09 Feb What Does It Mean to Maintain Federal Compliance After Approval?

Short Answer

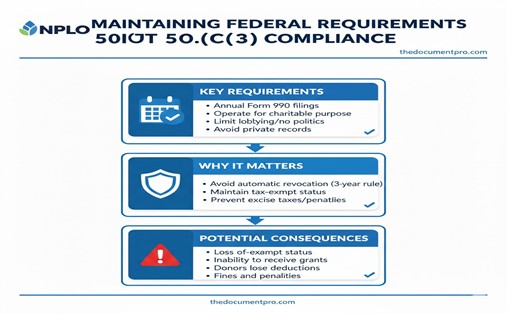

Maintaining federal compliance after IRS 501(c)(3) approval means filing required annual information returns (Form 990, 990-EZ, or 990-N) by deadlines, continuing to operate exclusively for approved charitable purposes without substantial changes to mission or activities, avoiding prohibited political campaign intervention and limiting lobbying to insubstantial amounts, preventing private inurement where net earnings benefit insiders beyond reasonable compensation, and preserving organizational documents including meeting minutes, financial records, and governance policies. Ongoing compliance matters because failure to file Form 990 for three consecutive years triggers automatic revocation of tax-exempt status, substantial deviation from approved charitable purposes can result in IRS determination that the organization no longer qualifies for exemption, and violations of prohibited activity rules (political campaigns, excess private benefit, unrelated business income) can lead to excise taxes or complete loss of recognition.

What annual filing requirements must organizations meet?

Form 990 series annual information returns report organizational finances and activities to IRS. Organizations with gross receipts over $200,000 or assets over $500,000 file full Form 990. Organizations with gross receipts under $200,000 and assets under $500,000 file Form 990-EZ. Organizations with gross receipts normally $50,000 or less file Form 990-N (e-Postcard). These returns are due by the 15th day of the 5th month after fiscal year end (May 15 for calendar-year organizations).

Filing deadline compliance prevents automatic revocation. Organizations missing Form 990 filings for three consecutive years automatically lose tax-exempt status without further IRS notice. The organization disappears from TEOS database showing revoked status, donors can no longer deduct contributions, and the organization must apply for reinstatement to restore recognition. Missing one year doesn’t trigger revocation, but starting the three-year countdown toward automatic loss of exemption.

Extensions provide additional filing time when needed. Organizations unable to complete Form 990 by the regular deadline can file Form 8868 requesting automatic six-month extension (extending deadline to November 15 for calendar-year organizations). Extensions prevent late filing penalties but don’t extend payment deadlines for any taxes owed. Filing extension requests demonstrates good faith compliance even when circumstances prevent timely completion.

Accuracy and completeness matter beyond just meeting deadlines. Form 990 is a public document that funders, media, watchdog organizations, and community members review. Incomplete forms with missing schedules, inconsistent data, or obvious errors create credibility problems. Answers to governance questions about conflict policies, board meeting frequency, and document availability signal organizational quality to sophisticated reviewers.

What operational compliance requirements continue after approval?

Exclusive charitable purpose operation must continue. The IRS granted exemption based on organizational purposes and planned activities described in Form 1023/1023-EZ applications. Substantial changes to purposes or activities—adding major new program areas not described in applications, fundamentally shifting who you serve, or conducting activities outside approved charitable categories—should be disclosed to IRS through amended applications or supplemental correspondence. Organizations operating significantly differently from what IRS approved risk determination that exemption was granted based on incorrect information.

Political campaign intervention remains absolutely prohibited. Tax-exempt 501(c)(3) organizations cannot participate in or intervene in political campaigns supporting or opposing candidates for public office. This includes making contributions to campaigns, endorsing candidates in organizational capacity, distributing campaign materials, or allowing organizational resources to be used for campaign purposes. Any amount of campaign intervention jeopardizes exemption—there’s no de minimis exception. Issue advocacy and nonpartisan voter education are permitted with careful structuring.

Lobbying limitations require monitoring. While campaign intervention is completely prohibited, lobbying (attempting to influence legislation) is permitted as long as it doesn’t constitute a substantial part of activities. Most organizations interpret “substantial” as less than 5-10% of time and resources. Organizations can elect to measure lobbying under Section 501(h) expenditure test providing more precise limits. Exceeding substantial lobbying limits can result in excise taxes or exemption loss.

Private inurement and excess benefit prevention continues. No part of net earnings can benefit private individuals including founders, board members, substantial contributors, or their families beyond reasonable compensation for actual services rendered. Organizations must maintain conflict of interest procedures, ensure compensation decisions receive independent review based on comparability data, and avoid self-dealing transactions benefiting insiders. Excess benefit transactions trigger excise taxes on recipients and approving managers even without exemption revocation.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

Launch includes establishing systems ensuring ongoing compliance from inception. Riverside nonprofits should create Form 990 filing calendars, implement governance practices supporting compliance, and establish recordkeeping systems preserving required documentation before compliance failures occur.

Fix becomes necessary when organizations missed Form 990 filings triggering automatic revocation, conducted prohibited activities requiring correction and potential penalty payment, or discovered operations drifted substantially from IRS-approved purposes requiring amended applications or operational corrections.

Fund depends on maintaining compliance because funders verify current tax-exempt status through TEOS database before awarding grants. Organizations showing revoked status due to missed filings cannot receive grants until status is restored. Organizations with compliance problems face funder skepticism even after correction.

Federal Recognition isn’t a one-time achievement but ongoing status maintained through continuous compliance. The determination letter proves recognition was granted, but maintaining recognition requires meeting annual filing requirements and operational standards indefinitely.

CA Compliance Triangle operates parallel to federal compliance. Organizations must maintain both IRS federal compliance AND California Secretary of State, Franchise Tax Board, and Attorney General compliance simultaneously—success in one doesn’t compensate for failure in others.

Step-by-step: How NPLO helps organizations maintain federal compliance

Step 1: Filing Calendar Creation We establish comprehensive calendars showing Form 990 deadlines with advance reminders preventing missed filings.

Step 2: Annual Filing Preparation We prepare accurate complete Form 990/990-EZ/990-N returns reflecting organizational activities and finances.

Step 3: Governance Documentation We ensure boards maintain meeting minutes, policies, and records supporting Form 990 governance responses.

Step 4: Activity Monitoring We help organizations evaluate whether programs remain consistent with IRS-approved purposes or require notification.

Step 5: Political Activity Guidance We provide clear guidance preventing prohibited campaign intervention while allowing permitted issue advocacy.

Step 6: Compensation Review We establish procedures ensuring insider compensation receives independent review with comparability documentation.

Step 7: TEOS Verification We monitor TEOS database quarterly ensuring organizations show current active status without revocation flags.

Step 8: Corrective Action When compliance problems emerge, we guide remediation including delinquent filing, penalty abatement, or reinstatement applications.

Checklist: Federal compliance requirements

Annual Filing Requirements:

- File Form 990/990-EZ/990-N by deadline

- Choose correct form based on revenue thresholds

- Complete all required schedules

- Provide accurate financial information

- Answer governance questions honestly

- File extension (Form 8868) if needed

- Maintain copies of filed returns

Operational Requirements:

- Continue operating for approved charitable purposes

- Avoid substantial mission or activity changes without IRS notification

- Maintain charitable purpose exclusivity

- Document all programs and activities

- Ensure activities advance exempt purposes

Prohibited Activity Avoidance:

- No political campaign intervention (zero tolerance)

- Limit lobbying to insubstantial amounts

- No private inurement to insiders

- Prevent excess benefit transactions

- Avoid unrelated business income or pay UBIT on it

Governance and Documentation:

- Hold regular board meetings

- Maintain meeting minutes

- Preserve financial records (7 years minimum)

- Keep organizational documents accessible

- Update policies as needed

- Ensure conflict procedures are followed

Public Disclosure:

- Make Form 990 available on request

- Provide determination letter when requested

- Maintain TEOS database listing accuracy

Quick Answers (PPA)

What happens if we miss our Form 990 deadline—is there a grace period or penalty? Organizations missing deadlines can file late returns preventing the three-year countdown toward automatic revocation, though late filing penalties may apply ($20 per day up to $10,000 for small organizations, higher for large organizations). File immediately upon discovering missed deadline—late filing is far better than not filing. If you missed one year, file that delinquent return now before missing a second year. If you missed two consecutive years, file both immediately before the third-year deadline preventing automatic revocation. While penalties exist, reinstatement after revocation is far more expensive and time-consuming than paying late filing penalties.

Can we change our programs and activities after IRS approval, or are we locked into what we initially described? Organizations can and should evolve programs as community needs change, as long as modifications remain within approved charitable purposes and don’t constitute substantial organizational changes. Adding a new tutoring program when approved purposes include education doesn’t require IRS notification. Completely shifting from education mission to healthcare mission requires substantial explanation to IRS. The test is whether changes are reasonable program evolution within existing exempt purposes versus fundamental mission shifts requiring amended applications. When uncertain, consult tax professionals about whether contemplated changes require IRS notification.

What’s the difference between lobbying (which is allowed with limits) and political activity (which is prohibited)? Lobbying is attempting to influence legislation—contacting legislators about pending bills, encouraging public to contact legislators, or taking positions on specific legislation. This is permitted as long as not substantial (typically interpreted as under 5-10% of activities). Political campaign intervention is participating in campaigns for or against candidates for public office—endorsing candidates, contributing to campaigns, distributing campaign literature, allowing candidates to use organizational resources. This is absolutely prohibited with zero tolerance—any amount jeopardizes exemption. Organizations can engage in issue advocacy and nonpartisan activities without violating either restriction with careful structuring.

If we have conflicts of interest, does that automatically violate compliance, or is it okay as long as we follow our conflict policy? Having conflicts doesn’t violate compliance—conflicts are unavoidable when board members have business relationships, family connections, or financial interests that intersect with organizational activities. What matters is how conflicts are managed. Organizations must have conflict of interest policies requiring disclosure, recusal from conflicted decisions, and independent review of conflicted transactions. Following proper conflict procedures allows legitimate transactions with appropriate oversight. Failing to disclose conflicts, allowing interested parties to vote on their own compensation, or conducting self-dealing without independent review violates compliance regardless of whether written policies exist.

How do we know if we’re still in compliance, or do we just hope we don’t hear from IRS? Proactive compliance verification is far better than hoping. Check TEOS database quarterly confirming your organization shows active status eligible to receive deductible contributions without revocation warnings. Review Form 990 filing history ensuring you haven’t missed any years. Conduct annual board review of activities confirming operations remain consistent with exempt purposes. Review compensation arrangements periodically ensuring independent approval and reasonableness. If you discover compliance problems, address them immediately rather than hoping IRS won’t notice—voluntary correction with cooperation is far better than IRS discovering violations during audits.

What to do next (DIY vs Done-With-You)

DIY approach: Create comprehensive filing calendar showing your Form 990 deadline (15th day of 5th month after fiscal year end) with 90-day, 60-day, and 30-day advance reminders. Determine which Form 990 version you must file based on revenue and asset thresholds, updating annually as organization grows. Gather financial records, program information, and governance documentation throughout the year rather than scrambling at deadline. Review Form 990 instructions thoroughly before completing return—don’t guess at answers to governance or activity questions. Complete all required schedules based on organizational activities. Have board review draft Form 990 before filing ensuring accuracy. File electronically through IRS-authorized e-file providers. Save filed returns and all supporting documentation for seven years minimum. Verify after filing that TEOS database still shows active status. Review organizational activities annually comparing to purposes approved in IRS determination ensuring substantial consistency. Avoid political campaign intervention completely and monitor lobbying to ensure insubstantial. Maintain conflict of interest procedures with annual disclosures and proper recusal documentation. If you miss a filing deadline or discover compliance problems, address immediately rather than hoping they’ll go unnoticed.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive ongoing federal compliance support for Riverside and Inland Empire nonprofits. We establish filing calendars with automated deadline reminders preventing missed Form 990 returns, prepare accurate complete annual returns reflecting organizational activities and governance, ensure board meeting minutes and policies support Form 990 governance responses, help organizations evaluate whether program evolution requires IRS notification of changes, provide clear guidance preventing prohibited political activity while allowing permitted advocacy, establish compensation review procedures ensuring independent approval with comparability documentation, monitor TEOS database quarterly verifying current active status, guide corrective action when compliance problems emerge including delinquent filing or reinstatement applications, and provide ongoing consultation as questions arise about activities, transactions, or situations with compliance implications. This ensures you maintain the tax-exempt status that funders verify and that your organization depends on for operations and fundraising.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Find Us Locally

Service Area: Moreno Valley, CA and surrounding areas

Coordinates: 33.9535, -117.2081

Address: 23945 Sunnymead Blvd. #4, Moreno Valley, CA 92553

Sources

- https://www.irs.gov/charities-non-profits/charitable-organizations

- https://www.irs.gov/forms-pubs/about-form-1023

- https://calnonprofits.org/

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.