16 Jan What Documents Do Funders Commonly Ask for When Reviewing a First-Time Grantee?

Short Answer

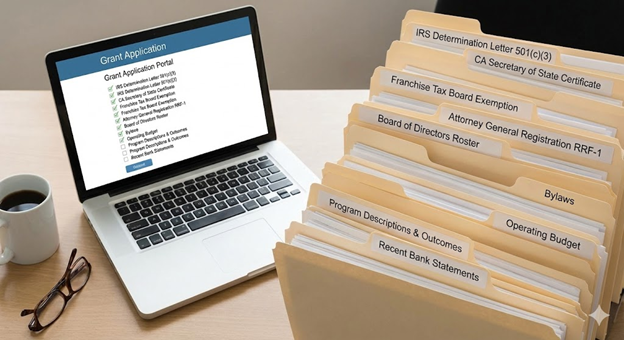

Funders reviewing first-time grantees commonly request federal IRS 501(c)(3) determination letters proving tax-exempt status, recent IRS Form 990 filings showing financial activity and program expenses, organizational bylaws demonstrating governance structure, board of directors roster with names and affiliations, conflict of interest policies proving ethical oversight, operating budgets showing revenue sources and expense allocations, financial statements or bank records demonstrating fiscal capacity, and program descriptions with measurable outcomes showing what the organization actually does and achieves. California funders additionally verify Secretary of State Active status certificates, Franchise Tax Board exemption confirmations, and Attorney General Registry of Charities registration numbers to confirm multi-agency compliance. Eligibility varies by grant, but first-time applicants generally face heightened documentation scrutiny because funders lack relationship history and prior grant performance data to inform risk assessment.

Why do first-time grantees face different documentation expectations than established applicants?

First-time applicants represent unknown quantities to funders who lack performance history, relationship familiarity, or track records demonstrating organizational competence. When funders evaluate repeat applicants, they draw on years of grant reporting, site visits, ongoing communication, and observed program results that provide confidence in the organization’s capacity and integrity. First-time applicants have no such history, requiring funders to establish baseline confidence through documentation review rather than through accumulated relationship knowledge.

Risk assessment drives heightened documentation requirements. Funders releasing money to unknown organizations face risks that recipients will misuse funds, fail to deliver promised programs, lack capacity to manage grants effectively, or present compliance problems that create reputational damage for the funder. Documentation serves as the primary risk mitigation tool—proof of IRS recognition confirms legitimacy, financial records demonstrate fiscal capacity, governance documents show oversight structures, and program documentation reveals organizational competence.

Temecula and Inland Empire first-time applicants should expect longer application processes, more detailed information requests, and potentially lower initial award amounts compared to what established grantees receive. Funders often start new relationships with modest grants that test organizational performance before committing larger amounts. Successfully managing that first grant—delivering promised outcomes, reporting accurately and timely, maintaining compliant operations—establishes the performance history that reduces documentation burden and increases funding access in subsequent cycles.

The transition from first-time applicant to established grantee happens through consistent demonstration of organizational quality. Each successful grant relationship builds funder confidence, reduces perceived risk, and streamlines future documentation requirements. Organizations that maintain excellent governance, deliver strong programs, communicate proactively, and report thoroughly typically find that documentation requests decrease and award amounts increase as the relationship matures and trust develops.

What federal recognition documents do all funders require regardless of prior relationship?

The IRS determination letter stands as the single most universal document requirement across all institutional funders. This letter from the Internal Revenue Service officially confirms your organization’s 501(c)(3) tax-exempt status, specifies your determination date, shows your Employer Identification Number, and indicates your foundation classification (typically public charity rather than private foundation). Funders need this document because it proves contributions to your organization qualify as tax-deductible charitable donations under federal law, a requirement for most institutional grants.

Current IRS TEOS verification supplements or sometimes replaces determination letters as primary federal recognition proof. TEOS (Tax Exempt Organization Search) at apps.irs.gov/app/eos is the IRS database showing organizations with current tax-exempt recognition. Funders increasingly verify applicant status directly through TEOS rather than relying solely on determination letters because TEOS reflects real-time status—organizations can possess old determination letters while having lost recognition through automatic revocation for missed filings. First-time Temecula applicants should provide both the determination letter and recent TEOS printout showing “Eligible to receive tax-deductible contributions” status.

Recent IRS Form 990 filings demonstrate ongoing compliance with federal filing requirements that maintain tax-exempt status. Form 990 (or 990-EZ for smaller organizations, or 990-N for very small ones) provides funders with financial transparency—total revenue by source, expenses by category, program spending percentages, governance practices, compensation information, and narrative descriptions of activities. First-time applicants may only have one or two years of Form 990 history, which funders understand and accept, but having whatever filings you’re required to submit completed and available is essential.

For very new organizations, explaining limited filing history becomes part of the documentation narrative. If you incorporated within the past 12-18 months, you may not have filed your first Form 990 yet because it’s not due until the 15th day of the 5th month after your first fiscal year ends. Funders generally understand new organization timelines, but you should proactively explain your filing status—”We incorporated in March 2024, so our first Form 990 will be filed in August 2025″ provides context that prevents funder confusion about missing documents.

What California-specific compliance documents do regional funders verify?

California Secretary of State documentation proving current “Active” entity status appears on nearly all California funder checklists. This typically takes the form of a certificate of good standing (officially requested from the Secretary of State for a fee) or a business entity search printout showing your nonprofit corporation’s current status, registered agent, and recent Statement of Information filing. California funders verify SOS status because it confirms your nonprofit legally exists as a California corporation and maintains basic structural compliance with state corporate law.

Franchise Tax Board exemption confirmation demonstrates your organization holds California state tax exemption in addition to federal IRS recognition. While qualifying 501(c)(3) organizations are exempt from California’s $800 annual franchise tax, you must still file annual information returns (Form 199 or 199N) to maintain that exemption. Funders may request your FTB exemption letter (Form 3500A issued after IRS determination) or recent Form 199 filing confirmation proving you’re current with state tax obligations and not operating under FTB suspension.

Attorney General Registry of Charities registration documentation confirms your organization is properly registered for charitable fundraising in California. Most nonprofits must register with the AG Registry within 30 days of first receiving assets and file annual renewal reports (RRF-1) thereafter. Funders request your CT number (Charity Trust registration number) from initial registration or your most recent RRF-1 confirmation. Some funders verify your AG Registry status independently through the online search at oag.ca.gov/charities, but providing documentation proactively demonstrates compliance awareness.

The California three-agency verification pattern—Secretary of State, Franchise Tax Board, Attorney General Registry—distinguishes California from most other states with simpler nonprofit oversight. First-time applicants in Temecula pursuing funding from California-based foundations, corporate giving programs, or government grants should expect verification across all three state agencies plus federal IRS recognition, creating a four-point compliance documentation requirement that national applicants in other states don’t typically encounter.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

The Nonprofit Launch Office operates within a strategic framework designed to help California nonprofits move from formation to fundability:

Launch includes establishing the documentation systems that first-time grant applications will require. Launch-phase organizations should create central files—digital and physical—containing all governance documents, compliance proofs, financial records, and program descriptions that funders commonly request. Building these systems during formation rather than scrambling during first application deadlines creates significant competitive advantage. Launch means having documentation ready before you need it rather than discovering gaps under deadline pressure.

Fix addresses situations where first-time applicants discover during application processes that they’re missing critical documents or have compliance gaps funders verify. Common Fix scenarios include realizing your IRS determination letter was lost and needs replacement (requesting Form 4506-A), discovering you’re suspended by Franchise Tax Board and need urgent restoration, finding that you never registered with Attorney General Registry despite being required to, or identifying that governance documents like bylaws or conflict policies were never formally adopted. Fix work during first grant applications creates stress and often results in missed deadlines.

Fund represents the operational state where documentation systems remain current without crisis management. Fund-phase organizations maintain updated board rosters as membership changes, refresh financial statements quarterly, file compliance renewals before deadlines, and update program descriptions as services evolve. This continuous maintenance means first-time grant applications and subsequent applications both access current, organized documentation rather than outdated or missing materials.

Federal Recognition through IRS 501(c)(3) determination provides the foundation document that appears in virtually every first-time grant application. Organizations lacking federal recognition cannot access most institutional funding regardless of how strong their programs are or how urgent community needs are. The determination letter and TEOS verification prove federal recognition to funders conducting due diligence on unknown applicants.

CA Compliance Triangle represents California’s three-agency state verification system that first-time applicants must satisfy alongside federal recognition. Temecula nonprofits applying to California-based funders need simultaneous current standing with Secretary of State (Active status), Franchise Tax Board (exemption without suspension), and Attorney General Registry (current registration). Being compliant with two out of three creates application rejections just as surely as being compliant with none.

Step-by-step: How NPLO helps first-time applicants organize documentation

Step 1: Documentation Inventory and Gap Analysis We assess what documents you currently have organized versus what first-time grant applications typically require. This inventory reveals which items you possess and can easily access, which items exist but need organizing or updating, and which items are missing entirely and need creation or procurement. The gap analysis prioritizes which missing documents represent urgent needs versus nice-to-have additions.

Step 2: Federal Recognition Verification and Organization We locate your IRS determination letter (or help request replacement if lost), generate current TEOS printout showing your active tax-exempt status, organize recent Form 990 filings or explain filing timeline if you’re too new to have filed yet, and prepare narrative explaining your federal recognition history for funders. This federal documentation package addresses the baseline requirement nearly all funders verify.

Step 3: California Multi-Agency Compliance Documentation We obtain Secretary of State certificate of good standing or business entity search printout showing Active status, gather Franchise Tax Board exemption confirmation and recent Form 199 filing, compile Attorney General Registry CT number and current RRF-1 confirmation, and verify that all three California agencies show current compliance without suspensions or delinquencies. This three-agency package satisfies California funder verification requirements.

Step 4: Governance Document Assembly We organize or help create the governance documents funders request—formally adopted bylaws with board approval date, comprehensive board roster with complete contact information and terms, conflict of interest policy with signed annual disclosure forms, recent board meeting minutes demonstrating active oversight, and any other governance policies your organization has established. These documents prove functional organizational structure to skeptical reviewers.

Step 5: Financial Documentation Preparation We compile financial records funders commonly request—operating budget for current fiscal year showing revenue sources and expense categories, recent financial statements or bank statements demonstrating fiscal capacity, Form 990 analysis highlighting program expenses and fundraising efficiency, financial policies addressing fund management and internal controls, and explanations for any financial patterns that might raise funder questions.

Step 6: Program Documentation Development We help articulate program descriptions, measurable outcomes, service statistics, and community impact narratives that appear throughout grant applications. For first-time applicants with limited formal evaluation data, we develop frameworks for documenting outcomes going forward and present available evidence of effectiveness—participant testimonials, preliminary outcome measurements, partnership letters, or community needs documentation supporting your program approach.

Step 7: Master Documentation Folder Creation We organize all compliance proofs, governance documents, financial records, and program materials into a systematic master folder—digital files with clear naming conventions, physical binder for board reference and backup, quick-access organization matching common funder request patterns, and master index showing what’s available and when each document was last updated. This organized system accelerates application completion.

Step 8: Application-Specific Document Customization When you identify specific grant opportunities, we review the application requirements and customize your master documentation to match funder requests—adapting program descriptions to match word count limits and focus areas, highlighting budget elements most relevant to that funder’s priorities, and selecting governance or financial documents most responsive to their specific requirements. Customization from organized master files is far faster than creating documents from scratch under deadline.

Checklist: What you should have ready for first-time grant applications

First-time grant applicants in Temecula and the Inland Empire should maintain organized access to these commonly requested documents:

- IRS determination letter showing 501(c)(3) recognition with your current legal name, EIN, and determination date clearly visible

- IRS TEOS printout from apps.irs.gov/app/eos showing your organization currently listed with “Eligible to receive tax-deductible contributions” status

- Most recent IRS Form 990, 990-EZ, or 990-N demonstrating federal filing compliance (or explanation of filing timeline if too new)

- California Secretary of State certificate of good standing or business entity search showing “Active” status

- Current Statement of Information confirmation from Secretary of State showing biennial filing within past two years

- Franchise Tax Board exemption letter (Form 3500A) and most recent Form 199 or 199N filing

- Attorney General Registry CT number and most recent RRF-1 (Registry Renewal Fee Report) confirmation

- Formally adopted bylaws with board approval date and any amendment history documented

- Current board of directors roster listing all members with names, affiliations, contact information, term dates, and committee assignments

- Conflict of interest policy with annual disclosure forms signed by all board members and key staff

- Board meeting minutes from organizational meeting and recent regular meetings showing active governance

- Operating budget for current fiscal year detailing anticipated revenue sources and planned expenses by program and administration

- Financial statements showing recent activity (bank statements minimum; audited financials for larger organizations)

- Financial policies addressing approval authorities, fund management, expense reimbursement, and internal controls

- Program descriptions for each major activity area with target populations, service geography, and intended outcomes

- Outcome measurement framework showing how you track program effectiveness and impact

- Service statistics documenting how many people you serve, what activities you provide, and what results you achieve

- Letters of support from community partners, beneficiaries, or stakeholders attesting to your work’s value and impact

- Insurance certificates showing general liability coverage and directors & officers liability if applicable

- Registered agent documentation showing current agent authorization and contact information for legal service

Quick Answers (PPA)

What if I’m asked for documents I don’t have because we’re a very new organization? Funders generally understand that brand new organizations have limited documentation history—you can’t provide three years of Form 990 filings if you’ve only existed 18 months. The key is being transparent and proactive: explain your organizational age, provide whatever documentation your current stage allows, demonstrate that you’re establishing proper systems going forward, and show that you understand what mature organizations maintain even if you don’t have years of history yet. Many funders specifically target emerging organizations and design eligibility criteria accommodating new nonprofits. Being new isn’t disqualifying—lacking awareness of what you should be building toward is.

Do I need audited financial statements for my first grant application? Most first-time grant applications don’t require audited financial statements unless the grant amount is substantial (typically $250,000+) or the funder has specific audit requirements. Smaller first-time applicants usually satisfy financial documentation requirements with Form 990 filings, operating budgets, and bank statements or internally prepared financial statements. However, as your organization grows and pursues larger grants, some funders will eventually require audited financials. Review each funder’s specific requirements—don’t assume you need expensive audits for every application, but don’t ignore audit requirements when they’re explicitly stated.

How many years of Form 990 filings do funders expect from first-time applicants? Funders generally expect whatever Form 990 history your organization’s age allows. If you’re in your second year of operations, having one Form 990 on file is normal and acceptable. If you’ve existed five years but haven’t filed Form 990s, that’s a serious compliance problem raising red flags. First-time applicants should provide all Form 990s they’ve been required to file, even if that’s only one or two years of history. Funders understand limited filing history for genuinely new organizations but view missing required filings as evidence of poor governance and compliance management.

Can I use the same documents for all grant applications or do I need to customize everything? Core documents like IRS determination letters, bylaws, board rosters, and Form 990s are universal—you’ll provide identical versions to all funders. However, program descriptions, budgets, and outcome narratives typically need customization to match each funder’s specific focus areas, word count limits, and format requirements. Maintain master versions of customizable documents that you can adapt quickly rather than starting from scratch for each application. The organized documentation folder approach allows you to have both universal documents ready and flexible templates that customize efficiently.

What if I discover missing documents or compliance gaps while working on my first grant application? Address problems immediately rather than hoping funders won’t notice or trying to submit incomplete applications. If you’re missing required compliance filings, start the process to file them before submitting the application—many funders accept evidence of filing in progress for first-time applicants establishing systems. If governance documents were never formally adopted, have an emergency board meeting to rectify this before the application deadline. If compliance restoration takes longer than the application timeline allows, consider focusing on different funders with later deadlines while you fix problems, rather than submitting applications you know will be rejected for eligibility issues.

What to do next (DIY vs Done-With-You)

DIY approach: Create a comprehensive documentation checklist by reviewing application guidelines from 3-5 funders you plan to approach and noting every document requested across those applications. Compile a master list of unique documents rather than duplicates. Systematically gather or create each document on your list—start with federal recognition documents (determination letter, TEOS printout, Form 990s), then move to California compliance proofs (SOS, FTB, AG Registry), then governance documents (bylaws, board roster, conflict policy, minutes), then financial materials (budget, statements, policies), then program documentation (descriptions, outcomes, statistics). Organize everything in a digital folder with clear file names like “IRS_Determination_Letter_2023.pdf” or “Board_Roster_Current_2025Q1.pdf” and create a physical binder backup. Build a master index document listing every item in your documentation folder with last update dates. Set quarterly calendar reminders to review and update time-sensitive documents like board rosters, budgets, and financial statements.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive first-time grantee documentation preparation for Temecula and Inland Empire nonprofits. We conduct detailed documentation inventories identifying exactly what you have versus what applications require, verify and organize federal recognition documents including determination letters and TEOS verification, compile California three-agency compliance documentation proving good standing across SOS, FTB, and AG Registry, create or formalize governance documents meeting institutional funder expectations, organize financial records into funder-friendly formats with appropriate narratives, develop program descriptions and outcome frameworks translating your work into grant language, assemble master documentation folders with systematic organization and version control, and provide application-specific customization support when you target particular opportunities. This preparation work transforms first-time applications from overwhelming documentation hunts into manageable processes where you focus on program narrative rather than scrambling for proof of legitimacy.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Sources

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.