15 Jan Can a Nonprofit with No Prior 990 Filings Still Be Considered for Grants?

Short Answer

Nonprofits with no prior Form 990 filings can still be considered for grants if they’re genuinely new organizations that haven’t yet reached their first filing deadline, can provide alternative financial documentation like operating budgets and bank statements, target funders who specifically support emerging organizations without extensive financial history requirements, and proactively explain their filing timeline in cover letters rather than leaving reviewers to wonder why filings are absent. Eligibility varies by grant, but the key distinction is between legitimately new organizations that haven’t filed because filings aren’t yet due versus organizations that missed required filings through noncompliance—funders generally accommodate the former while rejecting the latter as evidence of poor governance and financial management.

What does Form 990 filing status tell funders about an organization?

Form 990 filing history provides funders with standardized financial transparency showing total revenue by source, expenses by category and program, compensation information for key staff, governance practices and policies, and narrative descriptions of organizational activities and accomplishments. The IRS requires most tax-exempt organizations to file annually—Form 990-N (e-postcard) for very small organizations with gross receipts under $50,000, Form 990-EZ for organizations with gross receipts under $200,000 and total assets under $500,000, or full Form 990 for larger organizations. Filing history demonstrates compliance with federal reporting obligations that maintain tax-exempt status.

When funders review Form 990 filings, they’re assessing fiscal responsibility and organizational capacity beyond what narrative applications convey. Form 990 data reveals whether an organization spends reasonable percentages on programs versus administration and fundraising, compensates staff at appropriate levels, maintains adequate cash reserves or operates with precarious finances, has diversified revenue sources or depends heavily on single funders, and operates at scales consistent with their stated impact claims. Multi-year Form 990 histories show trends—growing, stable, or declining organizations—that inform funding decisions.

Missing Form 990 filings trigger immediate questions in reviewers’ minds. For Moreno Valley nonprofits applying to sophisticated funders, absence of Form 990 documentation suggests one of several scenarios: the organization is extremely new and hasn’t reached first filing deadline yet (understandable), the organization is small enough that Form 990-N suffices but hasn’t filed even that minimal requirement (compliance red flag), the organization fell behind on filings and faces potential IRS revocation (serious problem), or the organization doesn’t understand that Form 990 filing is mandatory for maintaining tax-exempt status (competence concern). Only the first scenario is acceptable to most funders.

The IRS publicly posts Form 990 filings, making them independently verifiable through databases like GuideStar/Candid, Foundation Directory Online, and ProPublica’s Nonprofit Explorer. Funders often check these databases regardless of what applicants submit, discovering discrepancies between applications claiming financial health and Form 990s showing concerning patterns. The transparency Form 990 provides means organizations cannot easily hide financial problems from funders conducting thorough due diligence.

How do new nonprofits explain legitimate absence of Form 990 filings?

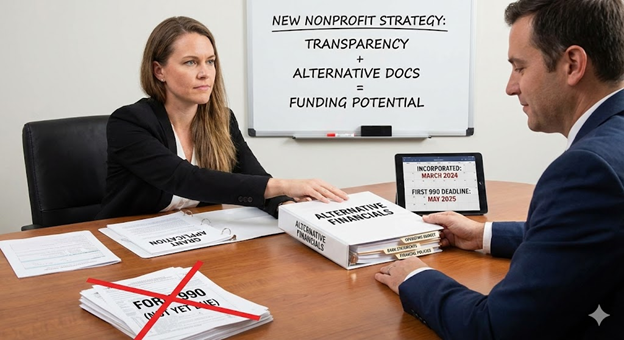

Proactive explanation in cover letters or application narratives prevents funder confusion about missing Form 990 filings. Rather than hoping reviewers won’t notice or assume they’ll understand, new Moreno Valley nonprofits should state clearly: “Our organization incorporated in March 2024 with fiscal year ending December 31, 2024. Our first Form 990 will be due May 15, 2025. We have not yet filed Form 990 because our first filing deadline has not arrived. We have provided our operating budget and recent bank statements as alternative financial documentation.” This transparency demonstrates awareness of filing requirements and honest communication rather than attempting to hide information.

The filing timeline explanation should match your actual organizational age and fiscal year structure. Organizations with fiscal years ending December 31 file Form 990 by May 15 of the following year (or November 15 with extensions). Organizations with fiscal years ending June 30 file by November 15 (or May 15 of the following year with extensions). New organizations formed mid-year often have short first fiscal years—incorporating in September with December 31 fiscal year end means your first “year” is only four months, but you still file Form 990 covering that short period. Understanding and accurately explaining your specific timeline shows competence even when you lack filing history.

Alternative financial documentation fills the gap that Form 990 would otherwise occupy. New nonprofits should provide comprehensive operating budgets showing detailed revenue projections and expense allocations, recent bank statements demonstrating actual financial activity and account balances, any financial statements prepared internally or by bookkeepers/accountants, financial policies addressing approval authorities and internal controls, and narratives explaining financial assumptions and sustainability plans. While these alternatives don’t provide the standardized comparability that Form 990 offers, they demonstrate financial thinking and fiscal responsibility to reviewers evaluating new organizations.

Targeting funders who explicitly support emerging organizations increases acceptance of limited filing history. Application guidelines stating “open to organizations in their first three years” or “capacity building grants for new nonprofits” signal that absence of extensive Form 990 history won’t automatically disqualify applications. These funders structure evaluation criteria accounting for limited track records, often placing greater weight on leadership credentials, community need, program design quality, and partnership strength rather than emphasizing financial history that new organizations cannot provide.

Framework: Launch → Fix → Fund + Federal Recognition + CA Compliance Triangle

The Nonprofit Launch Office operates within a strategic framework designed to help California nonprofits move from formation to fundability:

Launch includes understanding Form 990 filing requirements from day one so you can explain your filing timeline accurately when pursuing early grants. Launch-phase organizations should establish fiscal years strategically (many choose December 31 for simplicity with calendar years), understand which Form 990 version applies based on revenue projections, implement financial record-keeping systems that facilitate eventual Form 990 preparation, and anticipate that absence of Form 990 filings will raise questions requiring clear explanations during first-year grant applications.

Fix addresses situations where nonprofits missed required Form 990 filings—either through ignorance that filing was mandatory (many small organizations incorrectly assume “no taxes owed” means “no filing required”) or through administrative failure despite knowing the obligation. IRS automatically revokes 501(c)(3) recognition for organizations failing to file for three consecutive years, creating serious grant eligibility problems. Fix work involves filing delinquent returns, requesting retroactive reinstatement if revocation occurred, paying penalties, and demonstrating to funders that you’ve addressed compliance gaps before they’ll consider renewed funding.

Fund represents the operational state where Form 990 filing happens consistently on schedule, creating the multi-year filing history that strengthens grant applications. Fund-phase organizations view Form 990 not as burdensome paperwork but as public accountability documentation and funder communication tool. They file before deadlines, review filings for accuracy and completeness, understand what Form 990 information tells funders about their operations, and use filing data strategically when crafting grant narratives about financial health and program spending.

Federal Recognition through IRS 501(c)(3) determination establishes the tax-exempt status that makes Form 990 filing mandatory. Organizations must file annual returns to maintain recognition—failure to file triggers the automatic revocation that ends grant eligibility immediately. Understanding that federal recognition creates ongoing filing obligations prevents the compliance gap where organizations celebrate receiving determination letters without realizing annual filings are required thereafter.

CA Compliance Triangle includes California’s state-level equivalent of Form 990—Form 199 or Form 199N filed with the Franchise Tax Board. While funders focus more heavily on federal Form 990, California funders may also request Form 199 filings demonstrating state compliance. New Moreno Valley nonprofits explaining absence of Form 990 should similarly explain Form 199 timeline—often the same explanation works for both since filing schedules align: “We have not yet filed Form 990 or Form 199 because our first fiscal year has not yet ended.”

Step-by-step: How NPLO helps nonprofits address Form 990 gaps in grant applications

Step 1: Filing Status Assessment We determine your actual Form 990 filing status—are you truly too new to have filed, or have you missed required filings? This assessment distinguishes between “legitimate absence requiring explanation” versus “compliance gap requiring correction.” The strategies differ dramatically depending on which scenario applies. We review your incorporation date, fiscal year structure, and time elapsed to calculate when filings were or will be due.

Step 2: Timeline Explanation Development We craft clear, accurate explanations of your filing timeline for inclusion in cover letters and application narratives. These explanations state your incorporation date, fiscal year ending, first filing deadline, and what alternative financial documentation you’re providing. The explanation tone conveys competence and transparency rather than defensiveness or confusion about requirements.

Step 3: Alternative Financial Documentation Assembly We help gather and organize financial materials that demonstrate fiscal responsibility despite absence of Form 990—operating budgets with detailed assumptions, recent bank statements showing actual activity, any financial statements prepared internally or by professionals, financial policies addressing controls and oversight, and narratives explaining financial sustainability plans. This package provides reviewers with comparable information to what Form 990 would show.

Step 4: Funder Research and Targeting We identify which funders on your prospect list have flexible requirements for new organizations versus which impose strict multi-year Form 990 requirements that make your application premature. This targeted approach prevents wasting time on funders whose guidelines explicitly require “three years of Form 990 filings” when you’re a first-year organization that couldn’t possibly satisfy that criterion.

Step 5: Form 990 Preparation Planning Even though your first Form 990 isn’t yet due, we help establish the financial record-keeping and documentation systems that will make preparation straightforward when the deadline arrives. Organizations that implement good systems from day one file accurate, complete Form 990s easily. Organizations that operate informally until deadline approaches struggle with reconstructing financial information and often submit incomplete or error-riddled filings.

Step 6: Delinquent Filing Remediation (if applicable) If assessment reveals you’ve missed required filings, we coordinate urgent remediation—preparing delinquent Form 990 returns for all missed years, filing with IRS and paying associated late penalties, requesting retroactive reinstatement if automatic revocation occurred, and developing governance improvements preventing future missed filings. We also help explain compliance gaps honestly to funders while demonstrating corrective action.

Step 7: Application Customization We customize how you address Form 990 absence for each specific application. Some applications have explicit fields for uploading Form 990s with clear options like “Not yet required—organization formed [date].” Others require narrative explanation in cover letters or supplemental materials. We ensure each application clearly addresses why Form 990 isn’t included rather than leaving reviewers to speculate.

Step 8: Future Filing Communication Strategy Once you file your first Form 990, we help communicate this milestone to funders who previously received applications without filings—”We’re pleased to share that our organization has now filed our first Form 990, demonstrating [positive financial patterns like strong program spending, diverse revenue, etc.].” This proactive communication shows organizational maturation and builds funder confidence for subsequent grant cycles.

Checklist: What you should provide when Form 990 filings aren’t available

Nonprofits applying for grants without Form 990 filing history should ensure applications include:

- Clear written explanation of filing timeline stating incorporation date, fiscal year structure, first filing deadline, and why filings aren’t yet available

- Operating budget for current fiscal year showing detailed revenue projections by source and expense allocations by program and category

- Recent bank statements (typically 3-6 months) demonstrating actual financial activity, account balances, and cash flow patterns

- Financial statements if available—internally prepared balance sheets and income statements showing organizational financial position

- Financial policies addressing approval authorities, signing requirements, internal controls, and fund management procedures

- Board treasurer report or financial committee documentation showing regular financial oversight and review

- Funding sources narrative explaining current revenue—individual donations, earned income, in-kind contributions, volunteer support, or other sources

- Financial sustainability plan articulating how you’ll build sustainable revenue as you mature beyond seed funding phase

- Budget assumptions document explaining how you developed revenue projections and expense estimates for a new organization without historical data

- Cash reserve policy or discussion of how you’re building financial stability and managing cash flow fluctuations

- Fiscal sponsor documentation if operating under fiscal sponsorship—the sponsor’s Form 990 rather than your own (since sponsored projects file under sponsor)

- Comparison to peer organizations if possible—”Organizations of similar age and focus in our region typically operate on budgets of $X, which aligns with our projections”

- Commitment to future filing stating you understand Form 990 requirements and will file appropriately when deadlines arrive

- Contact information for board treasurer or financial committee chair if funders want to discuss financial oversight directly

- Proactive communication offering to provide Form 990 once filed if the grant award extends beyond your first filing deadline

Quick Answers (PPA)

What if a funder explicitly requires “most recent three years of Form 990 filings” and we’re too new to have three years? When funders specify multi-year Form 990 requirements, first contact them to ask whether newer organizations are eligible with alternative documentation or whether the requirement is absolute. Some funders state “three years” as standard language but make exceptions for promising new organizations. Others maintain the requirement firmly because their evaluation methodology depends on trend analysis requiring multiple years of data. If the requirement is absolute and you can’t satisfy it, don’t waste time applying—focus on funders with criteria you can meet. If exceptions are possible, provide whatever Form 990 history you have (even one year or none) with clear explanation and robust alternative financial documentation.

Does filing Form 990-N (the e-postcard for very small organizations) count as having Form 990 history? Form 990-N satisfies IRS filing requirements for organizations with gross receipts under $50,000, maintaining your tax-exempt status and preventing automatic revocation. However, Form 990-N provides almost no financial information to funders—it confirms your organization exists and filed something, but reveals nothing about revenue sources, expense patterns, program spending, governance practices, or organizational capacity. Many funders request “Form 990” expecting the informational content that Form 990-EZ or full Form 990 provides. If you’ve only filed Form 990-N, explain this proactively and provide detailed alternative financial documentation. Some funders accept this for very small organizations; others may view it as insufficient regardless of your legitimate reason for 990-N eligibility.

If we’re a fiscally sponsored project, whose Form 990 do we provide—ours or the sponsor’s? Fiscally sponsored projects operating under comprehensive sponsorship (Model A) do not file independent Form 990 returns—your activities and finances are included in the sponsor organization’s Form 990 as one of their programs. When applying for grants, you provide the sponsor’s Form 990 with explanation: “Our project operates under fiscal sponsorship by [Organization]. We have attached their most recent Form 990, which includes our project’s activities in Schedule O and financial information in the consolidated statements.” Some funders request additional documentation like project-specific budgets or financial reports beyond what appears in the sponsor’s consolidated Form 990.

What happens if funders discover we missed required Form 990 filings that we should have submitted? If funders discover missed filings during due diligence, they typically view this as serious governance failure indicating poor organizational management and compliance awareness. Most will reject applications immediately or pause review pending compliance correction. The appropriate response involves acknowledging the gap honestly, filing delinquent returns immediately with penalties, implementing governance improvements to prevent recurrence, and requesting opportunity to reapply once compliance is restored. Attempting to hide missed filings or make excuses beyond “we made an error, here’s how we’re correcting it” typically ends funding relationships. Prevention through understanding filing requirements from day one avoids this damaging scenario entirely.

Can we start applying for grants before we’ve filed our first Form 990 if the deadline hasn’t passed yet? Yes, absolutely. Being too new to have filed Form 990 yet is completely different from being old enough that filings should exist but are missing. New Moreno Valley nonprofits should pursue grants as soon as they achieve full compliance (IRS determination, California registrations) even if their first Form 990 isn’t due for months. The key is proactive explanation—”Our first fiscal year ends [date], with Form 990 due [deadline]. We have not yet filed because the deadline has not arrived. We have provided alternative financial documentation.” Most funders understand new organization timelines and evaluate applications based on available information rather than penalizing you for not having filed returns that aren’t yet due.

What to do next (DIY vs Done-With-You)

DIY approach: Determine your actual Form 990 filing status by reviewing your incorporation date and fiscal year ending to calculate when your first Form 990 is or was due. If you’re genuinely too new to have filed, draft clear explanation text stating your incorporation date, fiscal year, first filing deadline, and what alternative financial documentation you’re providing. Include this explanation in every grant application cover letter or narrative where Form 990 would normally be uploaded or referenced. Assemble comprehensive alternative financial documentation—detailed operating budget, recent bank statements, any financial statements, financial policies, and sustainability narrative. If you discover you’ve missed required filings, file delinquent returns immediately through IRS before pursuing additional grants—funders who discover missed filings typically reject applications regardless of program quality. Research funder requirements carefully—prioritize those who explicitly support emerging organizations over those requiring extensive financial history you cannot provide.

Done-With-You approach: The Nonprofit Launch Office provides comprehensive Form 990 strategy for Moreno Valley and Inland Empire nonprofits navigating grant applications without filing history. We assess your actual filing status distinguishing between legitimate absence versus compliance gaps requiring correction, develop accurate filing timeline explanations appropriate for grant applications, assemble alternative financial documentation packages demonstrating fiscal responsibility, identify and target funders whose requirements align with your available documentation rather than pursuing inappropriate opportunities, coordinate delinquent filing remediation if missed returns are discovered, implement financial record-keeping systems that facilitate smooth Form 990 preparation when deadlines arrive, customize application approaches explaining Form 990 absence appropriately for each funder’s specific requirements, and develop communication strategies for sharing first Form 990 once filed as evidence of organizational maturation. This guidance prevents both the premature applications to funders requiring extensive history you lack and the compliance crises from missed filings that block future funding access.

Contact

Book: https://thedocumentpro.com/

Call: 1(800) 285-0078

Email: mydocumentpro@gmail.com

The Nonprofit Launch Office™ — a discipline of The Document Pro, operated by Gitta Williams.

Operated by The Document Pro (Gitta Williams)

Sources

Disclaimer

Document preparation and nonprofit readiness support — not legal or tax advice.