28 Jan What Does “Public Benefit” Mean in Nonprofit Terms?

Short Answer

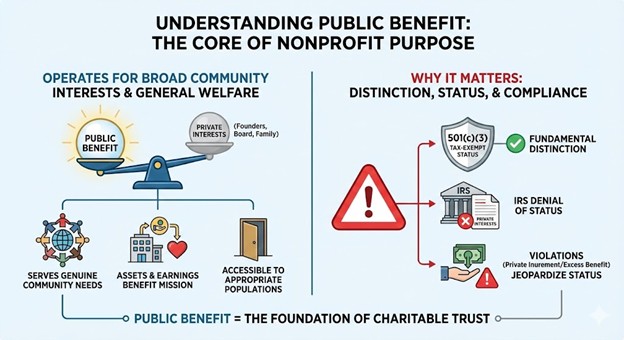

“Public benefit” in nonprofit terms means the organization operates exclusively to serve broad community interests and general public welfare rather than private interests or benefits for specific individuals like founders, board members, or their families. This concept requires that charitable activities address genuine community needs accessible to appropriate populations, that organizational assets and earnings benefit the charitable mission rather than enriching individuals, and that operations serve public rather than private purposes even when specific programs target defined populations. Public benefit matters because it’s the fundamental distinction between tax-exempt charitable organizations and for-profit businesses, because IRS denies 501(c)(3) status to organizations primarily serving private interests, and because violations of public benefit principles through private inurement or excess benefit transactions can jeopardize tax-exempt status.

How does public benefit differ from private benefit?

Public benefit focuses on serving community needs broadly accessible to appropriate populations. A Murrieta nonprofit providing literacy tutoring to low-income adults serves public benefit because educational services address genuine community needs and anyone meeting income eligibility can participate. The benefit flows to the community through improved literacy rates, economic mobility, and civic participation. Services don’t need to serve literally everyone to qualify as public benefit—targeting specific populations with demonstrated needs (low-income families, homeless individuals, at-risk youth) still serves public purposes.

Private benefit flows primarily to specific identified individuals who control or have special relationships with the organization. If a nonprofit’s primary purpose is employing the founder’s family members at above-market salaries, providing services exclusively to the founder’s relatives, or conducting activities that primarily benefit board members’ businesses through contracts or referrals, it serves private rather than public benefit. The IRS distinguishes between incidental private benefit (unavoidable minor benefits to individuals while pursuing genuine public purposes) and substantial private benefit that undermines charitable status.

The “exclusive” test means organizations must operate exclusively for charitable purposes even when activities incidentally benefit some individuals. A homeless shelter serves public benefit helping anyone experiencing homelessness, even though specific individuals receive meals and beds. However, if that shelter only serves the founder’s family members or provides luxury accommodations exceeding genuine need, it crosses into private benefit. The test isn’t whether any individuals benefit—all charitable work benefits specific people—but whether the primary purpose serves public welfare.

Accessibility and non-discrimination reinforce public benefit principles. Organizations serving defined populations for legitimate charitable reasons (poverty relief, health promotion, education) serve public benefit when services are accessible to everyone meeting appropriate eligibility criteria without discrimination based on relationships with insiders. If you provide youth programs only for your own children and their friends while excluding other qualified youth, you’re not serving genuine public benefit despite claiming an educational purpose.

What specific practices violate public benefit requirements?

Private inurement represents the most serious public benefit violation. This occurs when organizational net earnings benefit insiders—founders, board members, substantial contributors, or their families—beyond reasonable compensation for actual services rendered. Examples include paying the founder’s spouse an executive director salary far exceeding market rates for the work performed, distributing organizational surplus to board members as bonuses, selling organizational assets to insiders at below-market prices, or providing free services to board members while charging others. Private inurement violations can result in IRS revocation of tax-exempt status.

Excess benefit transactions provide more-than-reasonable compensation or benefits to disqualified persons (insiders). Even without intentional private inurement, paying executives compensation substantially exceeding market rates for comparable positions constitutes excess benefit transactions. The IRS imposes excise taxes on recipients of excess benefits and on organization managers who knowingly approved them. While not immediately revoking tax-exempt status like private inurement, patterns of excess benefit transactions indicate the organization isn’t operated exclusively for public benefit.

Self-dealing occurs when insiders transact business with the organization in ways that benefit themselves. While not absolutely prohibited, self-dealing requires rigorous independent review, full disclosure, competitive pricing or comparability data, and clear demonstration that arrangements benefit the organization fairly. A board member’s company providing services at premium prices without competitive bidding or market analysis likely constitutes improper self-dealing serving private benefit.

Serving too-limited beneficiary classes can indicate private rather than public purpose. If your stated purpose is “providing scholarships to descendants of XYZ Company employees,” you’re serving such a narrow class defined by private employment relationships rather than genuine charitable criteria that IRS may question public benefit. Legitimate scholarship programs serve students based on merit, need, or field of study—charitable criteria—not based on family employment relationships with private companies.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

Launch includes structuring organizations to serve genuine public benefit from inception. Murrieta nonprofits should establish governance demonstrating public purpose, adopt policies preventing private benefit, and design programs serving appropriate populations rather than insider interests.

Fix addresses organizations that inadvertently allowed private benefit through founder control, family hiring without independent review, or programs primarily serving insiders. Correcting these issues requires restructuring governance, implementing proper conflict procedures, and potentially unwinding problematic transactions.

Fund depends on demonstrating public benefit because funders verify that organizations serve genuine charitable purposes. Grant applications to foundations serving public interest won’t support organizations primarily benefiting founders or insiders rather than intended beneficiary populations.

Federal Recognition hinges entirely on public benefit. IRS 501(c)(3) determination requires organizations demonstrate that they will operate exclusively for public rather than private benefit. Applications showing governance structures or planned activities suggesting private benefit face denial.

CA Compliance Triangle includes Attorney General oversight of charitable assets ensuring they serve public purposes. California law prohibits private benefit from charitable organizations and authorizes AG enforcement when organizations deviate from public benefit purposes.

[[DIAGRAM IMAGE PLACEHOLDER: Title=Federal Recognition + California Compliance Triangle Diagram Type=Triangle + foundation bar Nodes/Labels=IRS (foundation bar: Tax-Exempt Status + Annual Filing Requirements); CA Secretary of State (top vertex: Entity Status / Statement of Information); CA Franchise Tax Board (bottom-left vertex: State Tax Exemption / Annual Filing Requirements); CA Attorney General Registry of Charities (bottom-right vertex: Fundraising Registration / Annual Renewal Reporting) Caption=Grant readiness is easier when your federal status is verifiable and your California filings are current. ]]

Step-by-step: How NPLO helps organizations maintain public benefit focus

Step 1: Mission Alignment Review We evaluate whether stated purposes genuinely serve public benefit or inadvertently favor private interests.

Step 2: Governance Structure Assessment We ensure boards maintain independence from founders and that decision-making serves organizational mission.

Step 3: Program Design Evaluation We verify programs serve appropriate populations based on charitable criteria rather than insider relationships.

Step 4: Conflict Policy Implementation We establish robust conflict procedures preventing self-dealing and ensuring independent review of insider transactions.

Step 5: Compensation Review We verify that founder, board, and family compensation reflects market rates for services rather than private benefit extraction.

Step 6: Beneficiary Eligibility Criteria We help develop program eligibility criteria based on legitimate charitable purposes rather than relationships with insiders.

Step 7: Asset Protection Provisions We ensure dissolution clauses and operational practices preserve charitable assets for public benefit.

Step 8: Ongoing Monitoring We establish systems for boards to monitor that operations continue serving public benefit as organizations evolve.

Checklist: Public benefit compliance elements

- Charitable purpose serves genuine community needs

- Programs accessible to appropriate populations without discrimination

- Eligibility criteria based on charitable factors (need, merit) not insider relationships

- No distribution of net earnings to individuals

- Compensation limited to reasonable amounts for services rendered

- Board majority independent of founders and uncompensated

- Conflict of interest procedures preventing self-dealing

- Asset protection ensuring charitable use

- Dissolution provisions directing assets to other charities

- Services provided at no charge or affordable fees related to costs

- No exclusive benefits to founders, board, donors, or families

- Activities serve public welfare not private commercial interests

- Decision-making prioritizes mission over insider preferences

Quick Answers (PPA)

Can a nonprofit serve a specific small group and still qualify as public benefit? Yes, serving defined populations with demonstrated needs constitutes public benefit when based on legitimate charitable criteria. A nonprofit serving homeless veterans in Murrieta serves public benefit even though beneficiaries are a specific small group, because veteran status and homelessness are charitable eligibility criteria, services are accessible to any veteran meeting those criteria, and addressing veteran homelessness serves broader community welfare. The distinction is between serving defined populations based on charitable need versus serving limited groups defined by relationships with insiders—serving your extended family exclusively isn’t public benefit even if they have genuine needs.

What’s the difference between paying ourselves reasonable salaries versus private benefit? Reasonable compensation for actual services rendered is explicitly permitted and necessary—nonprofits need staff to deliver programs. Private benefit occurs when compensation exceeds reasonable amounts or when individuals receive benefits without providing equivalent services. The keys are independent board approval of compensation, comparability data showing market rates, and clear employment providing genuine value. Paying yourself as executive director at market rates for full-time work is reasonable compensation. Paying yourself twice market rates, or paying family members who don’t actually work, crosses into private benefit.

Does charging fees for services violate public benefit principles? No, charging reasonable fees related to service costs doesn’t violate public benefit as long as fees don’t exclude the intended beneficiary population and the organization provides accommodation for those unable to pay. Many charitable organizations charge program fees covering costs while maintaining public benefit through sliding scale fees, scholarships, or free access for those demonstrating financial need. The test is whether fee structures support sustainable service delivery while remaining accessible to intended populations, not whether services are completely free. However, charging premium prices far exceeding costs to generate profits for distribution would violate public benefit.

Can we provide services to board members’ family members without violating public benefit? Yes, if services are provided on the same terms available to other eligible participants without preferential treatment and if board members recuse themselves from program decisions. If your youth tutoring program serves all qualifying students including some who happen to be related to board members, that’s acceptable public benefit as long as no preference is given. However, if the program primarily serves board members’ children with limited access for others, or if board members’ relatives receive free services while others pay, you’ve crossed into private benefit. The key is equal access and treatment regardless of insider relationships.

What happens if IRS determines we’re providing private rather than public benefit? For new organizations, IRS denies 501(c)(3) determination applications when proposed activities indicate private rather than public benefit. For existing organizations, IRS can revoke tax-exempt status if operations deviate from public benefit purposes, impose excise taxes on private inurement or excess benefit transactions, and potentially pursue criminal charges in egregious cases of insider enrichment. California Attorney General can also pursue enforcement including removing board members, unwinding improper transactions, and imposing civil penalties. The consequences are serious—maintaining genuine public benefit focus isn’t optional for tax-exempt charitable organizations.

What to do next (DIY vs Done-With-You)

DIY approach: Review your organizational mission, programs, and operations asking whether they genuinely serve public welfare or primarily benefit founders, board members, or their families. Examine beneficiary eligibility criteria—are they based on charitable need (poverty, health conditions, educational access) or based on relationships with insiders? Evaluate compensation for all founders, board members, and their relatives—is it based on independent review using comparability data, or determined by the recipients themselves? Review your board composition—is the majority independent and uncompensated, or dominated by founders and family members receiving benefits? Assess program accessibility—can anyone meeting legitimate charitable criteria participate, or are services primarily available to people connected to insiders? If you identify practices that appear to serve private more than public benefit, implement corrective measures: restructure board for independence, adopt robust conflict policies, establish independent compensation review, revise eligibility criteria to charitable factors, and ensure equal access. Document that operations serve genuine public purposes through meeting minutes, policy adoption, and program reporting showing who benefits.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive public benefit compliance review for Murrieta and Inland Empire nonprofits. We evaluate whether missions and programs genuinely serve public benefit or inadvertently favor private interests, assess governance structures ensuring boards maintain independence and serve organizational missions, review program designs verifying services reach appropriate populations based on charitable criteria, implement conflict policies preventing self-dealing and ensuring independent transaction review, verify compensation practices reflect market rates rather than private benefit extraction, develop program eligibility criteria based on legitimate charitable purposes, establish asset protection provisions preserving charitable use, and create monitoring systems ensuring ongoing public benefit focus as organizations evolve. This ensures your organization maintains the public benefit focus required for tax-exempt status while avoiding private benefit violations that jeopardize charitable recognition.

How does public benefit differ from private benefit?

Public benefit focuses on serving community needs broadly accessible to appropriate populations. A Murrieta nonprofit providing literacy tutoring to low-income adults serves public benefit because educational services address genuine community needs and anyone meeting income eligibility can participate. The benefit flows to the community through improved literacy rates, economic mobility, and civic participation. Services don’t need to serve literally everyone to qualify as public benefit—targeting specific populations with demonstrated needs (low-income families, homeless individuals, at-risk youth) still serves public purposes.

Private benefit flows primarily to specific identified individuals who control or have special relationships with the organization. If a nonprofit’s primary purpose is employing the founder’s family members at above-market salaries, providing services exclusively to the founder’s relatives, or conducting activities that primarily benefit board members’ businesses through contracts or referrals, it serves private rather than public benefit. The IRS distinguishes between incidental private benefit (unavoidable minor benefits to individuals while pursuing genuine public purposes) and substantial private benefit that undermines charitable status.

The “exclusive” test means organizations must operate exclusively for charitable purposes even when activities incidentally benefit some individuals. A homeless shelter serves public benefit helping anyone experiencing homelessness, even though specific individuals receive meals and beds. However, if that shelter only serves the founder’s family members or provides luxury accommodations exceeding genuine need, it crosses into private benefit. The test isn’t whether any individuals benefit—all charitable work benefits specific people—but whether the primary purpose serves public welfare.

Accessibility and non-discrimination reinforce public benefit principles. Organizations serving defined populations for legitimate charitable reasons (poverty relief, health promotion, education) serve public benefit when services are accessible to everyone meeting appropriate eligibility criteria without discrimination based on relationships with insiders. If you provide youth programs only for your own children and their friends while excluding other qualified youth, you’re not serving genuine public benefit despite claiming an educational purpose.

What specific practices violate public benefit requirements?

Private inurement represents the most serious public benefit violation. This occurs when organizational net earnings benefit insiders—founders, board members, substantial contributors, or their families—beyond reasonable compensation for actual services rendered. Examples include paying the founder’s spouse an executive director salary far exceeding market rates for the work performed, distributing organizational surplus to board members as bonuses, selling organizational assets to insiders at below-market prices, or providing free services to board members while charging others. Private inurement violations can result in IRS revocation of tax-exempt status.

Excess benefit transactions provide more-than-reasonable compensation or benefits to disqualified persons (insiders). Even without intentional private inurement, paying executives compensation substantially exceeding market rates for comparable positions constitutes excess benefit transactions. The IRS imposes excise taxes on recipients of excess benefits and on organization managers who knowingly approved them. While not immediately revoking tax-exempt status like private inurement, patterns of excess benefit transactions indicate the organization isn’t operated exclusively for public benefit.

Self-dealing occurs when insiders transact business with the organization in ways that benefit themselves. While not absolutely prohibited, self-dealing requires rigorous independent review, full disclosure, competitive pricing or comparability data, and clear demonstration that arrangements benefit the organization fairly. A board member’s company providing services at premium prices without competitive bidding or market analysis likely constitutes improper self-dealing serving private benefit.

Serving too-limited beneficiary classes can indicate private rather than public purpose. If your stated purpose is “providing scholarships to descendants of XYZ Company employees,” you’re serving such a narrow class defined by private employment relationships rather than genuine charitable criteria that IRS may question public benefit. Legitimate scholarship programs serve students based on merit, need, or field of study—charitable criteria—not based on family employment relationships with private companies.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

Launch includes structuring organizations to serve genuine public benefit from inception. Murrieta nonprofits should establish governance demonstrating public purpose, adopt policies preventing private benefit, and design programs serving appropriate populations rather than insider interests.

Fix addresses organizations that inadvertently allowed private benefit through founder control, family hiring without independent review, or programs primarily serving insiders. Correcting these issues requires restructuring governance, implementing proper conflict procedures, and potentially unwinding problematic transactions.

Fund depends on demonstrating public benefit because funders verify that organizations serve genuine charitable purposes. Grant applications to foundations serving public interest won’t support organizations primarily benefiting founders or insiders rather than intended beneficiary populations.

Federal Recognition hinges entirely on public benefit. IRS 501(c)(3) determination requires organizations demonstrate that they will operate exclusively for public rather than private benefit. Applications showing governance structures or planned activities suggesting private benefit face denial.

CA Compliance Triangle includes Attorney General oversight of charitable assets ensuring they serve public purposes. California law prohibits private benefit from charitable organizations and authorizes AG enforcement when organizations deviate from public benefit purposes.

[[DIAGRAM IMAGE PLACEHOLDER: Title=Federal Recognition + California Compliance Triangle Diagram Type=Triangle + foundation bar Nodes/Labels=IRS (foundation bar: Tax-Exempt Status + Annual Filing Requirements); CA Secretary of State (top vertex: Entity Status / Statement of Information); CA Franchise Tax Board (bottom-left vertex: State Tax Exemption / Annual Filing Requirements); CA Attorney General Registry of Charities (bottom-right vertex: Fundraising Registration / Annual Renewal Reporting) Caption=Grant readiness is easier when your federal status is verifiable and your California filings are current. ]]

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Find Us Locally

Service Area: Moreno Valley, CA and surrounding areas

Coordinates: 33.9535, -117.2081

Address: 23945 Sunnymead Blvd. #4, Moreno Valley, CA 92553

Sources

- https://www.irs.gov/charities-non-profits/charitable-organizations

- https://www.irs.gov/forms-pubs/about-form-1023

- https://calnonprofits.org/

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.