19 Jan What Should a Nonprofit’s Purpose Statement Include at a High Level?

Short Answer

A nonprofit’s purpose statement should include specific charitable purposes qualifying under IRS Section 501(c)(3) (education, poverty relief, community development, health services, etc.), clearly identified target populations or communities served with enough specificity to demonstrate focus without overly limiting future flexibility, concrete descriptions of primary activities or programs the organization conducts to achieve its charitable purposes, and intended outcomes or community benefits that result from the organization’s work. Eligibility varies by organization, but effective purpose statements avoid vague generalities like “helping people” or “making the world better” in favor of precise language that satisfies IRS requirements, appears in Articles of Incorporation and determination applications, guides board governance and program decisions, and communicates organizational identity to funders, donors, and community stakeholders throughout the nonprofit’s existence.

What are the core elements every purpose statement must contain?

Charitable purpose classification under IRS Section 501(c)(3) represents the foundational element determining whether your organization qualifies for tax-exempt status. The IRS recognizes specific categories of charitable purposes: relief of poverty, advancement of education, advancement of religion, promotion of health, governmental or municipal purposes, lessening neighborhood tensions, eliminating prejudice and discrimination, defending human and civil rights, and combating community deterioration. Your purpose statement must clearly fall within one or more of these recognized categories—”we do good work in the community” doesn’t specify a recognized charitable purpose, while “we provide literacy tutoring to low-income adults” clearly advances education while relieving poverty.

Target population or community identification demonstrates organizational focus and helps establish public benefit rather than private interest. Effective purpose statements specify who benefits from the organization’s work with enough detail to communicate focus—”youth ages 14-18 in Riverside County,” “homeless veterans in the Inland Empire,” “seniors experiencing food insecurity,” “immigrant families seeking legal services.” However, purpose statements should avoid such narrow specificity that they limit organizational flexibility—”students at Riverside High School graduating in 2025″ creates problems if you want to serve students at other schools or in different years. The balance involves being specific enough to demonstrate genuine charitable focus while broad enough to allow reasonable program evolution.

Primary activities or methods describing how the organization achieves its charitable purposes transform abstract goals into concrete operational plans. Rather than stating only “we serve homeless individuals” (target population), effective purpose statements add “through emergency shelter provision, case management, employment readiness training, and housing placement assistance” (specific activities). This activity description helps IRS evaluators understand what your nonprofit actually does, prevents confusion about organizational operations, and provides accountability framework ensuring activities remain aligned with stated charitable purposes.

Intended outcomes or community benefits articulate why the organization’s work matters and what change it seeks to create. Purpose statements might reference “enabling participants to achieve economic self-sufficiency,” “improving academic performance and graduation rates,” “reducing food insecurity,” or “increasing civic participation among underserved communities.” While outcomes shouldn’t promise unrealistic guarantees (“we will eliminate homelessness”), they should describe the positive community impact the organization pursues through its charitable activities.

How should purpose statements balance specificity with flexibility?

Overly specific purpose statements create operational constraints that become problematic as organizations evolve. If your Articles of Incorporation state “we provide after-school tutoring in mathematics to 6th grade students at Lincoln Elementary School,” you’ve locked yourself into serving only that grade level, only that subject, only that school, and only through after-school timing. Expanding to serve 7th graders, adding reading tutoring, serving students at other schools, or offering weekend programs would technically require amending your Articles of Incorporation—an expensive, time-consuming process requiring Secretary of State filing and potential IRS notification. Many Temecula nonprofits discover years later that overly narrow original purpose statements constrain their ability to adapt programs based on community needs, evaluation findings, or funding opportunities.

Overly broad purpose statements create different problems by failing to demonstrate focused charitable purpose or raising IRS concerns about organizational mission clarity. Purpose statements like “improving the quality of life for all people” or “addressing social problems” are so vague they don’t meaningfully communicate what the organization does, don’t help IRS evaluators determine whether activities qualify as charitable, and don’t provide governance boundaries ensuring the board maintains mission focus. Broad statements also create credibility problems with funders who question whether organizations pursuing everything effectively accomplish anything.

The strategic middle ground involves specific-enough-to-be-meaningful language that preserves reasonable flexibility for program evolution. Consider: “We advance education and relieve poverty by providing literacy training, workforce development, and economic empowerment programs for low-income adults in Riverside County.” This statement specifies charitable purposes (education, poverty relief), describes activity categories (literacy, workforce development, economic empowerment), identifies target population (low-income adults), and indicates geographic focus (Riverside County)—while remaining flexible about specific program models, particular curricula, exact age ranges, or precise service locations within the county.

Purpose statement refinement over organizational life stages often proves necessary as nonprofits mature, programs evolve, or community needs shift. While amending Articles of Incorporation requires formal processes, most organizations can adjust program emphasis, service models, or activity details through board policy decisions without Articles amendments—as long as changes remain consistent with the general charitable purposes stated in formation documents. The initial purpose statement should be specific enough for IRS approval and meaningful board governance while broad enough to accommodate reasonable adaptation without requiring Articles amendments every few years.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

The Nonprofit Launch Office operates within a strategic framework designed to help California nonprofits move from formation to fundability:

Launch includes developing purpose statements during the formation phase that will appear in California Articles of Incorporation, IRS Form 1023 applications, grant proposals, and organizational communications throughout your existence. Purpose statement quality during Launch determines whether you achieve smooth IRS approval or face questions requiring supplemental submissions, whether your Articles of Incorporation provide appropriate operational flexibility or create constraints requiring later amendments, and whether board members and stakeholders clearly understand organizational mission or operate with confusion about focus and boundaries. Getting purpose statements right during Launch prevents Fix needs later.

Fix addresses situations where original purpose statements were problematic—too vague to satisfy IRS requirements requiring supplemental clarification, too narrow constraining current operations requiring Articles amendments to expand scope, misaligned with actual activities raising IRS concerns about mission consistency, or written in language that confuses rather than clarifies organizational identity. Fix work involving purpose statement problems often requires amending California Articles of Incorporation (Secretary of State filing plus fees), notifying IRS of significant organizational changes, revising grant applications and communications using outdated language, and managing stakeholder confusion about organizational identity shifts.

Fund depends partly on clear purpose statements that communicate organizational focus to funders evaluating whether your mission aligns with their priorities. Grant applications universally request organizational mission or purpose statements, and funders use this language to determine program fit with their funding focus areas. Vague or confusing purpose statements weaken grant applications because reviewers cannot confidently assess mission alignment. Clear, compelling purpose statements strengthen applications by immediately communicating what you do, who you serve, and what change you seek—helping funders understand within seconds whether your work matches their priorities.

Federal Recognition through IRS 501(c)(3) determination depends fundamentally on demonstrating that your stated purpose qualifies as charitable under Section 501(c)(3) and that your planned activities advance that charitable purpose rather than serving private interests. The IRS examines purpose statements in Articles of Incorporation and Form 1023 applications closely, requesting clarification when language is vague or concerning when activities don’t clearly support stated purposes. Purpose statements using recognized IRS terminology and clearly describing charitable activities strengthen applications and streamline approval processes.

CA Compliance Triangle (Secretary of State, Franchise Tax Board, Attorney General Registry) all reference the charitable purpose established in your Articles of Incorporation. When registering with Attorney General Registry of Charities, you must describe organizational purpose and activities—language should align with what appears in your Articles and IRS determination. Inconsistencies between purpose statements in different documents raise compliance questions and suggest poor organizational coordination or potential mission drift from originally approved charitable purposes.

Step-by-step: How NPLO helps organizations develop effective purpose statements

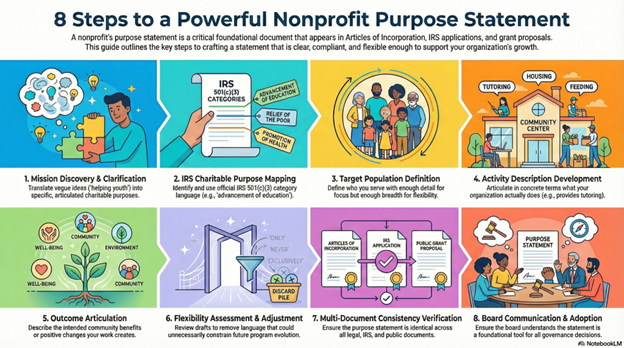

Step 1: Mission Discovery and Clarification We facilitate conversations with founding teams exploring what problem you’re addressing, why it matters to your community, who specifically needs your services, what approaches you’ll use, and what change you seek to create. These discovery conversations often reveal that initial vague ideas (“we want to help youth”) contain more specific charitable purposes when properly articulated (“we advance education and prevent juvenile delinquency by providing academic tutoring and positive mentoring relationships for at-risk youth in Temecula”).

Step 2: IRS Charitable Purpose Mapping We help identify which recognized 501(c)(3) charitable purpose categories your work fits within—education, poverty relief, health promotion, etc.—and use IRS-friendly terminology that strengthens determination applications. Many founders describe their work in community language that doesn’t clearly map to IRS categories; we translate community language into regulatory language that satisfies IRS requirements while remaining authentic to organizational identity.

Step 3: Target Population Definition We help define who you serve with appropriate specificity—specific enough to demonstrate focused charitable purpose, broad enough to allow reasonable program flexibility. This includes considering geographic boundaries (Temecula, Riverside County, Inland Empire), demographic characteristics (age ranges, income levels, specific populations), and eligibility criteria (homeless, formerly incarcerated, immigrant, etc.) that focus your work without unnecessarily constraining it.

Step 4: Activity Description Development We help articulate what your organization actually does in concrete terms—providing services, conducting education, distributing resources, advocating for policy changes, building community capacity—in language that clearly advances your charitable purposes. Activity descriptions should be specific enough that IRS evaluators understand your operations while flexible enough to accommodate program model evolution.

Step 5: Outcome Articulation We help describe intended community benefits or changes your work pursues—educational attainment, economic self-sufficiency, health improvement, community development—that demonstrate charitable impact. Outcome language should be aspirational without promising unrealistic guarantees, results-oriented without requiring specific quantified metrics that might become outdated.

Step 6: Flexibility Assessment and Adjustment We review draft purpose statements for appropriate flexibility, identifying language that might unnecessarily constrain future program evolution and suggesting broader formulations that preserve mission focus while allowing adaptation. This assessment prevents the common problem where organizations outgrow overly narrow original purpose statements and face expensive Articles amendments.

Step 7: Multi-Document Consistency Verification We ensure purpose statement language appears consistently across Articles of Incorporation (exact legal language), IRS Form 1023 applications (detailed narrative), bylaws (mission section), and organizational communications (public-facing descriptions). Consistency across documents prevents confusion and demonstrates organizational coherence to regulators and funders.

Step 8: Board Communication and Adoption We help founding boards understand the purpose statement’s significance—it’s not just bureaucratic language for formation documents but foundational guidance for all future governance decisions about program development, funding priorities, partnership opportunities, and organizational boundaries. Board adoption of purpose statements should involve genuine discussion and understanding rather than rubber-stamping language they haven’t considered.

Checklist: What your purpose statement should communicate

Effective nonprofit purpose statements for Temecula organizations should clearly convey:

- Recognized charitable classification falling within IRS Section 501(c)(3) categories (education, poverty relief, health, etc.)

- Specific target population identifying who benefits from organizational work with appropriate demographic, geographic, or situational specificity

- Primary activity categories describing what the organization does in concrete operational terms (providing services, conducting education, distributing resources, etc.)

- Intended outcomes or benefits articulating what positive change or community impact the organization pursues through its activities

- Geographic scope indicating service area (Temecula, Riverside County, Inland Empire, California, or broader) appropriate to operational reality and funding sources

- Sufficient specificity to demonstrate focused charitable purpose and guide board governance decisions about program priorities and boundaries

- Adequate flexibility to accommodate reasonable program evolution, service model adaptation, and response to changing community needs without requiring Articles amendments

- IRS-compliant language using terminology recognized in charitable organization regulations and determination precedents

- Clarity and accessibility written in language stakeholders, funders, and community members can understand without regulatory expertise

- Consistency across documents matching language in Articles of Incorporation, IRS applications, bylaws, grant proposals, and public communications

- Authenticity to organizational identity reflecting genuine mission and values rather than generic template language

- Distinction from for-profit purposes clearly pursuing public benefit rather than private commercial interests or individual profit

- Exclusivity of charitable purpose demonstrating that all substantial activities advance charitable purposes rather than mixing charitable and non-charitable goals

- Permanence and commitment conveying that the organization pursues its charitable purposes consistently and sustainably rather than as temporary or occasional efforts

Quick Answers (PPA)

Can we change our purpose statement later if our programs evolve, or are we locked in forever? You can change purpose statements, but the process and implications depend on the significance of the change. Minor refinements or clarifications to how you describe work within your existing charitable purpose typically require only updating marketing materials, grant applications, and internal documents without formal Articles amendments. Substantial changes adding new charitable purpose categories, significantly expanding target populations, or fundamentally shifting organizational focus generally require amending California Articles of Incorporation (Secretary of State filing plus fees) and potentially notifying the IRS if changes affect your tax-exempt status basis. The IRS wants consistency between your stated purpose and actual operations, so significant mission drift without formal amendments raises red flags during audits or Form 990 reviews. The strategic approach involves crafting initial purpose statements with enough breadth to accommodate reasonable program evolution without needing frequent amendments.

How detailed should the purpose statement in Articles of Incorporation be compared to what we use in grant applications? Articles of Incorporation purpose statements should be moderately detailed—specific enough to clearly establish charitable purpose and guide operations, but not so detailed that minor program changes require amendments. Many California nonprofits use 2-4 sentence purpose statements in Articles capturing charitable categories, target populations, primary activities, and geographic scope at a relatively high level. Grant application purpose statements can and should be more detailed, elaborating on specific program models, particular service approaches, outcome measurements, and organizational history that provides context—often expanding to full paragraphs or pages depending on application requirements. The key is ensuring grant application language remains consistent with and clearly derives from the broader purpose stated in Articles, demonstrating faithful adherence to your chartered mission rather than suggesting mission drift or activities beyond your legal authorization.

Should we include specific programs or services by name in our purpose statement? Generally no—specific program names shouldn’t appear in Articles of Incorporation purpose statements because programs evolve, get renamed, end, or expand in ways that would make naming them in permanent formation documents constraining. Instead, describe program categories or activity types at a conceptual level. Rather than “we operate the Summer Youth Leadership Academy,” state “we provide leadership development and educational enrichment programs for youth.” This approach allows ending, renaming, or expanding the specific academy program without Articles amendments while maintaining alignment with your stated purpose of youth development and education. Save specific program names and detailed descriptions for operational documents, grant applications, and marketing materials that can be updated easily as programs evolve.

What if we want to serve multiple different populations or pursue several charitable purposes—can one purpose statement cover everything? Yes, purpose statements can and often should cover multiple charitable purposes or populations when organizations legitimately work in several areas, but should avoid becoming so comprehensive that they lack meaningful focus. For example: “We advance education, promote health, and relieve poverty by providing integrated services including academic tutoring, health education, nutritious food distribution, and economic empowerment programs for low-income families in Riverside County.” This statement covers multiple charitable purposes (education, health, poverty) with multiple activities serving a defined population. However, be cautious about “kitchen sink” purpose statements listing ten charitable categories and twenty activities—this suggests lack of focus and raises IRS questions about organizational clarity. Most effective purpose statements cover 1-3 primary charitable purposes with 2-5 major activity categories, demonstrating focused mission while preserving reasonable flexibility.

Does the purpose statement need to mention anything about tax-exempt status or that we’re a nonprofit organization? Purpose statements should focus on charitable purposes and activities rather than tax status or corporate structure. The charitable purpose itself is what qualifies you for tax exemption—”we advance education” is the relevant content, not “we are a tax-exempt educational organization.” However, California Articles of Incorporation must include specific required language elsewhere in the document (not necessarily in the purpose statement itself) stating that the corporation is organized under Nonprofit Public Benefit Corporation Law, that it’s organized exclusively for charitable purposes under 501(c)(3), and including the required dissolution clause specifying that assets will go to other 501(c)(3) organizations upon dissolution. These structural provisions appear in separate articles from the purpose statement but are equally mandatory for formation and IRS recognition.

What to do next (DIY vs Done-With-You)

DIY approach: Begin developing your purpose statement by free-writing answers to core questions: What specific community problem does your organization address? Who specifically experiences this problem and needs your services? What concrete activities will your organization conduct to address the problem? What positive changes or outcomes do you hope to create? What geographic area do you serve? Review your answers and identify which IRS charitable purpose categories your work fits within—education, poverty relief, health, community development, etc. Research how similar organizations in your field describe their purposes by reviewing their websites, IRS Form 990 filings (public on GuideStar/Candid), and grant materials. Draft purpose statement language combining charitable purpose classification, target population, primary activities, and intended outcomes in 2-4 clear sentences. Test your draft by asking: Is it specific enough that someone unfamiliar with your work understands what you do? Is it flexible enough to accommodate reasonable program evolution? Does it use recognized IRS charitable terminology? Could board members use this statement to guide decisions about whether new opportunities align with mission? Revise based on these questions. Review IRS Publication 557 examples of acceptable purpose statements. Consider having attorneys or nonprofit consultants review your draft before filing in Articles of Incorporation.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive purpose statement development for Temecula and Inland Empire organizations, ensuring language satisfies IRS requirements while preserving operational flexibility and communicating organizational identity effectively. We facilitate mission discovery conversations that clarify what community need you address, who you serve, what activities you conduct, and what outcomes you pursue, translating initial ideas into focused charitable purposes. We map your work to recognized IRS charitable purpose categories using regulatory-friendly terminology that strengthens determination applications. We help define target populations with appropriate specificity that demonstrates focus without constraining reasonable expansion. We develop activity descriptions that clearly convey operational plans while allowing program model evolution. We craft outcome statements that communicate intended impact without unrealistic promises. We review draft language for flexibility, identifying constraints that might require expensive later amendments. We ensure consistency across Articles of Incorporation, IRS Form 1023, bylaws, and organizational communications. We prepare board members to understand purpose statements as governance tools rather than just bureaucratic requirements. This comprehensive approach delivers purpose statements that satisfy regulatory requirements, guide effective governance, communicate clearly to stakeholders, and position organizations for grant success while preserving appropriate operational flexibility.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Sources

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.