23 Jan Can I Pay Myself in a Nonprofit (in General Terms) Without Breaking Rules?

Short Answer

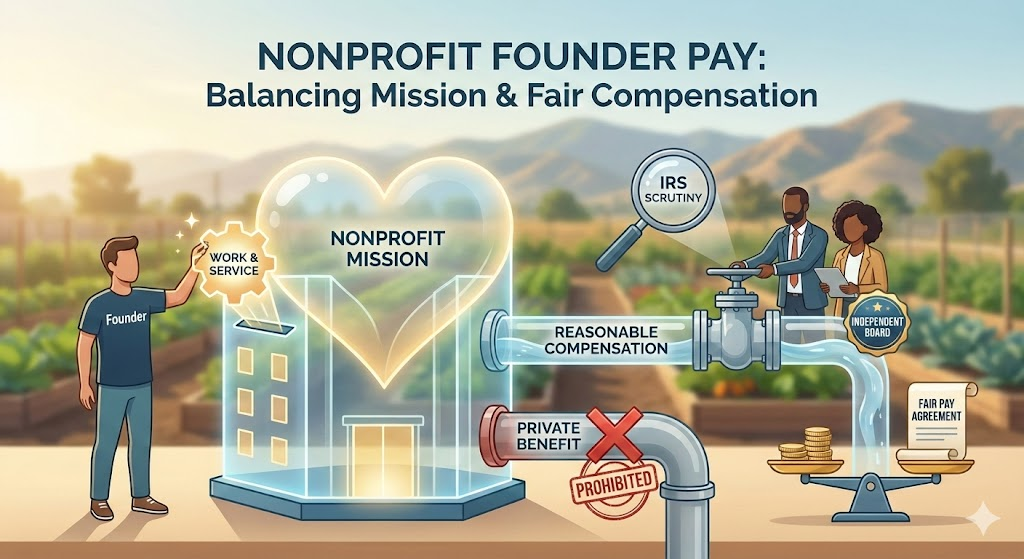

Nonprofit founders and board members can receive reasonable compensation for actual services performed in employee or contractor roles, but cannot receive compensation solely for serving as directors or for ownership interest in the organization—the key distinction is being paid fairly for work done versus extracting organizational assets as profit or personal benefit. IRS rules prohibit “private inurement” (insiders benefiting from nonprofit assets beyond reasonable compensation for services) and “excess benefit transactions” (compensation exceeding fair market value for services rendered), requiring that any payments to founders, board members, or family members receive independent board review, reflect market-rate compensation for comparable positions, and be documented with clear employment agreements or contractor arrangements. Eligibility varies by organization, but Temecula and Inland Empire nonprofits can employ founders or board members in staff roles with appropriate compensation as long as governance structures ensure independence, conflicts are properly managed, and compensation remains reasonable—creating sustainable leadership while maintaining the fundamental nonprofit principle that organizational assets serve charitable purposes rather than private enrichment.

What’s the fundamental difference between compensation for services versus prohibited private benefit?

The private inurement prohibition represents the core IRS principle distinguishing nonprofits from for-profit businesses—no part of a nonprofit’s net earnings can benefit private individuals beyond reasonable compensation for actual services rendered. This prohibition prevents nonprofits from functioning as profit-distribution vehicles where founders or insiders extract organizational assets as personal income without providing equivalent value through work performed. The IRS carefully scrutinizes transactions between nonprofits and insiders (founders, board members, substantial contributors, family members) to ensure these transactions serve organizational interests rather than enriching individuals.

Reasonable compensation for services performed is explicitly permitted and necessary for nonprofit operations. Nonprofits need staff to deliver programs, manage operations, raise funds, and maintain compliance—these staff members, whether founders or not, deserve fair pay for their work. The reasonableness standard requires that compensation aligns with what similar organizations pay for comparable positions, reflects the skills and experience the position requires, and relates directly to actual services performed rather than being disguised profit distribution. A founder serving as executive director managing a $500,000 budget organization might reasonably earn $60,000-$80,000 annually for full-time work, while a founder demanding $200,000 salary for the same role would face IRS questions about excessive compensation.

Independent review by disinterested board members forms the critical governance mechanism ensuring compensation decisions serve organizational rather than personal interests. When setting compensation for founders, board members, or family members of either, the IRS expects organizations to follow careful procedures: independent directors (those without personal or family interest in the compensation decision) review and approve compensation, the board bases decisions on comparable salary data from similar organizations and positions, the approval process is documented in board meeting minutes including the comparability data reviewed, and the individual whose compensation is being set doesn’t participate in the decision or vote. These procedures demonstrate that compensation reflects market rates for services rather than insider favoritism.

The distinction between founder as volunteer board member versus founder as paid employee matters enormously for both legal compliance and organizational perception. Serving as a board director is voluntary governance service—directors cannot receive compensation for board service itself in California nonprofit public benefit corporations. However, a board director can separately serve as a paid employee (like executive director) as long as proper conflicts are managed, the employee role is distinct from the board role, compensation is independently approved, and board independence is maintained (typically requiring that fewer than 49% of directors receive compensation). This dual role creates complexity requiring careful conflict management but is legally permissible and practically common in smaller nonprofits where founders provide both governance and operational leadership.

How do you determine what compensation is “reasonable” and properly document it?

Comparability data from similar organizations provides the foundation for determining reasonable compensation. Temecula nonprofits should research what organizations of similar size (budget, staff, complexity), in similar program areas (education, health, social services), in similar geographic markets (Inland Empire, Southern California), pay for comparable positions (executive director, program director, development director). Sources for comparability data include nonprofit salary surveys published by state associations or national organizations, Form 990 filings from similar nonprofits showing officer compensation (publicly available through GuideStar/Candid), job postings for similar positions showing offered salary ranges, and professional compensation consultants specializing in nonprofit pay scales.

The three-factor safe harbor test from IRS regulations provides a framework that, when followed, creates presumption of reasonableness protecting organizations from excess benefit transaction penalties. Organizations satisfy the safe harbor by: (1) having compensation approved in advance by authorized body (board or compensation committee) composed entirely of individuals without conflicts of interest in the decision, (2) basing the decision on appropriate comparability data showing what similar organizations pay for similar positions, and (3) adequately documenting the decision contemporaneously including the comparability data relied upon and the basis for determining compensation was reasonable. Following this safe harbor process doesn’t guarantee compensation is reasonable—extremely high compensation won’t be protected just because procedures were followed—but it shifts burden of proof to IRS to demonstrate unreasonableness.

Written employment agreements or contractor arrangements document compensation clearly and establish mutual expectations. These agreements should specify: compensation amount (salary or hourly rate), whether compensation is full-time or part-time and expected hours, what services the individual will perform (detailed position description), benefits provided beyond salary (health insurance, retirement contributions, paid leave), evaluation procedures and performance expectations, and term of employment or contract renewal provisions. Written agreements prevent misunderstandings, provide documentation for IRS review, and demonstrate professionalism that strengthens rather than weakens nonprofit credibility.

Board meeting minutes documenting compensation decisions create the permanent record proving independent review occurred. Minutes should include: who participated in the compensation discussion (identifying that interested parties were absent or recused), what comparability data the board reviewed (naming specific surveys, Form 990s, or other sources), how the board determined proposed compensation was reasonable based on comparables, the vote authorizing compensation with individual votes recorded, and the date of the decision. These contemporaneous minutes (recorded at or near the time decisions are made) are critical if IRS later questions compensation—claiming you followed proper procedures years after the fact without contemporaneous documentation won’t satisfy IRS requirements.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

The Nonprofit Launch Office operates within a strategic framework designed to help California nonprofits move from formation to fundability:

Launch includes making strategic decisions about founder compensation from the beginning—whether founders will serve as unpaid volunteers during startup phase, whether one founder will become paid executive director while others remain unpaid board members, or whether the organization will delay any founder compensation until revenue reaches sustainable levels. Launch-phase compensation planning prevents common problems: setting compensation too high relative to organizational revenue creating financial stress, paying founders without proper independent approval creating IRS problems, or creating compensation disparities between founders causing internal conflict.

Fix addresses situations where compensation arrangements created problems—founders paid without independent board approval requiring retroactive documentation and possibly repayment, compensation set at levels that comparability data don’t support requiring adjustment, or lack of written employment agreements creating confusion about expectations and authority. Fix work might involve developing compensation policies that weren’t established during Launch, securing independent compensation review for existing arrangements, or adjusting excessive compensation to reasonable levels.

Fund intersects with compensation because funders review organizational budgets and Form 990 compensation disclosures when evaluating grant applications. Funders question situations where executive compensation consumes high percentages of organizational budgets, where founder compensation seems excessive relative to organizational size, or where multiple family members receive compensation suggesting nepotism rather than merit-based employment. Reasonable, properly documented compensation strengthens grant applications by demonstrating fiscal responsibility; questionable compensation patterns weaken applications by raising concerns about financial management.

Federal Recognition through IRS 501(c)(3) determination involves scrutiny of proposed compensation arrangements described in Form 1023 applications. The IRS examines whether founders plan to receive compensation, whether governance structures ensure independence in compensation decisions, and whether proposed compensation seems reasonable for organizational size and scope. Organizations proposing that founders receive significant compensation from small budgets may face IRS questions requiring explanation and justification.

CA Compliance Triangle (Secretary of State, Franchise Tax Board, Attorney General Registry) includes specific California requirements about board member compensation. California law prohibits directors of nonprofit public benefit corporations from receiving compensation for board service (though they can be reimbursed for expenses). The Attorney General monitors compensation through Form 990 and RRF-1 reviews, investigating situations where compensation appears excessive or where insider transactions suggest private benefit violations.

Step-by-step: How NPLO helps nonprofits establish appropriate compensation practices

Step 1: Compensation Philosophy Development We help boards articulate compensation philosophy appropriate to organizational stage—should the organization prioritize paying competitive salaries to attract talent, or maintain lean budgets with below-market compensation while building programs? Should founders receive any compensation during startup, or volunteer until revenue reaches specific thresholds? These philosophical decisions guide specific compensation choices and prevent reactionary decisions made under financial pressure.

Step 2: Conflict of Interest Assessment We identify all potential compensation conflicts requiring management—which board members are or may become employees, which board members have family members as employees, which substantial donors might receive compensation, and what independent directors exist to review conflicted compensation decisions. Clear conflict mapping ensures proper procedures are followed before compensation is set.

Step 3: Comparability Research and Documentation We help gather appropriate comparability data from nonprofit salary surveys, similar organization Form 990 filings, job postings, and industry benchmarks. We document data sources, identify comparable organizations and positions, and prepare summary reports showing compensation ranges for positions being considered. This research provides the foundation for independent board decisions about reasonable compensation.

Step 4: Independent Board Review Process We guide proper governance procedures for compensation approval—interested parties recuse themselves from discussions and votes, independent directors review comparability data and discuss proposed compensation, decisions are documented in contemporaneous board meeting minutes including the data relied upon, and approval votes are recorded with individual directors’ votes noted. Proper procedures create the documentation trail proving independent review occurred.

Step 5: Written Agreement Development We prepare employment agreements or contractor arrangements documenting compensation terms clearly—position title and reporting structure, salary or hourly rate with payment schedule, full-time or part-time status and expected hours, detailed description of services and responsibilities, benefits beyond salary, evaluation procedures and performance expectations, and term or renewal provisions. Written agreements prevent misunderstandings and provide documentation for IRS and funder review.

Step 6: Form 990 Disclosure Preparation We ensure Form 990 compensation disclosures accurately reflect approved compensation—Part VII officer compensation reporting, Schedule J supplemental compensation details for highly compensated individuals, narrative explanations in Schedule O for compensation practices, and compliance with reporting thresholds requiring detailed disclosure. Accurate Form 990 reporting prevents IRS questions and demonstrates transparency.

Step 7: Policy Implementation We help establish compensation policies governing future decisions—requiring independent review for all insider compensation, specifying what comparability data will be reviewed, documenting decision-making procedures, establishing regular compensation review schedules, and creating procedures for handling compensation increases or bonuses. Written policies guide consistent practices and demonstrate commitment to appropriate compensation practices.

Step 8: Ongoing Compliance Monitoring We establish systems for reviewing compensation periodically against comparability data, ensuring continued reasonableness as organizations grow, documenting annual review in board minutes, and adjusting compensation when organizational size or market rates change significantly. Ongoing monitoring prevents compensation from becoming excessive over time as organizations succeed and grow.

Checklist: What you should consider before establishing founder compensation

Temecula founders considering nonprofit compensation should address:

- Financial sustainability assessing whether organizational revenue can support proposed compensation while maintaining program funding and reserves

- Board independence ensuring that a majority of directors are unrelated and uncompensated to maintain genuine governance oversight

- Comparable position research identifying what similar organizations pay for similar work in similar markets

- Independent approval securing compensation approval from disinterested directors who don’t personally benefit from the decision

- Written employment terms documenting compensation, responsibilities, hours, benefits, and expectations in employment agreements

- Conflict disclosure requiring annual written disclosure of all conflicts including compensation arrangements

- Form 990 implications understanding that compensation will be publicly disclosed on annual Form 990 filings

- Funder perception considering how compensation will appear to grant makers reviewing budgets and Form 990s

- IRS safe harbor compliance following the three-factor test for approval, comparability, and documentation

- California law compliance ensuring compensation complies with prohibition on paying directors for board service

- Alternative compensation timing considering whether delaying compensation until revenue grows reduces financial stress and IRS scrutiny

- Partial compensation evaluating whether part-time employment or reduced salaries during startup phase is more sustainable than full compensation

- Non-financial compensation exploring whether benefits like health insurance, professional development, or flexible schedules provide value beyond cash salary

- Succession planning considering how compensation arrangements affect organizational sustainability if founder transitions out

- Tax implications understanding that compensation is taxable income requiring W-2 or 1099 reporting

Quick Answers (PPA)

Can board members receive any compensation at all, or must board service always be unpaid? California law prohibits directors of nonprofit public benefit corporations from receiving compensation for serving on the board itself—board service is volunteer governance work. However, board directors can receive compensation for providing services to the organization in roles separate from board membership—a director who also serves as executive director, program coordinator, or consultant can be paid reasonably for those services as long as: proper conflicts are disclosed and managed, fewer than 49% of directors receive any compensation from the organization, compensation is approved by independent directors without conflicts, and the amounts are reasonable for services performed. The key distinction is payment for actual work performed in employee or contractor roles versus payment for being a board member.

What counts as “reasonable” compensation—is there a specific percentage of budget that’s too high? The IRS doesn’t specify maximum percentages of budget for compensation but evaluates reasonableness based on comparability to what similar organizations pay for similar work. A small startup nonprofit with $50,000 budget probably cannot reasonably pay an executive director $45,000 (90% of budget) regardless of work performed, while a $2 million organization might reasonably pay $150,000 for executive leadership (7.5% of budget). Reasonableness depends on organizational size, program complexity, geographic market, required skills and experience, and what comparable nonprofits pay. Compensation consistently exceeding the 75th percentile of comparable positions raises IRS questions. Very high compensation percentages (over 50% of budget going to one person) raise both IRS concerns and funder skepticism about organizational priorities.

If I’m the founder and also the executive director, do I need to recuse myself from compensation decisions even though I’m doing the work? Yes, absolutely. Even though you’re performing valuable work deserving compensation, you have a direct personal financial interest in compensation decisions about your own pay. Independent directors without personal or family interest must review comparability data, discuss appropriate compensation levels, and vote on your compensation without your participation in deliberation or voting. You can provide information about your responsibilities and work performed, but you should leave the meeting during actual compensation discussion and decision. This independent review process is critical for both IRS compliance (safe harbor requirements) and organizational credibility with funders who scrutinize insider compensation decisions.

What happens if the IRS determines compensation was excessive—do I have to pay money back? If the IRS determines compensation constitutes an excess benefit transaction (payment exceeding reasonable compensation for services), several consequences can occur. The recipient (person who received excess compensation) must repay the excess amount plus interest—if you received $100,000 but reasonable compensation was $60,000, you’d repay $40,000 plus interest. Additionally, the recipient faces excise taxes on the excess benefit (25% initially, potentially 200% if not corrected). Organization managers (board members) who knowingly approved the excessive compensation also face excise taxes (10% of excess benefit up to $20,000 per manager). The organization itself doesn’t lose tax-exempt status for isolated excess benefit transactions, but pattern of excessive compensation or private benefit can lead to revocation. These penalties make proper procedures and reasonable compensation levels critical.

Should I wait to take any compensation until the nonprofit is financially stable, or can I pay myself from the beginning? This is a strategic decision depending on financial reality and personal circumstances. Many founders volunteer during the startup phase while building revenue, then begin receiving compensation once organizational income reaches sustainable levels—this approach reduces financial stress on new organizations and demonstrates founder commitment to mission over personal gain. However, founders with relevant professional expertise providing significant work deserve fair compensation even during startup if organizational revenue supports it. Consider: Can the organization afford your compensation while maintaining programs and reserves? Will taking compensation during startup create IRS or funder concerns about priorities? Do you have personal financial flexibility to volunteer temporarily? Can you start with part-time or reduced compensation rather than full market-rate salary? Many Temecula nonprofits use hybrid approaches—founders volunteer initially, begin receiving partial compensation as revenue grows, and eventually transition to market-rate salaries as organizations stabilize.

What to do next (DIY vs Done-With-You)

DIY approach: Research compensation for comparable positions by searching nonprofit salary surveys from CalNonprofits.org or national organizations, reviewing Form 990 filings from similar-sized nonprofits in similar program areas using GuideStar/Candid databases, checking job postings for nonprofit positions in your region, and documenting all sources and salary ranges you find. If considering compensating yourself or another founder, identify truly independent board directors who have no personal or family relationship with the person being compensated. Develop written employment agreement or contractor arrangement documenting compensation amount, services provided, expected hours, benefits, and term. Schedule board meeting where independent directors review comparability data, discuss whether proposed compensation is reasonable, and vote on approval with interested parties recused from discussion and voting. Document the entire process in meeting minutes including comparability data reviewed, basis for determining reasonableness, and individual votes. Maintain all documentation for IRS review. Review compensation annually against updated comparability data. If you cannot identify genuinely independent directors to review founder compensation, this signals that compensation should wait until board independence can be established.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive compensation planning for Temecula and Inland Empire nonprofits ensuring compliance with IRS requirements while supporting sustainable leadership. We help develop compensation philosophy appropriate to organizational stage and financial capacity, conduct thorough comparability research from multiple reliable sources documenting market-rate compensation for your positions, assess conflict of interest situations and identify which directors can provide independent review, design proper governance procedures ensuring independent board review and approval, prepare written employment agreements or contractor arrangements documenting compensation terms clearly, guide board meetings through proper approval processes with appropriate recusal and documentation, ensure accurate Form 990 compensation disclosure and reporting, develop compensation policies governing future decisions and reviews, and provide ongoing guidance as organizations grow and compensation needs evolve. This comprehensive approach ensures founder compensation serves organizational needs while maintaining IRS compliance, funder confidence, and organizational sustainability.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Sources

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.