27 Feb Documents Needed to Start a Non-Profit in Perris, CA: A Checklist

To start a non-profit in Perris, CA, you need several key documents including Articles of Incorporation, organizational bylaws, IRS Form 1023 or 1023-EZ, conflict of interest policy, and initial board meeting minutes. Preparing these documents accurately ensures smooth filing with California and federal agencies and helps avoid delays in the approval process.

This guide provides educational information and does not constitute legal or tax advice.

Answer-First Summary

- State filing document: Articles of Incorporation (Form ARTS-PB-501) filed with California Secretary of State – $30 filing fee

- Governance documents: Organizational bylaws, conflict of interest policy, board resolutions (not filed with state but required for IRS)

- Federal tax-exempt application: IRS Form 1023-EZ ($275) or Form 1023 ($600) for 501(c)(3) status

- Tax identification: Employer Identification Number (EIN) from IRS – free, obtained before tax-exempt application

- Timeline: California state filing 5-7 business days; IRS determination 2-6+ months; complete process typically 3-9 months

- After approval: Statement of Information (Form SI-100) due within 90 days of incorporation, California Attorney General charitable registration if fundraising

Quick Actions Checklist

- Prepare Articles of Incorporation meeting California Corporations Code requirements

- Draft comprehensive organizational bylaws tailored to your governance structure

- Obtain Employer Identification Number (EIN) from IRS (free online application)

- Complete IRS Form 1023-EZ or Form 1023 for federal tax-exempt status

- Adopt conflict of interest policy and additional governance documents

- Hold and document first board of directors meeting with proper minutes

- File Articles of Incorporation with California Secretary of State ($30 fee)

- After state approval, submit IRS tax-exempt application

- Register with California Attorney General’s Registry of Charitable Trusts (if fundraising)

- File Statement of Information (Form SI-100) within 90 days of incorporation ($20 fee)

Essential Documents for California Non-Profit Formation

Articles of Incorporation (State Filing Document)

The Articles of Incorporation (Form ARTS-PB-501) is your foundational legal document that creates your non-profit corporation under California law. This document must be filed with the California Secretary of State and includes:

Required information:

- Organization’s name (must be distinguishable from existing entities and include “corporation,” “incorporated,” “corp.,” or “inc.”)

- Statement of non-profit purpose

- Initial agent for service of process and address

- Initial street address of the corporation

- Provisions for distribution of assets upon dissolution

- Statement that organization is organized under California Nonprofit Public Benefit Corporation Law

The California Secretary of State charges a $30 filing fee. Processing typically takes 5-7 business days for standard filing, with expedited options available ($350 for 24-hour or $500 for same-day processing).

Critical requirements: Articles must comply with California Corporations Code sections 5120-5121. Improper formatting or missing required provisions will result in rejection and resubmission delays.

Organizational Bylaws

Bylaws are your internal governance document that establishes rules for operating your non-profit corporation. While not filed with the California Secretary of State, bylaws are required for IRS tax-exempt applications and proper organizational governance.

Bylaws typically include:

- Board of directors structure, size, and election procedures

- Officer roles and responsibilities

- Meeting requirements and quorum rules

- Voting procedures for board decisions

- Committee formation and authority

- Membership provisions (if applicable)

- Amendment procedures

- Fiscal year definition

- Dissolution procedures

Bylaws must align with your Articles of Incorporation and cannot contradict provisions stated in the Articles. The IRS reviews bylaws during tax-exempt application processing to ensure proper governance structure.

Conflict of Interest Policy

California strongly recommends that non-profit corporations adopt a conflict of interest policy. The IRS requires this policy for tax-exempt status applications. This document establishes procedures for:

Policy components:

- Identifying potential conflicts of interest among board members and officers

- Disclosure requirements when conflicts arise

- Recusal procedures for conflicted individuals

- Annual disclosure statements from board members

- Review and approval processes for potentially conflicted transactions

The IRS provides a sample conflict of interest policy in Form 1023 instructions that can be adapted to your organization’s needs.

Board Meeting Minutes and Resolutions

Documentation of your initial board meeting and organizational resolutions demonstrates proper corporate governance. Required documentation includes:

Initial meeting records:

- Minutes of first board meeting

- Resolution adopting bylaws

- Resolution adopting conflict of interest policy

- Resolution authorizing officers to open bank accounts

- Resolution authorizing IRS tax-exempt application filing

- Appointment of officers resolution

These documents aren’t filed with government agencies but must be maintained in your corporate records and may be requested during IRS application review.

Federal Tax-Exempt Application Documents

Employer Identification Number (EIN)

Before applying for tax-exempt status, you must obtain an EIN from the IRS. This federal tax identification number is free and can be obtained immediately through the IRS online EIN application system.

The EIN is required for:

- Opening bank accounts in the organization’s name

- Filing IRS Form 1023 or 1023-EZ

- Future tax filings and correspondence with IRS

- Employment tax reporting (if hiring staff)

Application process: Visit IRS.gov and complete the online EIN application. You’ll receive your EIN immediately upon completion. This must be done before submitting your tax-exempt application.

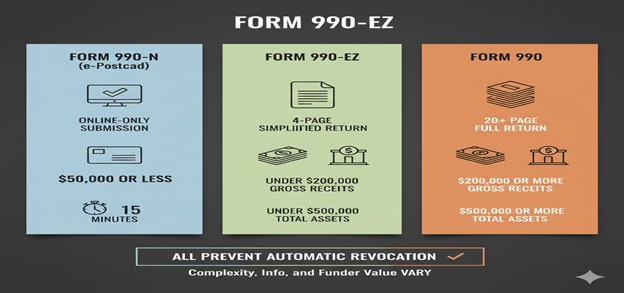

IRS Form 1023-EZ or Form 1023

After California approves your Articles of Incorporation, you apply for federal 501(c)(3) tax-exempt status using either the streamlined Form 1023-EZ or full Form 1023.

Form 1023-EZ eligibility ($275 user fee):

- Projected annual gross receipts under $50,000

- Total assets under $250,000

- Not a hospital, school, university, or supporting organization

- Simpler application with fewer narrative requirements

Form 1023 requirements ($600 user fee):

- Organizations not qualifying for Form 1023-EZ

- Requires detailed narrative descriptions of activities

- Financial projections for three years

- More extensive supporting documentation

Both forms require:

- Approved California Articles of Incorporation

- Organizational bylaws

- Conflict of interest policy

- Board member and officer information

- Detailed description of planned activities

- Financial information or projections

IRS processing typically takes 2-6 months, though timelines can extend longer depending on application volume and complexity.

Post-Formation Compliance Documents

Statement of Information (Form SI-100)

Within 90 days of incorporation, California requires filing a Statement of Information with the Secretary of State. This form provides:

- Current officer and director names and addresses

- Current business address

- Principal office location

- Brief description of business type

Filing fee: $20 Frequency: Must be filed biennially (every two years) thereafter

Failure to file the Statement of Information on time results in penalties and potential suspension of corporate status.

California Attorney General Registration

If your non-profit plans to solicit donations in California, you must register with the California Attorney General’s Registry of Charitable Trusts. Registration requirements include:

- Initial registration (Form CT-1) – typically due within 30 days of receiving charitable assets

- Copy of IRS determination letter

- Financial statements

- Annual renewal (Form RRF-1) with financial reporting

Registration is free initially, but annual renewal fees apply based on your organization’s gross revenue.

Why Choose The Document Pro – Non-Profit Launch Office

California Specialization: The Non-Profit Launch Office (NPLO), operated by The Document Pro and Gitta Williams, focuses exclusively on California non-profit formation with deep knowledge of state requirements.

Comprehensive Document Preparation: We prepare all required documents including Articles of Incorporation, bylaws, conflict of interest policies, board resolutions, and assist with IRS tax-exempt applications.

Inland Empire Expertise: Serving Perris, Moreno Valley, Riverside County, and throughout the Inland Empire with local knowledge and statewide California coverage.

After-Hours Support: Our AI assistant provides intake, guidance, and document preparation assistance outside regular business hours.

Transparent Pricing: $400-$1,200 based on organizational complexity, with clear explanation of included services.

Contact: Phone 1(800) 285-0078 | Email mydocumentpro@gmail.com

For detailed cost information: Cost to Prepare Non-Profit Papers in Perris, CA

Frequently Asked Questions

What is the first document I need to file to start a non-profit in Perris?

The first legal document is the Articles of Incorporation (Form ARTS-PB-501), which you file with the California Secretary of State to establish your non-profit's legal existence. This creates your corporation under California law and is required before you can apply for federal tax-exempt status. The filing fee is $30 with standard processing of 5–7 business days.

Do I need to file IRS Form 1023 or 1023-EZ?

It depends on your organization's size and structure. Form 1023-EZ (streamlined application, $275 fee) is available for organizations with projected annual gross receipts under $50,000 and assets under $250,000. Larger organizations or those not meeting eligibility criteria must file the full Form 1023 ($600 fee). The IRS provides an eligibility worksheet to help determine which form is appropriate.

How long does the filing process take in California?

California Secretary of State processing typically takes 5–7 business days for standard Articles of Incorporation filing. Expedited processing is available (24-hour for +$350 or same-day for +$500). After state approval, IRS tax-exempt status processing typically takes 2–6 months, though it can extend longer. Complete formation from initial state filing to IRS determination letter usually requires 3–9 months total.

Is an EIN required before applying for tax exemption?

Yes, you must obtain your Employer Identification Number (EIN) from the IRS before submitting Form 1023 or 1023-EZ. The EIN is free and can be obtained immediately through the IRS online application system. This federal tax ID is required for opening bank accounts and all IRS correspondence.

What is a Conflict of Interest Policy and do I need one?

A conflict of interest policy establishes procedures for identifying and managing situations where board members or officers have personal interests that could influence organizational decisions. California strongly recommends this policy, and the IRS requires it for tax-exempt status applications. The policy ensures transparency and proper governance procedures.

Are there any local Perris-specific filing requirements?

Perris follows standard California state regulations for non-profit formation. However, depending on your organization's activities, you may need local business licenses or permits from the City of Perris or Riverside County. Check with local government offices about requirements specific to your planned activities, especially if operating a physical location or hosting public events.

Can The Document Pro help prepare these documents?

Yes, The Document Pro – Non-Profit Launch Office specializes in preparing all essential non-profit formation documents for California organizations. We prepare Articles of Incorporation, bylaws, conflict of interest policies, board resolutions, and assist with IRS tax-exempt applications. Our services range from $400–$1,200 based on organizational complexity. Contact us at 1(800) 285-0078 for consultation.

Additional Resources

- Starting a Nonprofit in California

- Documents Needed to Start a Non-Profit in Perris, CA

- Urgent 24/7 Non-Profit Filing Help in Perris, CA

- Top Rated Non-Profit Filing Companies Near Perris

External Authority Sources

- California Secretary of State – Nonprofit Corporation Filing Requirements

- Internal Revenue Service (IRS) – Tax-Exempt Status Applications and Forms

- California Corporations Code – Nonprofit Legal Framework

- California Attorney General's Registry of Charitable Trusts – Registration Requirements

- IRS Publication 557 – Tax-Exempt Status Guidelines

- National Council of Nonprofits – Formation Best Practices

Sources & References

- California Secretary of State – Official forms, filing procedures, processing timelines, and expedited service options.

- Internal Revenue Service (IRS) – Form 1023, Form 1023-EZ, EIN applications, and tax-exempt determination procedures.

- California Corporations Code – Legal requirements for nonprofit public benefit corporations and ongoing compliance obligations.

- California Attorney General's Registry of Charitable Trusts – Registration requirements and annual reporting guidelines.

- IRS Publication 557 – Comprehensive guidance on tax-exempt status applications and organizational requirements.

- National Council of Nonprofits – Best practices for nonprofit formation, governance, and compliance management.

Disclaimer

This information is provided for educational purposes only and does not constitute legal or tax advice. Nonprofit formation requirements may vary based on organizational structure, activities, and specific circumstances. Consult qualified legal and tax professionals for advice specific to your situation.

Contact

Website:

https://thedocumentpro.com/

Phone: 1 (800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™

A discipline of The Document Pro, operated by Gitta Williams.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Find Us Locally

Service Area: Moreno Valley, CA and surrounding areas

Coordinates: 33.9535, -117.2081

Address: 23945 Sunnymead Blvd. #4, Moreno Valley, CA 92553

Sources

- https://www.irs.gov/charities-non-profits/charitable-organizations

- https://www.irs.gov/forms-pubs/about-form-1023

- https://calnonprofits.org/

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.