31 Jan What Is a 501(c)(3) at a High Level and What Does It Allow?

Short Answer

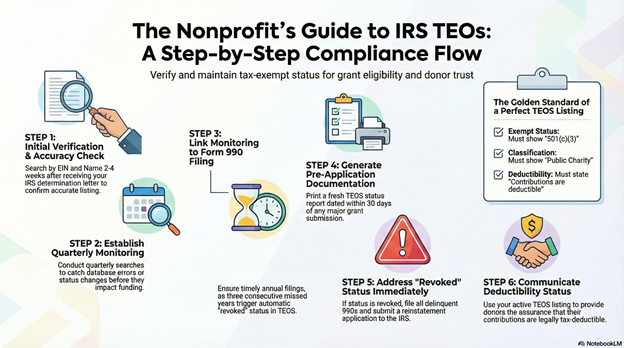

IRS Tax Exempt Organization Search (TEOS) is the official public database at apps.irs.gov/app/eos where anyone can verify an organization’s current federal tax-exempt status, search by organization name or EIN, and view determination details including effective date and exempt status type. TEOS matters because funders independently verify 501(c)(3) recognition by searching this database before approving grants, the listing provides instant public proof of legitimate tax-exempt status that organizational claims alone cannot offer, donors verify organizations before making tax-deductible contributions, and absence from TEOS or showing “revoked” status triggers immediate rejection of grant applications regardless of program quality or organizational claims about tax-exempt status.

What does 501(c)(3) status actually provide?

Federal income tax exemption represents the core benefit. Organizations with 501(c)(3) recognition don’t pay federal income tax on revenue generated through mission-related activities—donations received, grants awarded, program fees charged, and other income supporting charitable purposes. This exemption doesn’t cover unrelated business income (revenue from activities substantially unrelated to charitable mission), which remains taxable. However, the ability to receive hundreds of thousands in donations and grants without owing federal tax on that revenue provides enormous financial advantage.

Donor tax deductibility creates powerful fundraising incentive. Individual and corporate donors can deduct contributions to 501(c)(3) organizations on their federal tax returns (subject to percentage limitations), making donations more attractive than giving to non-recognized organizations. A donor in the 24% tax bracket effectively pays only $760 for a $1,000 donation to a 501(c)(3) because the deduction reduces their tax liability by $240. This tax benefit motivates giving especially for major donors seeking tax efficiency.

Grant eligibility depends almost universally on 501(c)(3) status. Most foundations, corporate giving programs, and government funding sources restrict grants to IRS-recognized 501(c)(3) organizations. Without federal recognition, Riverside nonprofits cannot access the vast majority of institutional funding regardless of program quality or community need. The determination letter opens doors to foundation grants, corporate sponsorships, and government contracts that would otherwise be completely unavailable.

Public recognition and credibility flow from official IRS designation. The 501(c)(3) determination signals to funders, partners, volunteers, and the public that your organization underwent IRS scrutiny, demonstrated compliance with federal charitable organization standards, and operates under ongoing oversight requirements. Being listed in the IRS Tax Exempt Organization Search (TEOS) database provides instant verification of legitimate nonprofit status that self-proclaimed “nonprofits” without recognition cannot offer.

What organizations qualify for 501(c)(3) status?

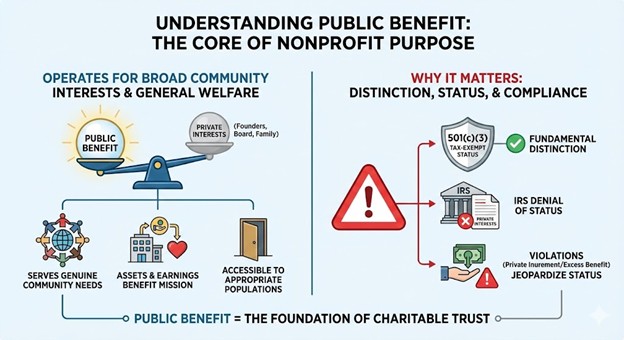

Charitable purposes recognized under Section 501(c)(3) include relief of the poor, distressed, or underprivileged; advancement of religion; advancement of education or science; erection or maintenance of public buildings, monuments, or works; lessening the burdens of government; lessening neighborhood tensions; eliminating prejudice and discrimination; defending human and civil rights secured by law; and combating community deterioration and juvenile delinquency. Organizations must operate exclusively for one or more of these purposes—not mixing charitable work with substantial non-charitable activities.

Public charities versus private foundations represent two 501(c)(3) categories with different rules. Most organizations new founders create are public charities—organizations that receive substantial public support through donations, grants, or earned income from charitable activities. Public charities face fewer restrictions and higher contribution deduction limits for donors. Private foundations typically receive funding from single sources (wealthy individuals or families) and primarily make grants to other charities rather than conducting direct programs. Most Riverside nonprofits should structure as public charities.

Organizational and operational tests determine qualification. The organizational test requires that Articles of Incorporation limit purposes to recognized charitable categories and include required dissolution language directing assets to other 501(c)(3)s upon dissolution. The operational test requires that actual activities primarily further charitable purposes, that no substantial part of activities involve lobbying or political campaign intervention, and that no net earnings benefit private individuals beyond reasonable compensation for services.

Ongoing compliance obligations accompany 501(c)(3) recognition. Organizations must file annual Form 990 information returns (or Form 990-N e-Postcard for small organizations) reporting activities and finances, maintain charitable purpose focus as activities evolve, preserve corporate records including minutes and financial statements, avoid prohibited political campaign intervention, and limit lobbying to insubstantial amounts. Failure to maintain compliance can result in revocation of tax-exempt status.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

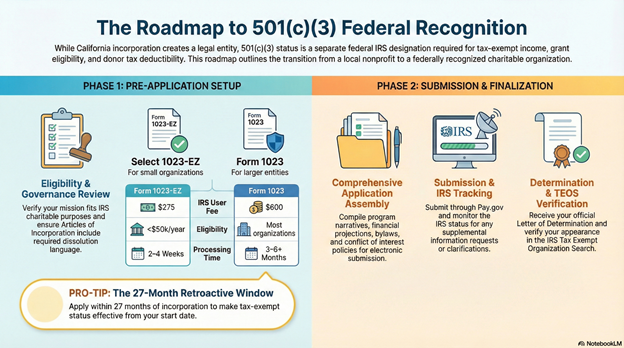

Launch for Riverside nonprofits must include pursuing 501(c)(3) determination as primary formation milestone. Organizations that incorporate in California but never file IRS Form 1023/1023-EZ applications remain legally non-tax-exempt regardless of charitable intentions.

Fix becomes necessary when organizations operated for years assuming they had 501(c)(3) status based on California incorporation alone, accepted donations claiming tax-deductibility without IRS recognition, or lost recognition through compliance failures requiring reinstatement applications.

Fund access depends almost entirely on 501(c)(3) status. Grant makers verify federal recognition through TEOS database searches—organizations not showing “Eligible to receive tax-deductible contributions” face immediate application rejection.

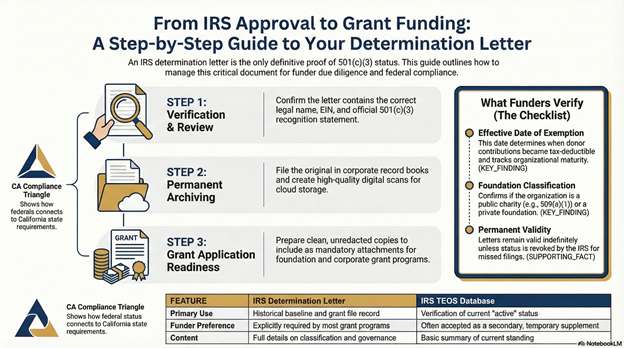

Federal Recognition IS the 501(c)(3) status—they’re synonymous. The IRS determination letter provides official recognition that organizations have qualified under Section 501(c)(3) of the Internal Revenue Code.

CA Compliance Triangle operates independently of federal 501(c)(3) status. Organizations can have IRS recognition while suspended by California agencies, or be current in California while lacking federal recognition. Both federal AND California compliance are required for full grant-readiness.

Step-by-step: How NPLO helps organizations achieve 501(c)(3) recognition

Step 1: Eligibility Assessment We verify your planned activities qualify under recognized 501(c)(3) charitable purposes.

Step 2: Articles Review We ensure California Articles of Incorporation contain required IRS language including dissolution clauses.

Step 3: Form Selection We determine whether Form 1023-EZ (simpler, $275, for qualifying small organizations) or Form 1023 (detailed, $600, for most organizations) is appropriate.

Step 4: Application Preparation We prepare complete Form 1023/1023-EZ applications including narrative descriptions, financial projections, governance documentation, and required exhibits.

Step 5: Supporting Documentation We compile bylaws, conflict policies, board meeting minutes, and other documents IRS requests with applications.

Step 6: Submission and Tracking We submit applications electronically, track processing status, and respond to IRS questions or supplemental information requests.

Step 7: Determination Letter Receipt We obtain official determination letters confirming 501(c)(3) recognition and effective dates.

Step 8: TEOS Verification We verify organizations appear correctly in IRS Tax Exempt Organization Search database showing eligible status.

Checklist: What 501(c)(3) status provides

Tax Benefits:

- Federal income tax exemption on mission-related revenue

- Donor tax deductibility for contributions

- Potential state income tax exemption (separate CA application)

- Potential property tax exemption (if owning real estate)

- Potential sales tax exemption (for eligible purchases in some states)

Funding Access:

- Foundation grant eligibility

- Corporate giving program access

- Government contract opportunities

- Individual donor motivation through deductibility

Operational Benefits:

- Nonprofit postage rates (significant savings)

- Discounted rates from some vendors

- Access to donated technology/services

- Volunteer recruitment appeal

Credibility Benefits:

- IRS TEOS database listing

- Official determination letter

- Public recognition as legitimate charity

- Enhanced donor/partner confidence

Required Compliance:

- Annual Form 990 filing

- Maintain charitable purpose focus

- No private inurement

- Limited lobbying

- No political campaign intervention

Quick Answers (PPA)

Does California incorporation automatically provide 501(c)(3) status, or is IRS application required? IRS application is absolutely required—California incorporation provides zero federal tax benefits. Filing Articles of Incorporation with California Secretary of State creates a California nonprofit corporation but doesn’t make it tax-exempt federally. You must separately apply to IRS using Form 1023 or Form 1023-EZ and receive an official determination letter before you have 501(c)(3) status. Many founders mistakenly believe incorporation equals tax-exempt status and operate for years without IRS recognition, only discovering the problem when funders verify federal status or donors request determination letters. Complete both California incorporation AND IRS determination application.

How long does IRS determination take, and can we operate as a nonprofit while waiting? IRS processing times vary—Form 1023-EZ typically processes within 2-4 weeks while Form 1023 often takes 3-6 months or longer depending on IRS workload and whether applications require supplemental information. You can operate as a California nonprofit corporation while waiting, but you’re not yet federally tax-exempt so you cannot legitimately tell donors their contributions are tax-deductible until you receive determination. Organizations applying within 27 months of incorporation date receive retroactive recognition effective from incorporation if approved, allowing donors during that period to claim deductions retroactively. Best practice is filing IRS applications immediately after incorporation minimizing the waiting period.

Can 501(c)(3) organizations engage in any political activity, or is it completely prohibited? Political campaign intervention (supporting or opposing candidates for public office) is absolutely prohibited—any amount jeopardizes tax-exempt status. However, issue advocacy and lobbying on legislation is permitted as long as it doesn’t constitute a substantial part of activities (generally interpreted as consuming less than 5-10% of budget/time). Organizations can educate about issues, advocate for policy positions, and even lobby legislators about specific bills without losing exemption, but cannot endorse candidates, contribute to campaigns, or make statements supporting/opposing candidates in official capacity. Navigating this distinction requires careful attention to IRS guidance.

What’s the difference between 501(c)(3) and other 501(c) categories like 501(c)(4)? 501(c)(3) organizations are charitable organizations where donor contributions are tax-deductible. 501(c)(4) organizations are social welfare organizations that can engage in more lobbying and limited political activity but donor contributions are NOT tax-deductible. 501(c)(6) covers business leagues and trade associations. Each subsection serves different purposes with different rules. Most organizations providing direct charitable services (education, poverty relief, health services) should be 501(c)(3). Organizations focused primarily on advocacy, lobbying, or political activity might be better suited to 501(c)(4). The tax-deductibility distinction is critical—if you want donors to deduct contributions, you need 501(c)(3).

Can we lose 501(c)(3) status once we have it, and what causes revocation? Yes, organizations can lose recognition through automatic revocation (failing to file required Form 990 returns for three consecutive years triggers automatic revocation), IRS determination that operations no longer serve charitable purposes, substantial private benefit or private inurement violations, political campaign intervention, or activities primarily serving non-charitable purposes. Organizations revoked for non-filing can apply for retroactive reinstatement if they act within specific timeframes. Organizations revoked for substantive violations typically must reapply and may face IRS skepticism. Maintaining recognition requires ongoing compliance with filing requirements and operational standards—it’s not a one-time achievement but continuous obligation.

What to do next (DIY vs Done-With-You)

DIY approach: Verify your California Articles of Incorporation contain required IRS language including specific charitable purpose statements and asset dissolution clauses directing assets to other 501(c)(3) organizations upon dissolution—if Articles lack required language, you’ll need to amend them before IRS application. Determine which form to file: Form 1023-EZ ($275 fee) for organizations projecting less than $50,000 gross receipts annually with limited asset holdings, or Form 1023 ($600 fee) for larger organizations or those not qualifying for EZ. Review IRS Form 1023 or 1023-EZ instructions thoroughly understanding required information—organizational descriptions, governance structure, program narratives, financial projections, conflict policies. Gather supporting documents IRS requests—bylaws, board meeting minutes, financial statements or projections. Complete application carefully answering all questions accurately and completely. Create Pay.gov account for paying user fees electronically. Submit application through IRS online system. Track application status through IRS online portal. Respond promptly to any IRS questions or supplemental information requests. Upon approval, obtain determination letter and verify appearance in TEOS database. Timeline: expect 2-4 weeks for 1023-EZ, 3-6+ months for Form 1023.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive 501(c)(3) determination support for Riverside and Inland Empire nonprofits. We assess whether planned activities qualify under recognized charitable purposes, review and if necessary amend California Articles ensuring required IRS language, determine appropriate form (1023-EZ vs 1023) based on organizational characteristics, prepare complete applications including narrative program descriptions and financial projections, compile supporting documentation including bylaws and policies, submit applications electronically handling all IRS correspondence, track processing status and respond to supplemental information requests, obtain official determination letters upon approval, and verify correct TEOS database listing showing eligible status. This ensures your application is complete, accurate, and professionally presented maximizing approval likelihood while minimizing processing delays from incomplete submissions or IRS questions requiring clarification.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Find Us Locally

Service Area: Moreno Valley, CA and surrounding areas

Coordinates: 33.9535, -117.2081

Address: 23945 Sunnymead Blvd. #4, Moreno Valley, CA 92553

Sources

- https://www.irs.gov/charities-non-profits/charitable-organizations

- https://www.irs.gov/forms-pubs/about-form-1023

- https://calnonprofits.org/

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.