19 Jan What Are the Basic Steps to Start a Nonprofit in California?

Short Answer

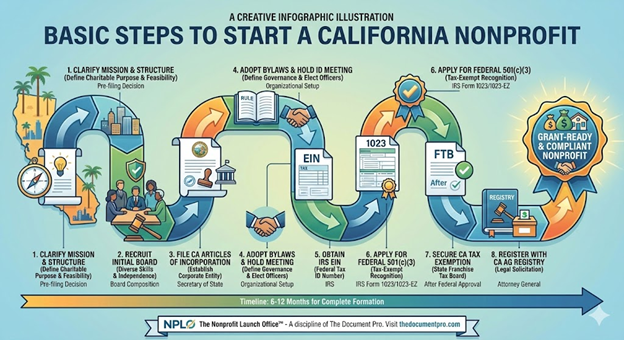

Starting a nonprofit in California requires completing several sequential steps: clarifying your charitable mission and determining whether nonprofit structure serves your goals, selecting and reserving a compliant organizational name, recruiting initial board members who meet legal requirements, drafting and filing Articles of Incorporation with the California Secretary of State establishing corporate existence, adopting bylaws defining governance structure and operational procedures, obtaining an Employer Identification Number from the IRS for tax and banking purposes, applying for federal 501(c)(3) tax-exempt recognition through IRS Form 1023 or 1023-EZ, securing California state tax exemption with the Franchise Tax Board after federal approval, and registering with the California Attorney General Registry of Charities to legally solicit donations. Eligibility varies by organization, but completing all steps typically requires 6-12 months and establishes the compliance foundation necessary for pursuing grants, accepting tax-deductible donations, and operating as a recognized charitable organization in California’s complex regulatory environment.

What foundational decisions must you make before filing any paperwork?

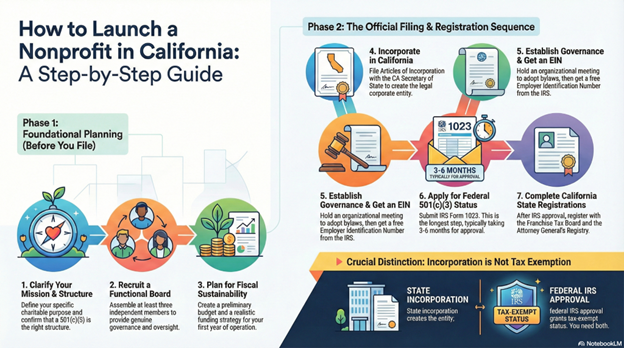

Mission clarity represents the most critical pre-filing decision because your charitable purpose determines IRS eligibility, shapes every formation document, guides board recruitment, and defines programmatic boundaries for your organization’s entire existence. Riverside founders should articulate precisely what community need their nonprofit addresses, what populations it serves, what activities it conducts, and what outcomes it pursues—not in vague generalities like “helping people” but in specific, demonstrable charitable purposes that qualify under IRS Section 501(c)(3). The mission statement becomes foundational language appearing in Articles of Incorporation, IRS applications, grant proposals, and public communications, so investing time in clarity before filing prevents costly amendments later.

Nonprofit structure appropriateness requires honest assessment of whether forming a 501(c)(3) charitable organization actually serves your goals better than alternative structures. Some community initiatives function better as informal volunteer groups, fiscally sponsored projects, social enterprises structured as benefit corporations, or collaborative programs of existing nonprofits rather than independent tax-exempt organizations. Consider whether you have sustainable funding sources beyond initial enthusiasm, whether you can recruit and maintain a functional board providing governance oversight, whether you’re prepared for ongoing compliance obligations including annual IRS and California filings, and whether the benefits of tax-exempt status (tax-deductible donations, grant eligibility, tax exemption) justify the administrative burdens and restrictions nonprofits face.

Board composition planning before filing Articles of Incorporation prevents common problems like insufficient directors to meet California’s three-person minimum, board members who don’t understand fiduciary responsibilities, or governance structures that violate conflict of interest rules. Ideal founding boards include members bringing diverse skills—financial oversight, legal/compliance understanding, fundraising capacity, programmatic expertise, community connections—and represent the communities you serve. California law prohibits nonprofit boards from being controlled by single families or having majority membership receiving compensation from the organization, so board design must ensure genuine independent oversight rather than serving as rubber stamp for founders’ decisions.

Fiscal sustainability planning before incorporation establishes realistic expectations about revenue generation and operational costs. Map potential funding sources—individual donations, foundation grants, government contracts, earned income, corporate sponsorships—and honestly assess which are accessible given your mission, capacity, and timeline. Develop preliminary budgets showing startup costs (incorporation fees, initial supplies, insurance) and first-year operating expenses (space, staff/contractors, program costs, compliance) against projected revenue. Organizations that launch without financial planning often discover too late that their program models don’t generate sufficient revenue to sustain operations, leading to organizational collapse despite good intentions.

What are the actual filing steps in sequence with California and federal agencies?

Name reservation with California Secretary of State represents the first formal step, requiring that your chosen name includes a corporate designation (Corporation, Incorporated, Limited, etc. or abbreviations Corp., Inc., Ltd.), doesn’t confusingly resemble existing registered names, and complies with nonprofit naming restrictions. The SOS business name database at bizfileonline.sos.ca.gov allows checking name availability before attempting reservation or filing. While name reservation isn’t mandatory, it protects your chosen name for 60 days while you prepare other formation documents, preventing another organization from registering the same name during your preparation period.

Articles of Incorporation filing with California Secretary of State creates the legal corporate entity by submitting Form ARTS-PB-501(c)(3) or equivalent document containing required elements: corporate name and California address, statement of charitable purpose aligned with IRS requirements, dissolution clause specifying that assets go to other 501(c)(3) organizations if your nonprofit dissolves, prohibition on private inurement ensuring no individual profits from organizational assets, and initial agent for service of process with California street address. The current filing fee is $30 plus $15 for Statement of Information if filed simultaneously. Upon acceptance, California issues a corporation number and your nonprofit legally exists as a California corporation, though not yet tax-exempt.

Organizational meeting of initial board establishes governance by adopting bylaws that specify board size and meeting requirements, officer positions and duties, membership provisions if applicable, amendment procedures, and operational policies. The board elects officers (typically president, secretary, treasurer at minimum), adopts conflict of interest and other essential policies, authorizes bank account opening, and documents decisions in meeting minutes. This organizational meeting creates the governance foundation the IRS examines when evaluating 501(c)(3) applications, so documentation demonstrating thoughtful, independent governance strengthens federal recognition prospects.

Employer Identification Number application through IRS Form SS-4 provides the federal tax identification number required for opening bank accounts, filing IRS Form 1023/1023-EZ for tax exemption, hiring employees or contractors, and fulfilling various regulatory requirements. EIN application is free and can be completed online at irs.gov with immediate number assignment for most applicants. The EIN becomes your nonprofit’s permanent federal tax identifier, remaining unchanged even if organizational name or structure changes, and appears on all federal tax documents, grant applications, and financial records.

IRS Form 1023 or 1023-EZ application for 501(c)(3) recognition represents the most complex and consequential filing, requiring detailed information about organizational purpose, planned activities, governance structure, compensation arrangements, financial projections, and relationships with other entities. Form 1023-EZ (simplified version for smaller organizations projecting under $50,000 annual gross receipts) costs $275 and processes faster but provides less detailed IRS review. Full Form 1023 (for larger or more complex organizations) costs $600 and involves more extensive documentation but creates more thorough IRS determination. Processing typically takes 3-6 months, during which the IRS may request additional information. Upon approval, the IRS issues a determination letter confirming 501(c)(3) status generally retroactive to your incorporation date.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

The Nonprofit Launch Office operates within a strategic framework designed to help California nonprofits move from formation to fundability:

Launch is precisely the process this question addresses—the sequential steps transforming an idea into a legally recognized, grant-eligible nonprofit organization. Launch includes both the mechanical filing steps (Articles of Incorporation, EIN application, IRS Form 1023) and the strategic planning decisions (mission clarity, board recruitment, financial sustainability) that determine whether the formed nonprofit functions effectively or struggles from inception. Proper Launch execution establishes compliance foundations, creates functional governance, and positions organizations for grant success rather than creating problems requiring later Fix interventions.

Fix becomes necessary when Launch steps were completed incorrectly, incompletely, or not at all—organizations that incorporated without proper charitable purpose language requiring Articles amendment, boards that never adopted bylaws or held organizational meetings requiring retroactive documentation, nonprofits that operated for years without applying for IRS recognition now facing revocation threats, or entities that missed California registrations and now need restoration. Fix is always more expensive, time-consuming, and complicated than proper Launch would have been, which is why understanding correct formation sequence matters enormously.

Fund represents the operational capability that proper Launch enables—once you’ve completed all formation steps including federal and state recognition, you can pursue institutional grants, accept tax-deductible donations, and operate with the compliance profile funders verify. Organizations that shortcut Launch steps often discover they cannot access funding because they lack required recognition, registration, or documentation. Fund-phase success depends on Launch-phase thoroughness.

Federal Recognition through IRS 501(c)(3) determination forms the foundation enabling most institutional funding and tax-deductible donations. While California incorporation creates corporate existence, federal IRS recognition creates tax-exempt charitable status. The two-level structure—state corporate formation plus federal tax exemption—confuses many Riverside founders who assume incorporating as a nonprofit automatically confers tax benefits. Understanding that federal recognition is separate and subsequent to state incorporation prevents the common error of attempting grant applications before IRS determination arrives.

CA Compliance Triangle represents the three California agencies requiring separate post-federal-recognition compliance: Secretary of State (Statement of Information biennial filings maintaining Active status), Franchise Tax Board (annual Form 199 or 199N maintaining state tax exemption), and Attorney General Registry of Charities (initial registration plus annual RRF-1 renewals authorizing fundraising). These three state-level requirements supplement rather than replace federal IRS obligations, creating the four-point compliance framework (IRS plus three California agencies) that distinguishes California nonprofit oversight from simpler single-agency states.

Step-by-step: How NPLO guides Riverside nonprofits through complete formation

Step 1: Mission and Structure Consultation We help clarify your charitable purpose into specific, IRS-compliant language that will appear in formation documents and determine whether nonprofit structure actually serves your goals better than alternatives. This consultation includes assessing financial sustainability prospects, evaluating whether sufficient board and leadership capacity exists, and confirming that your planned activities qualify as charitable under 501(c)(3) requirements. Many potential founders discover through this assessment that fiscal sponsorship, collaborative partnership, or other structures better serve their specific situations.

Step 2: Board Recruitment and Development We guide recruitment of initial board members meeting California’s three-person minimum with skills, diversity, and independence that signal functional governance to IRS reviewers. We help founding boards understand fiduciary responsibilities, conflict of interest obligations, and meeting requirements rather than treating board membership as honorary recognition. Proper board composition and education from day one prevents governance problems that plague nonprofits with rubber-stamp boards lacking oversight capacity.

Step 3: Name Selection and Availability Verification We help select organizational names that are distinctive, memorable, aligned with mission, compliant with California requirements, and available for registration. This includes checking Secretary of State name availability, verifying that domain names and social media handles are available for consistency, and ensuring the name isn’t confusingly similar to existing Riverside-area nonprofits serving similar populations. Strong name selection creates brand identity supporting fundraising and community recognition.

Step 4: Articles of Incorporation Preparation and Filing We draft Articles of Incorporation containing all required IRS-compliant language—charitable purpose statement, dissolution clause, private inurement prohibition, and other provisions IRS examines when reviewing 501(c)(3) applications. We file with California Secretary of State and manage any questions or requests for clarification. Properly drafted Articles prevent the need for amendments later when IRS identifies language problems, saving time and money.

Step 5: Bylaws Development and Organizational Meeting We prepare comprehensive bylaws tailored to your organization’s structure, size, and governance needs rather than using generic templates that may not fit. We guide the organizational board meeting where bylaws are adopted, officers are elected, conflict of interest policies are approved, and initial operational decisions are documented. We ensure meeting minutes demonstrate genuine deliberation and independent governance rather than founder-controlled rubber-stamping.

Step 6: EIN Application and Initial Compliance Setup We complete IRS Form SS-4 EIN application and establish initial compliance tracking systems—filing calendars covering federal and California obligations, document organization protocols, and basic record-keeping structures. Early compliance systems prevent the drift into noncompliance that creates problems when organizations pursue grants 18-24 months post-formation.

Step 7: IRS Form 1023/1023-EZ Preparation and Submission We prepare complete, accurate IRS applications including detailed narratives about planned activities, financial projections, governance structures, and compensation arrangements. We guide the choice between Form 1023-EZ (simpler, faster but less IRS scrutiny) versus full Form 1023 (more complex but more thorough IRS review). We manage IRS correspondence if additional information is requested and coordinate response strategies maximizing approval likelihood.

Step 8: California State Compliance Completion Once IRS determination arrives, we complete California state registrations—Franchise Tax Board exemption application (Form 3500A), Attorney General Registry of Charities initial registration (Form CT-1), and any other required state filings. We establish ongoing compliance monitoring ensuring Statement of Information, Form 199, and RRF-1 filings happen on schedule. This comprehensive approach delivers fully compliant, grant-ready organizations rather than partially formed entities missing critical registrations.

Checklist: What you should have ready before starting formation

Riverside founders beginning nonprofit formation should prepare or gather:

- Clear mission statement articulating specific charitable purpose, target populations, planned activities, and intended outcomes in IRS-compliant language

- Founding board member commitments from at least three individuals willing to serve, meeting regularly, and providing genuine governance oversight

- Initial board member information including full legal names, residential addresses, email addresses, phone numbers, and brief biographical information

- Organizational name options (primary plus alternates) that are distinctive, mission-aligned, and available for California registration

- Registered agent information including name and California street address (not PO Box) of person or service receiving legal notices

- Principal office address in California where organizational business is conducted and records are maintained

- Preliminary program descriptions explaining what activities you’ll conduct, how they serve charitable purposes, and who benefits

- Initial officers identified including president/CEO, secretary, and treasurer with understanding of their roles and responsibilities

- Financial projections showing anticipated startup costs, first-year operating expenses, and realistic revenue sources

- Funding strategy outline identifying potential individual donors, foundation prospects, earned income possibilities, or other revenue streams

- Conflict of interest policy draft addressing how the board will handle conflicts, require annual disclosures, and ensure independent decision-making

- Formation budget covering California incorporation fee ($30), IRS application fee ($275-$600), registered agent service if using one, potential professional assistance, and initial operating costs

- Timeline expectations understanding that complete formation from incorporation through IRS determination typically requires 6-12 months

- Commitment to ongoing compliance recognizing that nonprofits face annual federal and California filing obligations requiring time, attention, and resources

Quick Answers (PPA)

How long does the complete formation process actually take from start to finish? The mechanical filing steps—California incorporation, EIN application, IRS Form 1023 submission—can be completed within 2-4 weeks if you have all information prepared. However, IRS processing of 501(c)(3) applications typically takes 3-6 months, during which your organization exists as a California corporation but lacks federal tax-exempt recognition. Total timeline from initial planning through receiving IRS determination and completing California state registrations typically spans 6-12 months for well-prepared applications. Delays occur when IRS requests additional information, when founders take time gathering required documentation, or when formation steps are completed out of sequence requiring corrections. Organizations needing grant eligibility quickly sometimes pursue fiscal sponsorship as a bridge during the formation waiting period.

Can I start operating programs and accepting donations before IRS determination arrives? Yes, you can operate programs and accept donations after California incorporation and before IRS determination, but with important caveats. Donors cannot claim tax deductions for contributions until your IRS determination is granted, though recognition is typically retroactive to your incorporation date once approved. Most institutional funders won’t consider grant applications until you have actual IRS determination in hand and appear in the TEOS database. Early operations should focus on individual donor cultivation, program piloting, board development, and preparation for aggressive fundraising once determination arrives rather than attempting premature grant applications likely to be rejected for lack of federal recognition.

Do I need a lawyer to start a nonprofit, or can I do it myself? California law doesn’t require attorney involvement to form nonprofits—individuals can complete incorporation, EIN application, and even IRS Form 1023 independently using IRS instructions, online resources, and nonprofit formation guides. However, several formation elements benefit significantly from professional guidance: drafting Articles of Incorporation language that satisfies both California corporate law and IRS charitable requirements, preparing comprehensive bylaws tailored to your governance needs, developing conflict of interest and other policies meeting legal standards, and completing Form 1023 narratives that present your organization favorably to IRS reviewers. Many Riverside founders use hybrid approaches—handling simple mechanical filings themselves while getting professional review of critical documents like Articles and Form 1023 before submission.

What happens if we make mistakes in our formation documents—can we fix them later? Most formation mistakes can be corrected through amendments, though corrections are always more expensive and time-consuming than getting documents right initially. Articles of Incorporation amendments require California Secretary of State filing fees and potentially IRS notification if changes affect your tax-exempt status. Bylaws amendments require board approval and documentation but don’t require state filing. IRS Form 1023 errors discovered during processing can often be corrected through supplemental submissions, though errors suggesting misrepresentation or fundamental disqualification cause application rejection. The most problematic mistakes involve operating for extended periods under flawed formation documents—incorporating without proper charitable purpose language, adopting bylaws with California-noncompliant provisions, or forming board structures that violate conflict rules—requiring complex and expensive remediation when discovered during grant applications or audits.

What’s the difference between incorporating in California and getting 501(c)(3) status from the IRS? California incorporation creates corporate legal existence—your organization becomes a California nonprofit corporation, can enter contracts, hold property, and conduct business as a legal entity. However, incorporation alone doesn’t confer tax-exempt status or make donations tax-deductible. Federal 501(c)(3) recognition from IRS creates tax exemption—your organization becomes exempt from federal income tax and donors can claim charitable deductions for contributions. You need BOTH—California incorporation establishes the corporate entity, and IRS recognition grants that entity tax-exempt charitable status. This two-level structure confuses many founders who assume incorporating as a “nonprofit” automatically provides tax benefits, when in fact federal IRS determination is a separate, subsequent application proving your incorporated entity serves charitable purposes qualifying for tax exemption.

What to do next (DIY vs Done-With-You)

DIY approach: Begin by clarifying your mission through written exercises answering: What specific community need does your nonprofit address? What populations do you serve? What activities will you conduct? What measurable outcomes do you seek? Recruit at least three potential board members willing to provide genuine governance oversight and meet regularly. Research name availability through California Secretary of State business name database and secure matching domain names. Review IRS Publication 557 “Tax-Exempt Status for Your Organization” to understand 501(c)(3) requirements and eligibility criteria. Download California Form ARTS-PB-501(c)(3) and review requirements for Articles of Incorporation. Obtain nonprofit bylaws templates from resources like CalNonprofits.org and adapt to your governance structure. Create preliminary budgets showing startup costs and first-year operating expenses against realistic revenue projections. File California Articles of Incorporation through bizfileonline.sos.ca.gov once prepared. Apply for EIN online at irs.gov immediately after incorporation. Hold organizational board meeting adopting bylaws, electing officers, and documenting decisions in meeting minutes. Begin preparing IRS Form 1023 or 1023-EZ using instructions and worksheets at irs.gov. Understand this DIY approach requires significant time investment, careful attention to detail, and willingness to learn complex regulatory requirements.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive formation guidance for Riverside and Inland Empire founders, ensuring proper completion of all federal and California requirements in correct sequence. We clarify charitable mission into IRS-compliant language that strengthens both formation documents and future grant applications, guide board recruitment and development ensuring functional governance from inception, prepare Articles of Incorporation containing all required provisions while avoiding common language problems that complicate IRS applications, draft comprehensive bylaws tailored to your structure rather than using generic templates, facilitate organizational meetings that demonstrate genuine deliberation and independent oversight, complete EIN applications and establish initial compliance tracking systems, prepare complete IRS Form 1023 or 1023-EZ applications maximizing approval likelihood, and coordinate California state registrations once federal determination arrives. This comprehensive approach delivers fully formed, grant-ready organizations typically within 6-9 months while preventing the formation errors that require expensive later remediation, ensuring founders understand ongoing compliance obligations rather than treating formation as one-time event, and positioning new nonprofits for funding success rather than discovering barriers when first grant applications are attempted.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Sources

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.