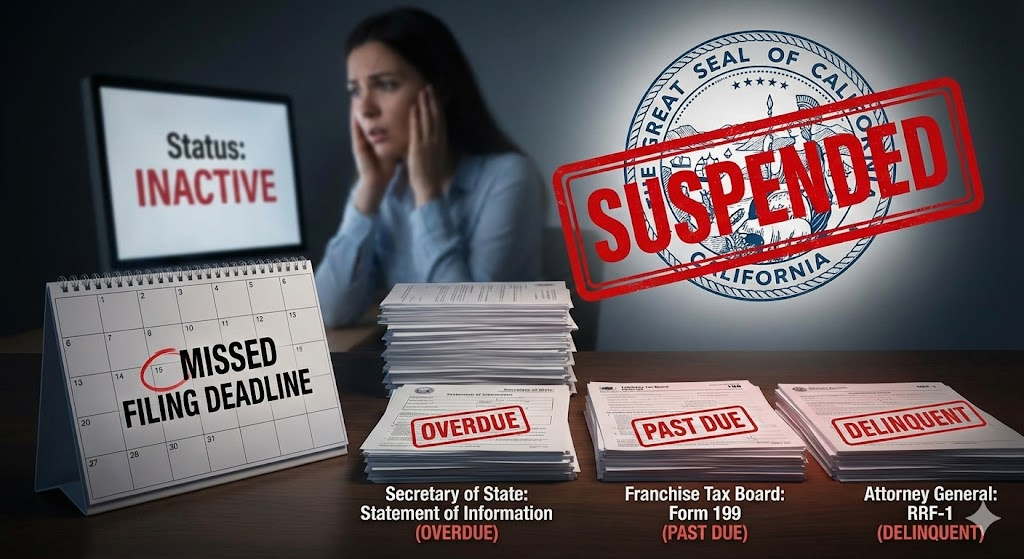

26 Jan What Happens If a Nonprofit Forgets a Recurring State Filing?

Short Answer

Missing recurring California state filings triggers progressive consequences depending on which filing was missed and for how long—California Secretary of State suspension for missed Statement of Information filings prevents the organization from legally conducting business or entering contracts, Franchise Tax Board suspension for missed Form 199 filings blocks state tax-exempt status and can trigger penalties, and Attorney General Registry delinquency for missed RRF-1 renewals technically prohibits charitable solicitation and fundraising until registration is current. These consequences matter for nonprofits because suspended or delinquent status discovered during grant due diligence typically results in immediate application rejection regardless of program quality, banking relationships may be affected when financial institutions verify organizational standing, the organization cannot enter legally enforceable contracts including grant agreements while suspended, and restoration requires filing all delinquent returns plus paying penalties and reinstatement fees. Eligibility varies by filing type, but Temecula and Inland Empire nonprofits can restore good standing through systematic remediation filing overdue returns and paying associated costs, though prevention through compliance calendars and deadline tracking proves far less expensive and disruptive than after-the-fact restoration efforts.

What specific consequences follow from each type of missed California filing?

Secretary of State Statement of Information filing lapses create corporate status problems when the biennial filing (due every two years during the organization’s designated filing month) isn’t submitted by the deadline. California nonprofit corporations must file Statement of Information updating the organization’s registered agent, principal office address, and current directors. Missing this filing initially doesn’t trigger immediate consequences—California provides grace periods before taking action. However, continued non-filing eventually results in Secretary of State changing corporate status from “Active” to “Suspended” or in severe cases “Forfeited.” Suspended status means the organization cannot legally conduct business in California, cannot enter enforceable contracts (including grant agreements), and technically should cease operations until status is restored through filing overdue Statement of Information and paying reinstatement fees.

Franchise Tax Board Form 199 or Form 199N filing lapses create state tax exemption problems when the annual California return isn’t filed by the deadline (typically the 15th day of the 5th month after fiscal year end, same as federal Form 990 deadline). The FTB requires tax-exempt nonprofits to file annually even though they owe no taxes—the filing maintains state tax-exempt status and demonstrates continued eligibility. Missing Form 199 filings triggers FTB suspension of tax-exempt status after appropriate notice periods. FTB suspension means the organization loses California state tax exemption (though federal IRS recognition remains unaffected), the organization is assessed minimum franchise tax ($800 annually) which accrues until resolved, penalties and interest accumulate on unpaid taxes, and the organization shows “Suspended” status in FTB lookups that funders commonly check during due diligence.

Attorney General Registry of Charities RRF-1 renewal filing lapses create fundraising registration problems when the annual renewal isn’t submitted by the deadline (within 4 months and 15 days after fiscal year end, matching Form 990 deadline). Most California nonprofits must register with Attorney General Registry and file annual RRF-1 renewals to maintain legal authority to solicit charitable donations in California. Missing RRF-1 renewals changes Registry status from “Current” to “Delinquent.” Delinquent status means the organization is technically operating without proper fundraising authorization, is violating California charitable solicitation law if continuing to fundraise, may face Attorney General investigation or enforcement action, and cannot demonstrate current registration to funders who verify Registry status during grant due diligence.

Combined filing failures across multiple agencies create compounding problems because California’s three-agency oversight structure (Secretary of State, Franchise Tax Board, Attorney General Registry) operates independently. An organization might be current with IRS federally but suspended by both FTB and Secretary of State while also delinquent with Attorney General. Each agency problem must be resolved separately—there’s no single “fix everything” filing that restores good standing across all three agencies simultaneously. Murrieta nonprofits discovering multiple concurrent suspensions face coordinating restoration efforts across three different state agencies with different procedures, forms, fees, and timelines.

How do you discover missed filings and what’s the restoration process?

Proactive status verification through periodic checking prevents the surprise discovery of missed filings during urgent grant applications or partnerships. Organizations should regularly (quarterly or at minimum annually) verify their status with all three California agencies plus IRS: search California Secretary of State business entity database confirming “Active” status, check Franchise Tax Board exempt organization lookup confirming tax-exempt status without suspension flags, search Attorney General Registry of Charities confirming “Current” registration status, and verify IRS TEOS database showing “Eligible to receive tax-deductible contributions” without revocation warnings. Many suspended organizations only discover problems when funders notify them that due diligence verification revealed compliance issues—at which point restoration must happen urgently under deadline pressure.

Secretary of State reinstatement to Active status requires filing all overdue Statement of Information returns for each missed period (if you missed three filing cycles, you file three separate Statements), paying the current filing fee for each overdue Statement ($20 per filing currently), and potentially paying reinstatement penalties if status reached Forfeited rather than just Suspended. Secretary of State processing of reinstatement typically happens within days to a couple weeks once complete filings and fees are submitted, making SOS restoration the fastest of California’s three agencies. However, you must know your designated filing month and which periods were missed—organizations that moved or changed leadership sometimes lose track of filing schedules.

Franchise Tax Board restoration from suspension requires filing all delinquent Form 199 or Form 199N returns for every year missed, paying accrued minimum franchise taxes ($800 per year assessed while suspended), paying penalties and interest on unpaid taxes, and submitting abatement requests if circumstances warrant penalty reduction. FTB processing of reinstatement and suspension lifts typically takes 4-8 weeks after complete filings and payments are received. Organizations suspended for multiple years may owe thousands in back taxes plus penalties before FTB lifts suspension—a significant financial burden for small nonprofits that missed filings through oversight rather than deliberate avoidance.

Attorney General Registry restoration from delinquent status requires filing all overdue RRF-1 annual renewals for each year missed, paying late filing fees ($25 for renewals filed within one year of due date, increasing for longer delays), and potentially re-registering if registration lapsed entirely rather than just becoming delinquent. AG Registry processing typically happens within 2-4 weeks of receiving complete filings and fees. Unlike SOS and FTB which impose significant financial penalties, AG Registry late fees are relatively modest—but the legal exposure from fundraising without current registration is serious even though financial penalties are low.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

The Nonprofit Launch Office operates within a strategic framework designed to help California nonprofits move from formation to fundability:

Launch includes establishing compliance calendars and tracking systems from day one preventing missed filings before they occur. Launch-phase organizations should create comprehensive filing calendars showing all federal and California deadlines—IRS Form 990, California Form 199, Statement of Information in designated filing month, RRF-1 renewal deadline—with advance reminders 90, 60, and 30 days before each deadline. Organizations that launch with systematic compliance tracking rarely experience the missed filing crises that plague organizations treating compliance as afterthought rather than operational priority.

Fix is precisely what organizations with missed filings need—urgent remediation restoring good standing across all affected agencies before compliance problems block critical funding or partnership opportunities. Fix work involves discovering the full extent of filing lapses across all agencies (many organizations find multiple concurrent problems when they start investigating), prioritizing which agency restorations are most urgent based on immediate organizational needs, coordinating simultaneous filings across multiple agencies to restore complete compliance rather than fixing one problem while others persist, and implementing prevention systems ensuring missed filings don’t recur after expensive restoration efforts.

Fund becomes impossible when missed filings create suspended or delinquent status because funders conducting due diligence verification discover compliance problems and reject applications immediately. Grant applications commonly ask organizations to certify good standing with all applicable agencies—answering “yes” while actually suspended constitutes misrepresentation, while answering “no” triggers immediate disqualification. Organizations must pause grant pursuit during Fix phase while restoring compliance, then resume applications once all agencies show current status. The missed funding opportunities during restoration periods often exceed the direct costs of penalties and fees.

Federal Recognition through IRS 501(c)(3) determination remains unaffected by California state filing lapses in most cases—you can be suspended by California agencies while maintaining current federal tax-exempt status. However, IRS reviews Form 990 filings and may notice through Schedule O narratives or other disclosures that California compliance problems exist, potentially triggering questions during audits. Additionally, some funders won’t consider applications from organizations with any compliance problems regardless of whether issues are state or federal.

CA Compliance Triangle illustrates why missed California filings are particularly problematic—the three-agency structure (Secretary of State, Franchise Tax Board, Attorney General Registry) means problems can exist with one, two, or all three agencies simultaneously, and each must be resolved independently. Unlike states with single-agency nonprofit oversight, California requires maintaining current status with three separate agencies plus federal IRS, creating four verification points where problems might exist. The triangle structure means you cannot compensate for weakness in one area with strength in another—suspended FTB status blocks grant access regardless of current SOS and AG status.

Step-by-step: How NPLO helps organizations restore standing after missed filings

Step 1: Comprehensive Status Verification We check organizational status across all four agencies (IRS, CA SOS, CA FTB, CA AG Registry) identifying every compliance problem that exists rather than addressing only the one missed filing you discovered. Many organizations find multiple concurrent issues once systematic verification happens—suspended SOS status, suspended FTB status, and delinquent AG Registry all existing simultaneously. Complete assessment prevents fixing one problem while remaining unaware of others.

Step 2: Missing Filing Identification We determine which specific filings were missed, for what periods, and when they were originally due. This requires reconstructing filing history—what fiscal year does your organization use, when is your SOS designated filing month, what years have RRF-1 renewals been filed—information that organizations with poor record-keeping may have lost. Accurate identification of all missing filings prevents the problem where you file some delinquent returns but miss others, failing to achieve complete restoration.

Step 3: Restoration Priority Assessment We help prioritize which agency restorations are most urgent based on immediate organizational needs. If you have a grant application deadline in three weeks, FTB restoration (4-8 weeks processing) might not complete in time while SOS restoration (days to weeks) could, suggesting whether pursuing the grant makes sense or requires delay. If you need to sign a partnership contract immediately, SOS Active status restoration becomes top priority. Strategic prioritization focuses resources on highest-impact restoration efforts first.

Step 4: Delinquent Filing Preparation and Submission We prepare all overdue filings for each agency—completing missed Statement of Information forms with accurate current data, preparing delinquent Form 199 returns for each year missed with accurate financial information, and completing overdue RRF-1 renewals with required financial schedules. We coordinate simultaneous submission to all affected agencies rather than sequential filing that extends total restoration timeline unnecessarily.

Step 5: Penalty and Fee Calculation We calculate total costs for restoration including base filing fees for each delinquent return, reinstatement fees where applicable, accrued franchise taxes if FTB suspended, penalties and interest on unpaid amounts, and late filing fees for AG Registry renewals. Cost transparency allows organizational planning and prevents the surprise when restoration proves more expensive than anticipated—multiple years of missed filings can cost thousands in back taxes and penalties.

Step 6: Abatement Request Preparation When circumstances warrant, we prepare penalty abatement requests explaining why penalties should be reduced or waived—reasonable cause for missing filings (organizational transition, board turnover, poor recordkeeping systems now corrected), first-time penalty abatement if organization has clean history otherwise, or financial hardship making full penalty payment difficult. Agencies have discretion to reduce penalties when persuasive explanations and genuine remediation efforts are demonstrated.

Step 7: Restoration Monitoring and Verification We track submission status with each agency, follow up on processing delays, and verify once agencies update status to current/active. We obtain and save documentation of restored status—current SOS status printout, FTB exemption verification, AG Registry current status confirmation. This documentation proves to funders conducting due diligence that compliance problems have been resolved.

Step 8: Prevention System Implementation Once restoration is complete, we implement systems preventing recurrence—comprehensive compliance calendars with all filing deadlines, automated reminder systems providing advance notice before deadlines, clear responsibility assignment for tracking and completing each filing, and quarterly status verification routines catching problems early before they escalate to suspension. Prevention systems ensure expensive restoration efforts don’t repeat in future years.

Checklist: What you need to restore good standing after missed filings

Murrieta nonprofits restoring compliance after missed filings should:

- Verify status comprehensively checking IRS TEOS, CA SOS entity search, CA FTB exempt org lookup, and CA AG Registry to identify all problems

- Identify all missed filings determining which returns were due for what periods across all agencies

- Gather historical financial data needed to complete delinquent returns accurately—prior year revenues, expenses, program activities

- Calculate total restoration costs including filing fees, reinstatement fees, back taxes, penalties, interest, and late fees

- Prepare all delinquent filings completing forms accurately with historical data for each missed period

- Submit filings with payment to each affected agency simultaneously to accelerate overall restoration timeline

- Request penalty abatement if circumstances justify reduced penalties—reasonable cause, first-time abatement, hardship

- Track processing status following up with agencies about restoration timeline

- Verify restored status obtaining current status documentation from each agency once processing completes

- Pause grant applications during restoration if deadlines won’t allow completion before due diligence verification

- Notify affected funders if mid-application when compliance problems discovered, explaining restoration efforts underway

- Document lessons learned identifying why filings were missed and what systems failed

- Implement prevention systems creating calendars, reminders, responsibility assignments preventing future missed filings

- Conduct quarterly verification checking status regularly to catch future problems early before escalation

- Update board on compliance restoration, costs incurred, and prevention measures implemented

Quick Answers (PPA)

How long does it typically take to restore good standing once you discover missed filings? Restoration timeline varies by agency and how many years of filings were missed. California Secretary of State restoration happens fastest—typically days to 2 weeks after filing overdue Statement of Information and paying fees. Attorney General Registry restoration typically takes 2-4 weeks after filing overdue RRF-1 renewals. Franchise Tax Board restoration takes longest—typically 4-8 weeks after filing delinquent Form 199 returns and paying back taxes, penalties, and interest. If you missed filings with multiple agencies simultaneously, total restoration timeline is determined by the slowest agency (typically FTB), meaning you should expect minimum 4-8 weeks from starting restoration efforts to achieving complete good standing across all agencies. Organizations facing imminent grant deadlines may not have time for complete restoration before applications are due.

Can we still apply for grants while restoration is in process, or must we wait until status is fully restored? This depends on funder requirements and application timing. Most funders verify organizational status during due diligence, which for competitive grants might happen weeks or months after application deadline—if you submit application while in restoration process and status is restored before due diligence occurs, the funder may never know problems existed. However, many grant applications ask organizations to certify current good standing at time of application submission—answering “yes” while actually suspended constitutes misrepresentation even if you’re actively working on restoration. The safer approach involves transparent communication: notify funders that compliance issues exist but restoration is underway, provide documentation of restoration efforts and expected completion timeline, and ask whether they’ll consider applications conditionally pending verification of restored status. Some funders accommodate this; others maintain strict eligibility requirements requiring current status at application submission.

What if we can’t afford to pay all the back taxes and penalties—are there payment plans or options? California Franchise Tax Board offers payment plan options for organizations unable to pay full tax liabilities immediately, typically requiring some down payment with monthly payments for remaining balance over agreed period. However, suspension typically isn’t lifted until full payment or approved payment plan is established and initial payment made—you can’t restore status without addressing financial obligations. For organizations facing genuine financial hardship, requesting penalty abatement explaining circumstances and demonstrating inability to pay full amounts may reduce total obligations to manageable levels. In severe cases where years of back taxes create obligations exceeding organizational capacity to pay, consulting with tax professionals about options including potential tax-exempt status reinstatement procedures or organizational dissolution and reformation may be necessary—though dissolution and reformation creates significant complications and should be last resort.

Will missed California state filings affect our federal IRS tax-exempt status? Generally no—California state filing lapses don’t directly affect federal IRS 501(c)(3) status. You can be suspended by California Franchise Tax Board while maintaining current IRS recognition, or be delinquent with Attorney General Registry while showing “Eligible to receive tax-deductible contributions” in IRS TEOS database. Federal and state tax-exempt statuses are separate and independent. However, IRS Form 990 includes questions about compliance with state filing requirements, and persistent state compliance problems might raise IRS questions during audits or reviews about overall organizational management quality. Additionally, some state compliance problems (like failure to maintain registered agent) might prevent IRS from communicating with organization about federal matters, potentially creating indirect federal problems. The key point is that state filing lapses should be corrected to restore state standing, but they don’t immediately trigger federal IRS revocation.

How do we prevent this from happening again after going through expensive restoration? Prevention requires systematic compliance management rather than reactive crisis response. Create comprehensive filing calendar listing every federal and California deadline—IRS Form 990 (15th day of 5th month after fiscal year end), California Form 199 (same deadline as 990), Statement of Information (specific designated filing month every two years), RRF-1 renewal (within 4 months 15 days after fiscal year end). Set automated reminders 90, 60, and 30 days before each deadline. Assign clear responsibility for tracking and completing filings—board treasurer, executive director, bookkeeper, or outside accountant depending on organizational structure. Conduct quarterly status verification checking all four agencies (IRS, SOS, FTB, AG) to catch problems early. Maintain organized records of when filings were submitted and confirmations received. Budget annually for filing fees and professional preparation assistance. Many Murrieta nonprofits that experienced suspension implement these systems and never face compliance crises again.

What to do next (DIY vs Done-With-You)

DIY approach: Immediately verify your current status with all four agencies: search IRS TEOS database at apps.irs.gov/app/eos, check California Secretary of State business entity search at bizfileonline.sos.ca.gov, verify Franchise Tax Board exempt organization status, and search Attorney General Registry of Charities at oag.ca.gov/charities. Save screenshots showing current status for all four agencies dated today. If any show suspended or delinquent status, determine which specific filings were missed—review organizational records to identify your fiscal year end, SOS designated filing month, and when last filings were submitted for Form 990, Form 199, Statement of Information, and RRF-1. Calculate how many years or periods of filings are missing. Gather financial data needed to complete delinquent returns—prior year revenues, expenses, program information from bank records, board minutes, or other documentation. Download appropriate forms for each missed filing from agency websites. Complete all delinquent filings accurately. Calculate total fees, taxes, penalties, and interest owed. Submit all filings simultaneously with required payments. Track processing status and follow up if delays occur. Once restored, create compliance calendar preventing recurrence and implement quarterly status verification routine.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive compliance restoration for Murrieta and Inland Empire nonprofits facing suspended or delinquent status from missed state filings. We conduct thorough verification across all four agencies identifying every compliance problem comprehensively, reconstruct filing history determining which returns were missed for what periods, gather and organize historical data needed for accurate delinquent filing preparation, prepare all overdue filings with proper financial information and narratives, calculate total restoration costs including fees, taxes, penalties, and interest, coordinate simultaneous submission to all agencies accelerating overall restoration timeline, prepare penalty abatement requests when circumstances warrant reduced penalties, track processing status and follow up ensuring timely completion, verify restored status and obtain documentation proving compliance resolution, communicate with funders if mid-application explaining restoration efforts and timeline, implement prevention systems including calendars, reminders, and responsibility assignments, and provide ongoing compliance monitoring preventing future missed filing crises. This comprehensive approach resolves current problems while preventing expensive repeat occurrences.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Sources

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.