05 Feb What Information Should a Nonprofit Prepare Before an IRS Exemption Application?

Short Answer

Before filing IRS Form 1023 or 1023-EZ, nonprofits should prepare Articles of Incorporation with required IRS language including dissolution clauses, adopted bylaws and governance policies demonstrating functional oversight, detailed program descriptions explaining what services will be provided to whom and how, three-year financial projections showing projected revenue sources and expenses, organizational meeting minutes documenting bylaw adoption and policy approval, conflict of interest policy with board disclosure procedures, and Employer Identification Number obtained from IRS. This preparation matters because incomplete applications trigger IRS requests for supplemental information delaying processing by months, poorly documented governance structures raise questions about charitable purpose and board oversight, and unrealistic financial projections suggest poor planning or unsustainable operations causing IRS to question organizational viability.

What formation and governance documents must be ready?

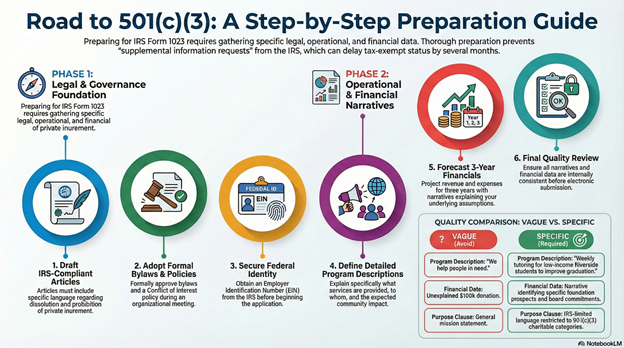

Articles of Incorporation with IRS-compliant language form the foundation. California Articles must contain specific provisions IRS requires: organizational purpose limited to recognized 501(c)(3) charitable categories, dissolution clause stating that upon dissolution assets will be distributed to other 501(c)(3) organizations or governmental purposes, and prohibition on private inurement stating no net earnings benefit individuals. If Articles lack this language, they must be amended before IRS application—retroactive amendments create complications better avoided through proper initial drafting.

Adopted bylaws demonstrate governance structure and operational procedures. IRS wants to see that boards will exercise genuine oversight through regular meetings, independent directors provide accountability rather than founder domination, conflict of interest procedures prevent self-dealing, and decision-making processes ensure democratic governance. Bylaws should be formally adopted at organizational meeting documented in minutes, not just downloaded templates sitting unsigned in files.

Conflict of interest policy proves commitment to preventing private benefit. IRS Form 1023 specifically asks whether the organization adopted a conflict of interest policy and requests a copy. The policy should require annual written disclosure from board members and officers identifying potential conflicts, establish procedures for recusal from conflicted decisions, and mandate independent review of transactions involving insiders. Many organizations incorporate conflict language directly into bylaws; others adopt separate standalone policies.

Organizational meeting minutes document that governance documents were properly adopted. Minutes should record the date, attendees, adoption of bylaws through board vote, approval of conflict policy, election of initial officers, authorization to apply for EIN and IRS determination, and other foundational decisions. These minutes prove the organization actually functions rather than existing only on paper.

What programmatic and operational information needs development?

Detailed program descriptions explain what charitable activities the organization will conduct. IRS needs to understand specifically what services you’ll provide, who will benefit from those services, how services will be delivered (frequency, location, staffing), and what outcomes or community impact you expect. Vague descriptions like “we help people in need” don’t satisfy IRS requirements. Specific descriptions like “we provide weekly academic tutoring to low-income high school students in Riverside, preparing participants for college admission and improving graduation rates” demonstrate clear charitable purpose.

Target population identification shows who benefits from programs. IRS evaluates whether programs serve genuine charitable purposes benefiting appropriate populations—people experiencing poverty, individuals lacking educational access, communities facing health challenges—rather than providing private benefits to specific individuals connected to founders. Define beneficiary populations with enough specificity to demonstrate focus while preserving reasonable flexibility.

Operational timelines indicate when programs will launch. New organizations applying for determination before beginning operations should provide realistic timelines showing when facilities will be secured, when staff or volunteers will be recruited, when services will commence, and how programs will scale over initial years. Unrealistic timelines suggesting immediate full operation without infrastructure raise IRS questions about planning quality.

Collaboration and partnership plans demonstrate community integration. Describing partnerships with schools, government agencies, established nonprofits, or community organizations strengthens applications by showing the organization understands the service landscape and has support rather than operating in isolation without community connections.

What financial information and projections are required?

Three-year financial projections showing revenue and expenses form the core IRS requirement. Organizations must project income sources (individual donations, foundation grants, corporate contributions, government funding, program fees, fundraising events, earned income) and expense categories (program costs, salaries, facilities, supplies, professional services, insurance, other overhead) for the current year plus next two years. Projections should be realistic and internally consistent—not showing $200,000 in program expenses with only $50,000 in projected revenue without explanation of how the gap will be covered.

Revenue source documentation explains where funding will come from. Rather than vague “donations” categories, identify specific likely funders—board member commitments, identified foundation prospects, corporate giving programs researched, realistic individual donor estimates. IRS wants to see that you’ve actually thought through fundraising strategy rather than hoping money appears. For organizations with committed funding, provide letters of intent or pledges demonstrating support.

Budget narratives explain major assumptions underlying projections. Why do you project $30,000 in foundation grants year one—have you identified specific foundations likely to fund your work? Why do program costs increase 50% in year two—are you expanding services or adding locations? Narrative explanations prevent IRS questions about unrealistic or unexplained figures.

Current financial status for existing organizations requires providing actual financial data. Organizations that incorporated and began operations before applying must submit current balance sheet, recent income statement, and explanation of activities to date. Organizations applying shortly after incorporation typically have minimal financial activity to report.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

Launch means preparing IRS applications carefully before submission rather than rushing incomplete applications. Riverside nonprofits that invest time developing thorough program descriptions, realistic financial projections, and complete governance documentation achieve smoother determination processes than organizations submitting hasty applications requiring supplemental information.

Fix becomes necessary when organizations submitted incomplete applications triggering IRS questions, provided unrealistic financial projections raising viability concerns, or filed with non-compliant Articles of Incorporation requiring amendments. Fixing these issues mid-application delays determination by months while corrections are made.

Fund depends on IRS determination, making application preparation critical. The faster you achieve determination through complete initial applications, the sooner you can pursue grants. Organizations stuck responding to IRS supplemental questions for months miss funding opportunities during the delay.

Federal Recognition is what IRS applications achieve. Proper preparation ensures you obtain recognition efficiently rather than experiencing delays from incomplete submissions or IRS concerns about governance, programs, or finances.

CA Compliance Triangle preparation should happen simultaneously with IRS application preparation. While gathering governance documents, financial projections, and program descriptions for IRS, also prepare for California Franchise Tax Board exemption application and Attorney General Registry registration.

Step-by-step: How NPLO helps organizations prepare IRS applications

Step 1: Document Review We review existing formation documents ensuring Articles contain required IRS language.

Step 2: Governance Documentation We verify bylaws and policies are adopted, or help develop and adopt them if missing.

Step 3: Program Development We work with clients developing detailed program descriptions with appropriate specificity.

Step 4: Financial Projections We create realistic three-year budgets with documented assumptions and explanations.

Step 5: Information Compilation We gather all required information organizing it for efficient application completion.

Step 6: Application Preparation We complete Form 1023 or 1023-EZ accurately with all required narratives and attachments.

Step 7: Quality Review We verify applications are complete, accurate, and internally consistent before submission.

Step 8: Submission Management We submit applications electronically and track processing, responding to any IRS questions.

Checklist: Information to prepare before IRS application

Formation Documents:

- Articles of Incorporation (with required IRS language)

- Bylaws (formally adopted)

- Organizational meeting minutes

- EIN assignment letter or confirmation

Governance Documents:

- Conflict of interest policy

- Whistleblower policy (recommended)

- Board member list with addresses

- Officer list with positions

Program Information:

- Detailed program descriptions

- Target population definitions

- Service delivery methods

- Expected outcomes

- Program timelines

- Partnership/collaboration plans

Financial Information:

- Three-year revenue projections

- Three-year expense projections

- Budget narratives explaining assumptions

- Current financial statements (if operating)

- Funding commitment letters (if available)

- Fundraising strategy description

Organizational Details:

- Organization history and formation story

- Mission statement

- Website or social media presence (if exists)

- Any existing marketing materials

Quick Answers (PPA)

Can we apply for IRS determination immediately after incorporation, or should we wait until programs are operating? Apply as soon as you have required documents ready—don’t wait for programs to launch. Organizations applying within 27 months of incorporation receive retroactive recognition effective from incorporation date if approved. Waiting serves no purpose and delays your ability to tell donors contributions are deductible and to pursue grants requiring federal recognition. IRS evaluates planned activities described in applications, not actual operating history, for new organizations. You’ll provide program descriptions, financial projections, and governance documentation demonstrating what you will do rather than proving what you’ve already accomplished.

What if our financial projections change after we submit the application—do we need to notify IRS? Minor variations between projected and actual finances don’t require IRS notification. Projections are estimates, not guarantees, and IRS expects that actual results will differ somewhat from applications. However, substantial changes to organizational plans—adding major program areas not described in applications, significantly exceeding projected revenue requiring different foundation classification, or fundamental shifts in operational approach—should be disclosed through amended applications or supplemental correspondence. The key is whether changes affect the basis on which determination was granted. Modest budget adjustments don’t trigger notification requirements.

Should we include letters of support from community members or partners with our IRS application? Letters of support aren’t required and IRS doesn’t specifically request them for most applications. However, letters from established organizations confirming partnerships, from funders confirming grant commitments, or from community leaders endorsing your mission can strengthen applications by demonstrating community integration and support. Include them if they add substantive value—letters confirming concrete partnerships or funding are helpful, while generic endorsement letters add little. Never include so many attachments that critical information gets buried in volume.

What if we don’t have three years of financial projections because we’re brand new—can we estimate? Yes, new organizations must estimate three-year projections even without operating history. Base projections on reasonable assumptions: research what similar organizations in your region spend for comparable programs, identify realistic funding sources through foundation research and donor conversations, and calculate necessary expenses for activities you plan to conduct. Document assumptions explaining where figures come from. IRS understands new organizations don’t have historical data—they want to see that you’ve thought through financial sustainability rather than launching without any financial planning.

Can we amend our Articles of Incorporation after IRS approval if we realize we want to add programs, or are we locked into what we initially described? Organizations can and should adjust programs as community needs evolve without IRS approval for reasonable modifications within stated charitable purposes. If your approved purpose is “advancing education through youth programs,” changing from tutoring to mentorship or adding college prep services is reasonable evolution not requiring IRS notification. However, substantial mission shifts—adding completely different charitable purpose categories or fundamentally changing who you serve—may require filing amended applications or notifying IRS of significant changes. The key distinction is modifications within approved charitable purposes (allowed and expected) versus entirely new purposes (requiring IRS review).

What to do next (DIY vs Done-With-You)

DIY approach: Review your California Articles of Incorporation verifying they contain required IRS language about charitable purposes, asset dissolution, and private inurement prohibition—if missing, amend Articles before IRS application. Ensure bylaws are formally adopted at organizational meeting documented in minutes, not just downloaded templates. Develop or adopt conflict of interest policy requiring annual disclosures. Obtain EIN if not already acquired. Draft detailed program descriptions explaining specifically what services you’ll provide, to whom, how, and with what expected outcomes—spend time making these clear and specific. Create realistic three-year financial projections showing revenue sources and expense categories with narrative explanations of assumptions. Compile everything in organized fashion. Download appropriate IRS form (1023-EZ if eligible, Form 1023 otherwise) and instructions. Complete application carefully answering all questions accurately and attaching required documents. Create Pay.gov account and pay user fee. Submit application electronically through IRS system. Track status through online portal. Be prepared to respond to any IRS supplemental information requests promptly.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive IRS application preparation for Riverside and Inland Empire nonprofits. We review formation documents ensuring Articles contain required IRS language and amending if necessary, verify or help develop adopted bylaws and governance policies, work with clients creating detailed program descriptions with appropriate specificity and clarity, develop realistic three-year financial projections with documented assumptions, compile all required information organized efficiently, prepare complete applications whether Form 1023-EZ or detailed Form 1023, verify applications are accurate and internally consistent before submission, submit applications electronically through IRS system, track processing status responding to any supplemental questions, and obtain determination letters confirming recognition. This ensures your application is complete, professional, and positioned for smooth approval without delays from incomplete submissions or IRS concerns about governance, programs, or financial sustainability.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Find Us Locally

Service Area: Moreno Valley, CA and surrounding areas

Coordinates: 33.9535, -117.2081

Address: 23945 Sunnymead Blvd. #4, Moreno Valley, CA 92553

Sources

- https://www.irs.gov/charities-non-profits/charitable-organizations

- https://www.irs.gov/forms-pubs/about-form-1023

- https://calnonprofits.org/

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.