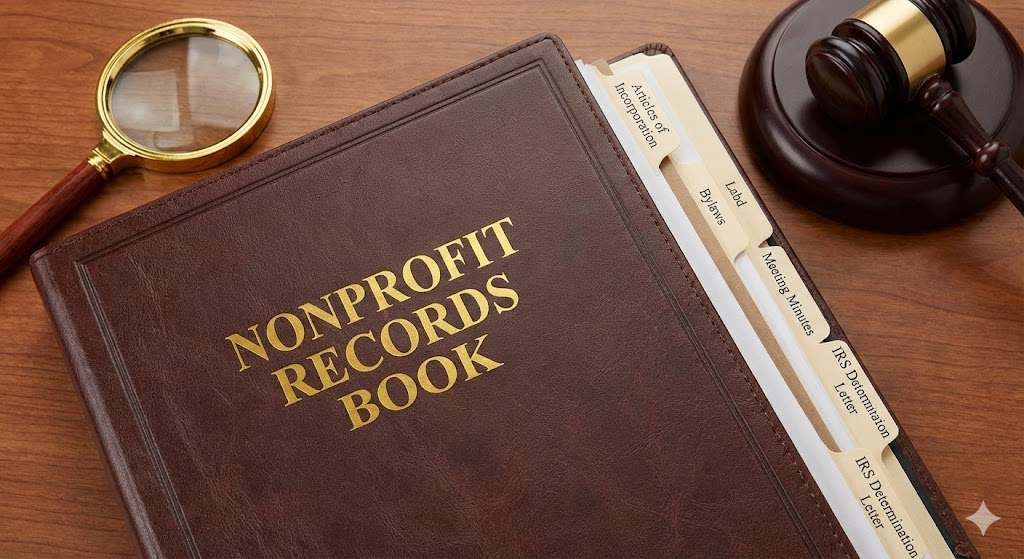

26 Jan What Is a Nonprofit “Records Book” and What Should It Contain?

Short Answer

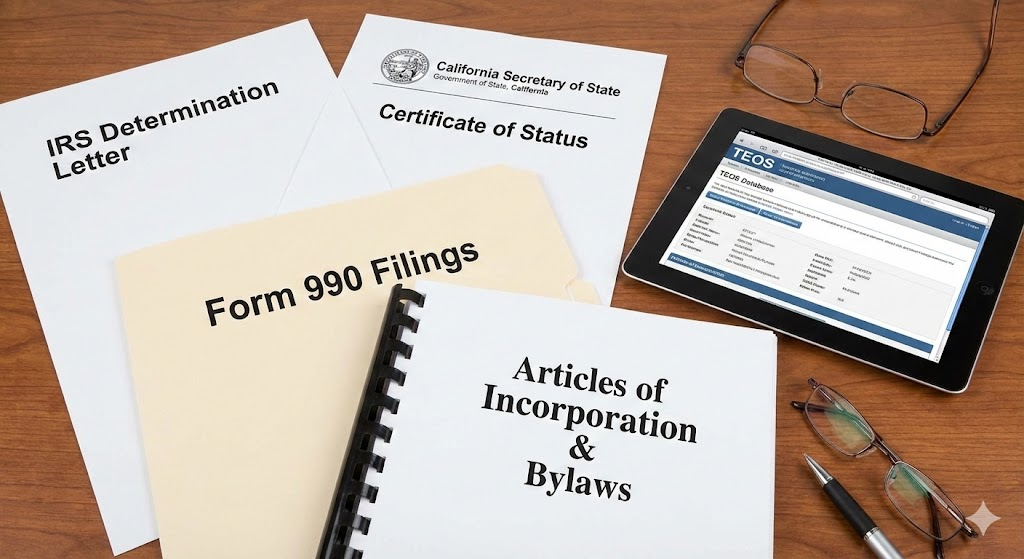

A nonprofit records book (also called a corporate records book or minute book) is the organized collection of essential organizational documents including formation documents, governance records, meeting minutes, resolutions, and compliance filings maintained in one accessible location. It should contain Articles of Incorporation, IRS determination letter, bylaws, board meeting minutes, annual reports, key policies, and other critical documents. The records book matters because California law requires nonprofits to maintain corporate records accessible for inspection, IRS and funders commonly request documents contained in the records book, and organized record-keeping prevents the crisis where critical documents can’t be located when urgently needed.

What documents belong in the nonprofit records book?

Formation documents establish legal existence and organizational structure. The records book should contain filed Articles of Incorporation showing Secretary of State filing stamp, original or certified copy of IRS determination letter confirming 501(c)(3) status, current bylaws as adopted and amended, and initial organizational meeting minutes documenting bylaw adoption, officer election, and policy approval. These foundational documents prove the organization was properly formed and operates under defined governance structures.

Meeting minutes and resolutions document ongoing governance activity. Include all board meeting minutes chronologically, committee meeting minutes if committees have decision-making authority, annual meeting minutes if membership structure exists, and board resolutions authorizing specific actions like bank account opening, contract signing authority, or major transactions. Complete minute records prove the board exercises genuine oversight rather than existing only on paper.

Policies and governance documents demonstrate operational frameworks. The records book should contain conflict of interest policy with annual disclosure forms, whistleblower policy, document retention and destruction policy, financial management policies, gift acceptance policy, and other adopted policies governing organizational operations. These policies show how the organization implements governance principles and manages operational risks.

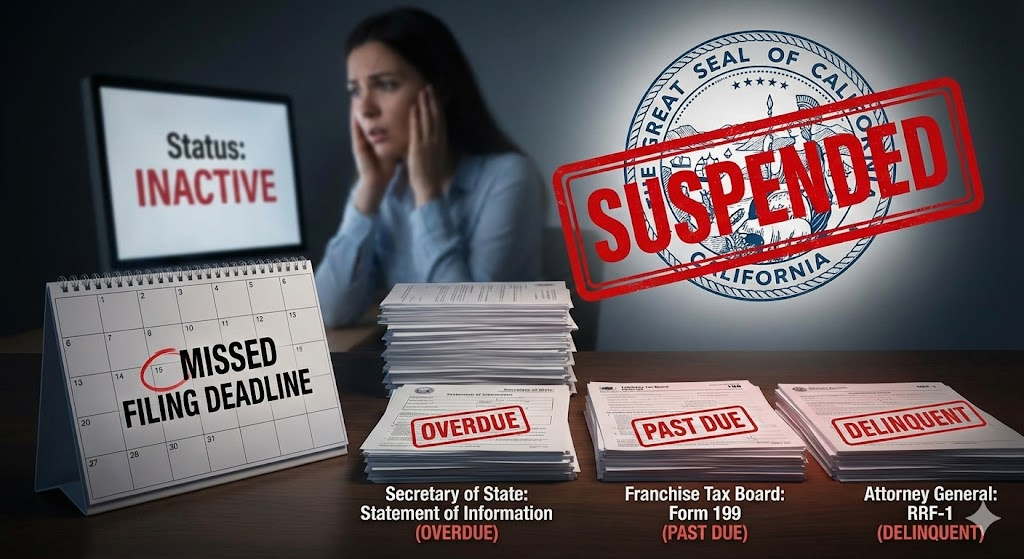

Compliance and registration documents prove ongoing legal standing. Include California Statement of Information filings, Franchise Tax Board correspondence confirming tax exemption, Attorney General Registry of Charities registration and renewal confirmations, annual Form 990 and Form 199 returns, and current certificates of insurance. These documents demonstrate compliance with federal and California requirements funders verify during due diligence.

How should records be organized and who can access them?

Physical organization traditionally uses three-ring binders with tabbed sections separating document categories. Many San Bernardino nonprofits maintain multiple binders—one for formation and governance (Articles, bylaws, policies), another for meeting minutes chronologically, and a third for annual compliance filings. Tabs should clearly label sections, documents should be arranged chronologically within sections, and the organization should maintain a table of contents or index showing what’s included.

Digital organization increasingly supplements or replaces physical records books. Scan critical documents to PDF format maintaining quality for legibility, organize files in clearly labeled folders matching physical binder structure, maintain cloud storage with regular backups, and implement access controls ensuring appropriate people can retrieve documents while maintaining security. Hybrid approaches maintaining both physical signed originals and digital copies for convenience work well for many organizations.

Access requirements under California law mandate that directors have right to inspect corporate records. The organization should maintain records at its principal office or make them available electronically to board members upon request. California Attorney General can request inspection of charitable corporation records during investigations. Certain documents like bylaws and conflict of interest policies may be requested by IRS or funders. Clear procedures for record access prevent disputes while maintaining appropriate confidentiality.

Responsibility assignment ensures someone maintains the records book. The corporate secretary typically holds primary responsibility for maintaining accurate, current records and ensuring meeting minutes get added promptly. However, small nonprofits without staff often assign treasurer or executive director to maintain the physical or digital files. Clear assignment prevents the common problem where everyone assumes someone else maintains records and critical documents get lost.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

Launch includes establishing the records book immediately after incorporation. New San Bernardino nonprofits should create organized filing systems from day one, adding formation documents as they’re received and minutes as meetings occur.

Fix addresses organizations with missing, disorganized, or incomplete records requiring systematic reconstruction and organization. Retroactively organizing scattered documents and identifying gaps allows developing complete records going forward.

Fund depends on organized records because grant applications request multiple documents with tight deadlines. Having everything organized in accessible records books prevents scrambling or missing opportunities because critical documents can’t be located.

Federal Recognition applications require submitting multiple documents that should be maintained in records books. IRS Form 1023 requests Articles, bylaws, minutes, and other documents. Well-maintained records books make application preparation straightforward.

CA Compliance Triangle documentation belongs in records books. Secretary of State status certificates, Franchise Tax Board exemption verifications, and Attorney General Registry confirmations should all be maintained in organized compliance sections.

Step-by-step: How NPLO helps organizations establish records books

Step 1: Document Inventory We identify what documents you currently have and what’s missing.

Step 2: Organization Structure Design We create logical section organization matching your operational needs.

Step 3: Missing Document Acquisition We help obtain duplicates of lost critical documents.

Step 4: Physical Book Assembly We set up physical binders with tabs and organized document placement.

Step 5: Digital Archive Creation We scan documents creating secure digital archives with backup.

Step 6: Index Development We create tables of contents showing what’s included and where.

Step 7: Maintenance Procedures We establish systems for adding new documents promptly.

Step 8: Access Protocols We implement procedures for board member access and security.

Checklist: Essential records book contents

Formation Section:

- Articles of Incorporation (filed with SOS stamp)

- IRS determination letter

- Current bylaws

- Organizational meeting minutes

Governance Section:

- Conflict of interest policy

- Annual conflict disclosure forms

- Whistleblower policy

- Document retention policy

- Other adopted policies

Minutes Section:

- All board meeting minutes (chronological)

- Committee minutes (if applicable)

- Annual meeting minutes (if applicable)

Resolutions Section:

- Bank account authorization

- Signing authority designations

- Major transaction approvals

Compliance Section:

- Statement of Information filings

- FTB exemption correspondence

- AG Registry confirmations

- Form 990 returns (recent years)

- Form 199 returns

- Insurance certificates

Financial Section:

- Current year budget

- Recent financial statements

- Audit reports (if applicable)

Quick Answers (PPA)

Can records be kept entirely electronically, or must we maintain physical copies? California law doesn’t mandate physical records books—electronic records are acceptable if properly maintained with security and backups. Many organizations maintain hybrid systems keeping physical signed originals in binders while also maintaining digital scans for easy sharing. The key is ensuring records are preserved, organized, accessible to those with legitimate need, and protected from loss. Whatever system you choose, maintain it consistently and ensure directors know how to access documents.

Who is allowed to look at the records book—can anyone request access? California law gives directors absolute right to inspect corporate records. The organization must make records available to directors at reasonable times and locations. Other parties have more limited access rights—California Attorney General can inspect charitable corporation records during investigations, IRS can request documents during audits or reviews, funders can request specific documents during grant applications, and some documents like Form 990 are publicly available regardless. The organization can maintain appropriate confidentiality for sensitive documents while meeting legal access obligations.

What should we do if our organization has no records book and we don’t know where critical documents are? Start by systematically searching for whatever documents exist—check email archives, old board members’ files, accountant or attorney files, cloud storage accounts, and organizational file cabinets. Obtain duplicates of critical missing documents—request duplicate IRS determination letter, download filed Articles of Incorporation from Secretary of State website, and request copies of Form 990s from IRS or download from GuideStar. Then create organized records book going forward, adding retroactively located documents and maintaining new documents as they’re created. Better to start organizing now than continue operating without accessible records.

How long must we keep documents in the records book—can old ones eventually be removed? Formation documents, bylaws, minutes, and resolutions should be maintained permanently—they’re the historical governance record. Compliance filings generally should be retained for significant periods—IRS recommends keeping Form 990s for seven years minimum, though many organizations keep them permanently. Financial records typically require seven-year retention. Document retention policy should specify retention periods for different document types. However, records books usually aren’t space-limited—adding sections or new binders as documents accumulate is straightforward, making permanent retention of most governance documents practical.

Should the records book stay at one person’s home or office, or should it be at the nonprofit’s office location? If the organization has a physical office, records should be maintained there for accessibility. If no office exists, records typically stay with whoever is responsible for maintenance—usually the secretary, treasurer, or executive director. California law requires making records available at the principal office address or electronically to directors. The key is that responsible parties know where records are located, multiple people know how to access them if the primary person is unavailable, and backup copies exist in case originals are lost. Digital records solve many location problems since multiple authorized people can access cloud storage.

What to do next (DIY vs Done-With-You)

DIY approach: Purchase three-ring binders and tab dividers from office supply store. Create sections: Formation, Governance/Policies, Minutes, Resolutions, Compliance, Financial. Gather all organizational documents you can locate—Articles, determination letter, bylaws, minutes, policies, compliance filings. Organize documents chronologically within each section. Create simple table of contents listing what’s in each section. Identify missing critical documents and obtain replacements—request duplicate determination letter from IRS, download filed Articles from Secretary of State website. Scan organized documents to PDF creating digital backup stored in secure cloud location. Assign clear responsibility for maintaining records book and adding new documents promptly—meeting minutes after each meeting, compliance filings when submitted, new policies when adopted. Establish procedure for board members to access records when needed. Review and update records book quarterly ensuring it remains current and complete.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive records book establishment for San Bernardino and Inland Empire nonprofits. We inventory existing documents and identify gaps requiring attention, design logical organization structures matching operational needs, help obtain replacement documents for critical missing items, assemble physical binders with professional organization and labeling, create secure digital archives with backup systems, develop comprehensive indexes showing contents and locations, implement maintenance procedures ensuring new documents get added promptly, establish access protocols balancing director rights with appropriate security, and provide ongoing support updating records as organizations evolve. This ensures you maintain the organized, complete, accessible records that satisfy California law, IRS requirements, and funder expectations while preventing the governance crises that emerge when critical documents can’t be located.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Sources

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.