02 Feb What Does an IRS Determination Letter Prove to a Funder?

Short Answer

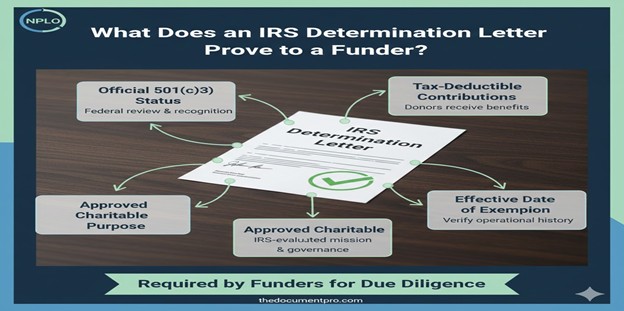

An IRS determination letter proves that the organization underwent federal review and received official recognition as a 501(c)(3) charitable organization, that donor contributions to the organization are tax-deductible, that the organization qualified based on specific charitable purposes and governance structures evaluated by IRS, and that tax-exempt status became effective on a specific date allowing verification of how long the organization has operated with federal recognition. Funders require determination letters because the letter provides definitive proof of federal tax-exempt status that organizational claims alone cannot offer, the letter demonstrates that IRS evaluated and approved the organization’s charitable purposes and governance, and most foundation and corporate grant programs explicitly require grantees to submit current determination letters as part of due diligence documentation proving eligibility.

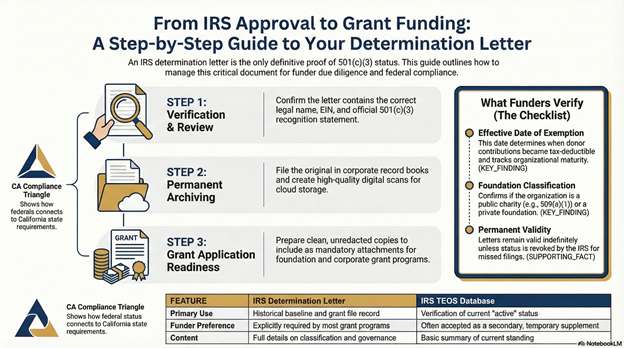

What specific information does the determination letter contain?

Official IRS recognition statement declares that the organization is recognized as tax-exempt under Section 501(c)(3). This formal declaration from the IRS provides legal authority that the organization qualifies for federal tax exemption. Without this official statement, organizations cannot legitimately claim federal tax-exempt status regardless of California incorporation or stated charitable purposes.

Effective date of exemption establishes when tax-exempt recognition began. For most organizations, this date matches incorporation date if Form 1023/1023-EZ was filed within 27 months of incorporation. The effective date matters because it determines when donors can claim tax deductions for contributions and when the organization became exempt from federal income tax on mission-related revenue. Funders reviewing determination letters verify the effective date to understand organizational maturity.

Foundation classification indicates whether the organization is a public charity or private foundation. Most determination letters state the organization is classified as a 509(a)(1) or 509(a)(2) public charity, meaning it receives broad public support rather than funding from a single source. This classification matters because different rules apply to public charities versus private foundations, and most funders prefer supporting public charities. The letter confirms which classification applies.

Advance ruling period information appears for some older determination letters. Previously, IRS issued “advance ruling” letters requiring organizations to demonstrate public support during an initial period before receiving permanent status. Current process typically provides definitive determinations immediately. However, older determination letters still valid may reference advance ruling periods that have since concluded, requiring organizations to hold foundation status determination letters confirming permanent classification.

Why do funders request determination letters beyond TEOS verification?

Physical documentation for grant files provides tangible proof of eligibility. While funders verify organizations in TEOS database, they also require physical determination letters filed in grant documentation. The letter serves as permanent record that due diligence was completed and that the grantee qualified as a 501(c)(3) at the time of grant award. If questions arise years later about whether proper verification occurred, the determination letter in the file provides documentation.

Verification of organization details beyond just tax-exempt status occurs through determination letter review. The letter shows the organization’s official legal name, EIN, and address as recorded by IRS at time of determination. Funders verify this information matches what appears on grant applications ensuring consistency. Discrepancies between determination letter information and application information raise questions requiring explanation.

Demonstration of IRS review and approval provides confidence in organizational legitimacy. The determination letter proves that IRS examined the organization’s purposes, governance structures, financial projections, and operational plans before granting recognition. This federal review and approval adds credibility beyond self-reported information on grant applications. Organizations without determination letters claiming to be “nonprofits” haven’t undergone federal scrutiny.

Protection against revocation or fraud risk motivates funder requests for determination letters. While TEOS database shows current status, determination letters provide historical baseline. If an organization claims 501(c)(3) status but cannot produce a determination letter, it raises questions about whether recognition was ever actually granted or whether the organization is misrepresenting its status. Legitimate organizations possess determination letters they can readily provide.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

Launch includes obtaining determination letters and maintaining them in permanent organizational records. Moreno Valley nonprofits should save original determination letters in corporate records books, create digital copies for easy sharing, and verify that letters contain all standard elements proving recognition.

Fix addresses situations where organizations lost determination letters requiring replacement requests from IRS, or where organizations operated for years without determination letters because recognition was never actually obtained requiring immediate Form 1023/1023-EZ applications.

Fund access depends on providing current determination letters when requested. Grant applications commonly include determination letters as required attachments. Organizations unable to provide determination letters fail basic eligibility requirements regardless of program quality.

Federal Recognition is precisely what determination letters prove. The letter is the official IRS document confirming that federal tax-exempt status was granted, when it became effective, and what classification applies.

CA Compliance Triangle operates independently—determination letters prove federal IRS recognition but say nothing about California Secretary of State, Franchise Tax Board, or Attorney General status. Funders require both determination letters AND California verification documents.

Step-by-step: How NPLO helps organizations manage determination letters

Step 1: Receipt Verification We verify clients received complete determination letters after IRS approval with all standard elements.

Step 2: Information Review We review determination letters confirming information is accurate—correct legal name, EIN, classification.

Step 3: Permanent Storage We ensure determination letters are filed in organizational records books for safekeeping.

Step 4: Digital Archiving We create high-quality digital scans for electronic sharing with funders.

Step 5: Replacement Requests If determination letters are lost, we help request certified copies from IRS.

Step 6: Grant Application Preparation We prepare determination letter copies in formats funders commonly request.

Step 7: Update Handling If determination letters are superseded by foundation status letters or amendments, we ensure current versions are used.

Step 8: Board Communication We educate boards about determination letter significance and storage responsibility.

Checklist: What determination letters should contain

- IRS letterhead and official signature

- Statement recognizing organization as 501(c)(3)

- Organization’s official legal name

- Employer Identification Number (EIN)

- Effective date of tax-exempt status

- Foundation classification (public charity or private foundation)

- Statement that contributions are deductible

- Reference to Internal Revenue Code Section 501(c)(3)

- Date letter was issued

- IRS contact information

- Clear without redactions obscuring critical information

- High-quality legible copy (if using copies rather than original)

Quick Answers (PPA)

Our determination letter was issued 15 years ago—is it still valid, or do we need a new one? Determination letters remain valid indefinitely unless IRS revokes recognition through specific actions like automatic revocation for missed Form 990 filings or determination that operations no longer serve charitable purposes. Organizations in continuous good standing since receiving determination 15 years ago can continue using that letter—IRS doesn’t require renewal or reissuance at intervals. However, verify your current status in TEOS database showing you’re still recognized and eligible to receive deductible contributions. If TEOS shows revoked status, your old determination letter is no longer valid and you’ll need reinstatement. Also note that very old determination letters may reference outdated IRS procedures or advance ruling periods that have concluded—these letters remain valid but you may want to include TEOS printout alongside them showing current active status.

We lost our determination letter—how do we get a replacement, and how long does it take? Request certified copies from IRS by writing to IRS Exempt Organizations Determinations office or calling Tax Exempt and Government Entities division. Include your organization’s legal name, EIN, address, and approximate date of determination. Explain you’re requesting a certified copy of the determination letter for your records. IRS typically provides certified copies for a fee (currently around $85). Processing times vary but expect 4-8 weeks minimum. While waiting, generate current TEOS printouts showing your organization’s active status—many funders will accept TEOS verification temporarily if you explain determination letter replacement is pending. However, secure the replacement letter for permanent files since some funders specifically require the physical determination letter regardless of TEOS status.

What if our determination letter shows a different address or name than we currently use—does that invalidate it? Address changes don’t invalidate determination letters—organizations move locations frequently. However, you should notify IRS of address changes by filing Form 8822-B ensuring future correspondence reaches you and updating TEOS database information. Legal name changes are more significant and may require IRS notification through letter explaining the change with documentation like amended Articles of Incorporation. If operating under a DBA (doing business as) name different from legal name on determination letter, include explanation for funders clarifying that the DBA is the same organization. Substantial changes to organizational structure or purposes might require amended determination applications. For typical address moves or minor name adjustments, original determination letters remain valid with explanatory documentation.

Can we provide funders with a TEOS printout instead of the determination letter, or do they specifically need the letter? Funder requirements vary—some explicitly require the physical determination letter as part of grant documentation, while others accept TEOS printouts as equivalent verification. When grant applications specify “provide copy of IRS determination letter,” provide the actual letter. When requirements are less specific or say “proof of 501(c)(3) status,” TEOS printouts may suffice. Best practice is providing both—determination letter plus current TEOS printout dated within 30 days. The determination letter shows historical baseline of when and how recognition was granted, while TEOS printout confirms current active status. If you have your determination letter available, always provide it rather than substituting TEOS printout unless space limitations or funder preferences dictate otherwise.

What if we applied for 501(c)(3) recognition but haven’t received determination yet—what do we tell funders? Be completely transparent that determination is pending. Grant applications asking about 501(c)(3) status should receive honest answers: “We applied for 501(c)(3) recognition on [date] and are awaiting IRS determination. Recognition has not yet been granted.” Most funders cannot consider applications from organizations lacking current 501(c)(3) recognition regardless of pending applications. However, some foundations have programs specifically supporting emerging organizations during formation and may consider applications with pending status if you’re transparent. Never claim you have 501(c)(3) status before IRS actually grants it and you receive the determination letter—misrepresentation discovered during verification results in permanent disqualification from that funder and potential fraud investigation. Wait to submit grant applications until after receiving determination whenever possible.

What to do next (DIY vs Done-With-You)

DIY approach: Locate your organization’s IRS determination letter in organizational records. If you have it, create multiple high-quality scans or photocopies maintaining legibility, save digital versions in secure cloud storage and local backup, file physical original in permanent corporate records book section for formation documents, and prepare easily accessible copies for sharing with funders. Verify that your determination letter contains all standard elements—IRS recognition statement, effective date, foundation classification, deductibility statement—and that information matches your current organizational details. If determination letter is lost, prepare request to IRS Exempt Organizations Determinations office including organization name, EIN, address, and approximate determination date requesting certified copy. While waiting for replacement, generate current TEOS printouts for temporary verification. If your organization never received determination letter because Form 1023/1023-EZ was never filed, prioritize IRS application immediately—you’re not actually tax-exempt without it regardless of years of operation. For grant applications, attach determination letter copies as requested ensuring documents are legible and complete without critical information obscured.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive determination letter management for Moreno Valley and Inland Empire nonprofits. We verify clients received complete determination letters after IRS approval, review determination letters confirming all standard elements and accurate information, establish permanent storage in organizational records books, create high-quality digital archives for electronic sharing, request IRS certified copies when letters are lost, prepare determination letter copies in formats funders commonly request, handle updates when foundation status letters or amendments supersede original determinations, educate boards about determination letter significance and preservation responsibility, and provide immediate access to determination letters when grant opportunities require rapid response. This ensures you maintain the definitive federal recognition documentation that funders require when evaluating whether to support your work.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Find Us Locally

Service Area: Moreno Valley, CA and surrounding areas

Coordinates: 33.9535, -117.2081

Address: 23945 Sunnymead Blvd. #4, Moreno Valley, CA 92553

Sources

- https://www.irs.gov/charities-non-profits/charitable-organizations

- https://www.irs.gov/forms-pubs/about-form-1023

- https://calnonprofits.org/

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.